Transcripts

1. About Son Han, Your Coach: again this classes on Leon Skill share, and I wanted to introduce myself. I want to put a face with the name before we dive into the material. My name is Son, and I'll be your guide today. I like to introduce myself in every class that I teach because it's important to put a face with the name. And you can see how passionate I am about the topic that we're talking about today, which is personal finance and helping the average person get their money in order. So just a few quick things about me that is first and four months. I don't talk about personal finance, having come from a place with a ton of money. I was not born with wealth. My parents did not give me $8 million then I created $100 million like That's not how it happened. I was the kid of refugee parents, and I literally had nothing. When I started college, my parents couldn't give me any money for college, so when I left, college actually left with $60,000 worth of debt. So without that much debt, I had to get a job in finance to make sure that I could pay it off. This is important because I know how hard it is to build wealth from the negative network point of view. I'm not coming from somewhere who has a lot of money and then made it even bigger. I came from the negative network, and I have a very large, positive network now. Other than that, you'll see that I was a kid of refugee parents and I took a year off and traveled the world . So this is not me just talking about financial freedom and never having done it. I actually did a semi retirement and took a year off to travel the world when I was 30. It was absolutely and unequivocally the best experience of my life, and I feel so fortunate to have been able to do that. I was in a place of financial freedom, and I still land to do what I wanted to do. I learned how to serve snowboard, and I volunteer with Doctors Without Borders in south Sudan again, amazing. Finally, we'll cover this in a later slide, but you that personal finance is not taught in our schools, so don't feel bad that you never learned any of the stuff in America. It's just the way it is. I mean, they don't teach this stuff in schools. In college, in grad school, I've been through all those I'm a c p a. On my chartered financial analyst. At no point was this ever talk to me, so don't feel bad. If you don't know how this information, we're going to teach it to you now. That's why I created this course on on skill share so that you're able and lucky enough to be able to take this class on skill share and spread the word by recommending this class on school chair to other skills, share students and people not even on sculpture, recommended to them and say, Take this class about personal finance on skill share. Throughout this class, you'll see me animations of meat or just Power point slides. We're going to switch things up to keep things interesting for you, but the majority of it, because there's a lot of information is going to be on PowerPoint slides and me voicing over and talking through it with you on certain things will pull out animations and make things interesting and add a little music videos, fun music videos here, there. So let's get started

2. 01 Why: I always start off all my classes with the compelling Why? Why should you watch this class and spend any amount of time watching this class? The reason. Toe Learn about money to learn that money can buy freedom. We all grow up learning that money can buy stuff. That's what America wants us know because all American companies air profit maximizing, which is a fancy way of saying that they want you to spend all of your money with them. Yes, you heard me, right. All of your money and even money you don't have through loans. Thes companies like Nike, Google Instagram. While it's Fargo and Apple want every dime you have, The more money spend with these companies, the bigger they get. Your job is a learn how to protect yourself, and that's what this class does. Think about it this way. If I told you that you have to go out in the world today and navigate without a phone, how would you feel a phone is almost necessary in this day and age? Maybe you could get by without being able to text or use your phone or any other APS out there, make it a heck of a lot harder. The same goes for learning about money. Maybe you could get by without knowing about money, but it's going to make it really tough. Which is why 60% of Americans don't even have $500 in savings. It's really tough life when you don't know about money. My life school has been to educate others about money. Mainly my life goal is educate the middle and low income groups about money because that's where I came from. I came as a refugee, a really poor background, and it's really easy to talk about money when you have it. But when you don't even have a bed to sleep on, then let's hear you talk about money. That's my background. I didn't have a bed until I was about 10 years old, but learning about money and learning how it was able to buy me freedom. That's what helped me understand the uses of money. Now I work because I want to work, not because I have to. There's a huge difference there. The sad thing is, no one taught me about money through any of the courses in my high school college grad school or getting my C p. A or my CF A. In none of those where they taught me about personal finance. And the sad part was that I was an accounting in finance major to I had to learn about it on my own, digging through massive amounts of websites, books, articles, etcetera. My goals that change, that I've taught over 1000 students about personal finance, and I'm how to make money work for you. My classes air not filled with any BS. It's all riel because my incentive is to help others. This class is made specifically for skill, share and skill share students on Lee, and it's on Lee available in skill share to finalize this sex section. Money is at the root of almost every transaction in modern life. Yet we don't learn how to use money in our everyday lives. We hear what the media tells us we should buy this or by that or buying this will give us a status symbol. We should take out loan for anything that we can't afford right now. Yes, we hear you. We hear all that, but what we never learn how we can use money to our advantage to buy a life free, off financial stress. This is also not a get rich quick scheme earning money to buy life. Our financial free of financial stress takes hard work and takes years to do. This course gives you the road map and the knowledge. At the end of this two hour course, you'll learn how to use money to buy a life free of financial stress stress, which will then allow you to take whatever job you want and the eventual freedom to decide if you want to work or not. If you're like me and you like working and making a difference, then you'll probably continue working. My financial situation allows me to live a stress free life financially. That's the compelling Why on why should stick through this course and finish it on skill share.

3. 02 The Material is Easy: so learning personal finance takes two hours or so to learn literally. Almost everything you need to know can be learned within that two hour period to keep you engaged. We have a class project, so pronounce the handout. It's in pdf printed out. Follow along with me, answer the questions and then upload that as your class project. I've answered those questions. You can see my handwriting. I've uploaded that as my class project, and that's what we're asking you to do. On skill share is take the handout, print it out, fill out the questions and write down your answers and then upload as a class project to inspire other students that take this class as well. So as a skill share user, we again ask you to upload your completed hand out in the project gallery to inspire other students to learn about money. Again. The hard part about personal finance is not learning it. It's actually the material is actually very easy to learn. The hard part is staying motivated. It's just like saying healthy, right, staying healthy, right, and work out every day while we can say that. But the hard part is actually doing it. That's the same thing with personal finance. It's very easy to learn the information you're gonna take this cost. You would be like, Wow, son, thinking for all this information, the hard part is staying motivated. So find a way to create incentives to create an ability for you to constantly stay motivated and stay hungry so you can build that financial wealth and you can live the life you want.

4. 04 Purpose of the Course: In addition to the handout, you actually have access to the power point slides. So please make sure to put out the PowerPoint slides and follow along. The purpose of this course is to prepare you for the real world. It matters to everyone. By the end of this course, you're going to be able to do a lot of things, But the things I want to focus on our one, you're gonna understand what network means and how it's and the most important metric not your credit score or how much you spend. That's the most important metric in personal finance is your network two. You're gonna understand the core four or personal finance three. You're going to learn how to invest $10. Until over 1000 companies were gonna make investing very easy for you. And four, you're gonna learn how to not let society confuse you with debt. Society is constantly trying to confuse you a debt, and we're gonna tell you how not to allow that to happen.

5. 05 Benfits of taking this course: the benefits of taking this course are fourfold. One. They're going to learn how you don't have to be like everyone else and work at a job you hate until you die. You will learn how to create financial freedom for yourself to you're going to learn how to invest, budget and save automatically. Investing won't be scary anymore. Three. You're going to truly understand the implications of student loans. You can skip the section if you don't have any student loans, but we know the a significant amount of users on Scotia or how student loans. And four. You're going to learn how all these companies out there just want your money. They don't want anything else. They want all the money you have. This includes Nike, Google, Apple and any company you can think of

6. 06 Why Personal Finance Matters: one of the big three reasons why personal finance matters. First and foremost, it reduces stress. You're not meant to go to bed every day, thinking about your next debt payment and feel like you're living paycheck to paycheck. That is simply not how life is supposed to be lived there, meant to sleep comfortably and soundly and enjoy life. You'll live a life free of financial stress. Once you take this course, this low stress life will lead you to being happier in this healthier. When you're healthier, you'll be spending less money on health care costs, which are also out of control in the United States. But that's not for this class. Finally, and most important to me is that you'll be able to pursue your passion and your goals, not someone else's. If you want to quit in, travel the world for a year, you can do that. If you want to learn how to surf and live in work in Sri Lanka, you'll be able to do that. You don't have to do what everyone else does. Financial freedom does not mean never having to work again. It's about working at a job you like with people you like and coming home to a life free of financial stress so you can spend time with the ones you love, like your family and friends.

7. 07 This is PERSONAL: when we want to convey a really important message, you'll see a slide like this. It's gonna be huge, and it's gonna have a very clear message on it. This one is for you to understand that personal finance is just that. It's personal. Personal means that everyone situation is going to be different. Your job is to take the learning from this course and apply them to your life. For example, some of you may want to buy a home, which may not be the best financial decision, but it's best for you and your family and your kids. Others may want to quit their job and decided to work in another field, taking a pay cut or you may have the opportunity for your dream job. So you quit your current job and take that pay cut, something I've done financially. It may not be the best decision, but for your mental health. This is by far the best decision. My personal example is I travel around the world for 2 to 3 months a year to surf snowboard in kite board. This is not financially prudent, but I do this because I love to surf and I can't surf around where I live. That's my example. Your example? Maybe buying slash financing a home. This is usually not a financially prudent idea, but it's great for your stay ability for your family.

8. 08 Live Below Your Means: Here's another key slide. The key. The personal finance is toe live below your means. It doesn't matter how much you make, because in America you'll always be able to spend more than you make in one year through the use of debt. Don't spend more than you make. If you think of yourself like a company, then you're the CEO. You're the CEO of your own company. You want to make a profit each year to make a profit. You have to spend less than you earn. We'll cover some specifics of people who are millions of dollars and filed for bankruptcy. I'll prove it to you with statistics that just because you make a lot of money doesn't mean you're financially well off. So again, don't try to show off by buying expensive cars, are big houses by what is essential for your life and will cover what essentially is, um is later on in this course, what you want is to have the freedom in the time to do what you want

9. 09 What Does Being Rich Mean: This is a quick video. So what does being rich mean to you were going to leave it open ended and want you to write down your answer on your hand out and submit it in the project gallery. It will only take a minute, but will be really interesting for us and for other students to see what you thought being rich meant before you took this class. And then after you took this class, when we made this course, these air things that we heard that make you rich, what do you think? Do you think these things make you rich? Like living in a mansion with a really nice car in a boat, making over $200,000 a year, being able to buy Louis Vuitton and Burberry close. Do those things make you rich? Let me give you an example of professional athletes. Okay. As I said earlier in this course, how much money you make doesn't really mean that much. As you can see, these professional athletes made multiple millions of dollars and you can see how many go bankrupt or are in financial stress. Within five years, almost 80% of NFL players Why? Because they live above their means. They're buying really huge houses, multiple in cars, multiple but using debt to finance them. We'll cover the difference between what owning something really means and financing something means later. But now we just want you to keep in mind that these people are living above their means and thus need to use debt to purchase these things that they have.

10. 10 High Net Worth: This is one of my favorite slides of the course. I didn't even think about net worth until I was about 25. Now you know a term that is going to be retained for you in your brain for the rest of your life. Being rich is about having a high net worth. What is net worth? Net worth is what you have left when you subtract your liabilities from your assets. If you take our budgeting, wanna one class, you'll see that so network easy example is, let's say that my house is worth $300,000. My home loan for that same house is $200,000. Then I have a net worth from my house of $100,000. You want your assets outpace your liabilities by a significant amount, and you want to grow that gap. Mawr assets and liabilities, And that's how you increase your net worth. So what are assets? Things that are worth money and hopefully go up in value over time? Think investments in your house car. Our assets has listed above, but they don't go up in value, so be careful about spending a lot of money on cars. We actually say, Don't spend very much money on cars at all. You want to increase your assets without taking on liabilities. Think about it this way. If you buy a $200,000 home and you take out $200,000 of debt to do this, did you increase your net worth at all? The answer is no, you didn't. Another example is, let's say you have $2000 worth of cash. That's an asset. But then you go by a $2000 purse or $2000 you know, TV. Did your network increase? It did not. Did it go down? Probably because that person is likely to decrease in value really quickly as you use it. Same thing with that TV. That's what happens when you buy depreciating assets. What you want to buy our assets that appreciate. We'll cover how you can increase your networks later, but in general you want to make money and then invest it so can grow. That will increase your net worth and make you rich, which means high net worth

11. 11 Netw Worth The Most Important Number: As you can see on the slide network, that's the most important personal finance number. Okay, so now let's move on to the next slide. Let's talk about two different people. Dumb Dan on the left hand side and smart Sam on the right hand side on the left. You have done Dan. He makes $200,000 a year. Good, right? Well, he has $500,000 in debt and no savings. His net worth is negative. 500,000. On the right side, you have smart Sam. He only makes $60,000 year but has been saving for a while. He has no debt and $250,000 or the savings and investments. He has a positive network of 250,000. Do you see the difference now? Dumb Dan probably looks a lot richer. He has a big house in a nice car and even a high credit score. Smart Sam looks poor to everyone, but he's the one with the high net. Worth looks will be said, deceiving as you get out of college and move on into the real world and for all of you who are currently working any millennials and people like that. You already see this. The people who look rich well, they spent cash to buy all the stuff that they have and have a low net worth. We'll talk about later. Why Feikens scores don't matter why we put them up on the screen here because they're not connected to your network at all. Which is why smart Sam has a lower FICO score but a higher net worth and looking dumb. Dan really? HaIf Eichel score and has $500,000 in debt and negative $500,000 network because FICO scores and your networks are not connected at all.

12. 12 Focus on Net Worth: The key is focused on your net worth of one of those slides that are just very, very key. Don't focus on showing off your wealth or credit scores. The number that matters the most is your net worth. You need to focus on increasing your income while keeping your expenses stagnant or even reducing your expenses. This will then allow you to have a high profit each year when your income is much higher than your expenses. You are the CEO for your own company. As CEO, you should strive to have the highest profit each year. The Onley way to do this is the Increase your income and keep your expenses low again. Focus on your network. Since then, worth is your focus. You should be careful about debt. There's no way I would be where I am without making the investment in my education. Using student loans. However, I was very careful to choose a career that would allow me to pay off all my student loans within four years. You need to really in consider the impact of debt on your life and understand how debt and that paying up interest can limit your ability to achieve your financial goals. I'm not saying all debt is bad. If you're really good with your finances, you can use debt toe leverage things. But for most people, you need to get out of debt first and then get your feeding footing down and then decide what you want to do. Make sure you're making a good investment with any debt you take out. The other key point here is earned more than you spend, which we've talked a lot about. This will allow you to invest your difference increasing your network and then allow you to find financial freedom. Next, we're gonna cover how to make your first budget. It's going to take a less than 20 minutes and make your first budget. And before we start, we have a funny music video. Make you laugh because, well, we could have covered a ton of info so far, and it's good to get some last in. Keep in mind that this class is on skill share, so just move over to my budgeting. Wanna one class? It's a separate class on skill share. Take that class and then come back here

13. Additional Info - Building a Capital Base Jenga Blocks: Okay, so let's talk about building the capital base. Let's use jingle blocks to show you the difference between people who have a negative net worth Ah, high net worth and a low network. So you can see here that the red blocks the red Jenga blocks do not represent some truth or dare Jenga game. The red blocks represent debt. The green blocks represent income or assets. So off to the left you see somebody with negative net worth because they have a lot more debt than they have. Incoming will go over through the details in a second in the middle. You see somebody with the high network. They have tons of different income, starting with an emergency. Fine. And then it screw. You find in a bunch of different other types of income in savings. And then finally, you have somebody who is off the right, which is a representation of my parents who have a low network. But they don't have any debt whatsoever. So these are the three different blocks to give you a visual analogy off negative net worth off to the left in the Middle high network and on the right hand side, low net worth

14. Additional Info 2 Detail Review of Blocks: So let's go through the detail of somebody was negative net worth. So on negative net worth. What you can see here is that you have your main job, which supports your car debt, your house debt, Moorhouse debt, credit cards and student loans. You can actually think of this as somebody who just graduated, right? They graduate. They have one job. They get a car to get a house they can't afford. These two have credit cards, and they still haven't paid off their student loans. This is not different from the average American. So what about somebody with high net worth? Right. So let's look at the details of somebody with high net worth you would see at the bottom there, and we'll talk more about what an emergency fund is and its crew you find. But those are two things that are buttress thing in their staff. Then you look into it, and they have a 41 K savings. They have more savings. On top of that, they have dividend income as an extra stream of income. They have one side hustle. Maybe it's a rental property. They have another side hustle. Maybe it's a business that they run on the side and then they have their main job at the top. And in this case we added a little bit of debt. Maybe they have $5000 a car net. Obviously, they can paid off really easily. And then finally, let's talk about somebody with low network somebody like my parents. They're refugees. They didn't have a college education, but what they didn't have is any debt. So we look at their stack. They have a 41 K at the bottom a side hustle, which is a rental house, and they have their main job.

15. Additional Info 3 Negative Net Worth and Lose Your Job: in finance. We do this thing called scenario analysis. What we say is what happens if this thing happened. So it's kind of life. If you're a computer science major and if then statement if this then this. In this case, we're to see what happens if you're negative network and you lose your job so we can see the stacks here again. Main job is at the bottom are looking at the left hand stack of Jenga blocks, right, tons of debt and one job holding all so we see what happens whenever you lose your main job and you have a ton of debt, your entire Jenga block comes crashing down. And that's what we want to prevent. Because what happens when all of its being buttressed by one job and supported by one job, not on Lee. If you lose your job, everything comes crashing down. If you break your leg, you think you're gonna call out of work. If something goes wrong? Do you think you're gonna call out of work? No. And how do you sleep? You're gonna have so much stress because you know that if you lose your job, everything comes crashing down. And again. This is that average American, Which is why we're trying to prevent this for you.

16. Additional Info 4 Green and Lose Your Job: now moving on to high and low net worth. Same scenario, and you lose your job, right? You lose some income. It's pretty obvious to know what's gonna happen here. Let's go through the video, but you'll see what happens. So you see here that you lose some income. You're okay because you have so many other income blocks. And if you lose your main job in your low net worth, what happens, you're okay as well. So my parents were tired and they have a rental house property supporting them, and they have savings as well. So that's the thing when you're high that weren't in your low network with no debt, something could go wrong and you're okay. And that's the's air. The to this acts that we want you to be as you head out of college. So pay off your student loans if you have any as soon as possible and avoid taking on any additional debt

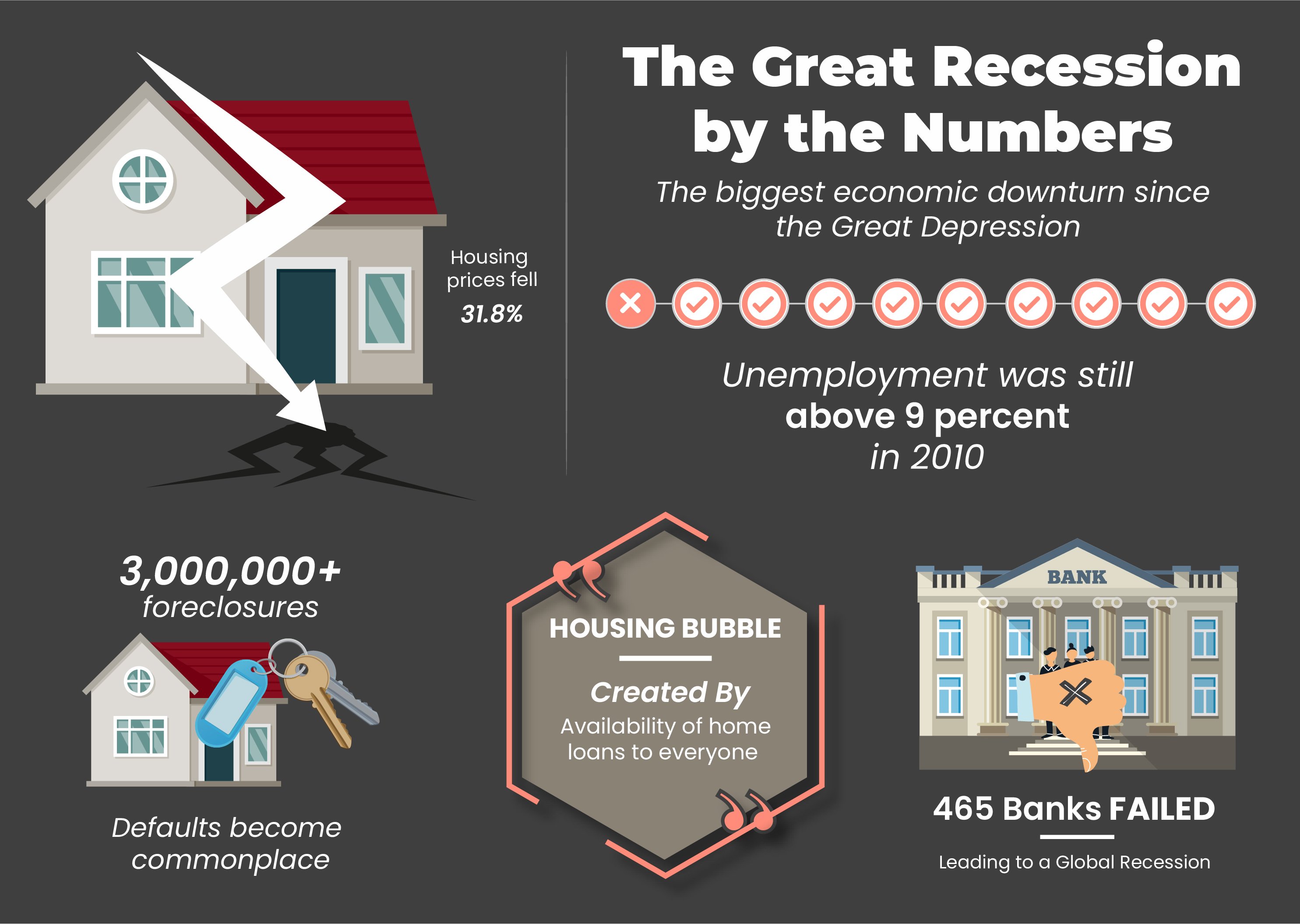

17. Understanding At Will Employment: So what's really important here? Okay, you get really passionate about this subject because it's really important to understand what is at will employment means in America. Almost every job is at will, which means you can get fired for any reason at any time. Okay, I could get fired for learning a blue shirt. I could get fired for coming into late three minutes late. I could get fired for coming in early. Actually, there are so many reasons I could get fired. I can get fired for cursing. All of those things are allowable reasons to get fired, and what you have to understand is in big, bold letters. Here, your job is not guaranteed. It's really important to understand that at all times, especially during a recession, because what companies are gonna try to do is maximized profit. So either make more money or what's in really easy thing to do is cut your costs where most companies cost people. Okay, so it's really important that you understand at will. Employment means your job is not guaranteed, and you could lose your job tomorrow and what we saw during 9 11 what we saw during the great recession in 2008 is that tons of people lost their jobs. Didn't matter if you're working for Lehman Brothers or United Airlines. People were losing their jobs left and right, and that's likely to happen again in 2021. We're entering this recession. Even if we get out of this recession, you have to understand your job is not guaranteed and you can be fired for any reason as long it's not illegal at any time.

18. 13 Intro to The Core Four: So you already took the budgeting one on one class. Now, if you have not, you got to go take it. It takes 19 minutes, so get your budget from start to finish. Use the brainy money sheet or use mint dot com. I'm a huge fan of mint dot com. We're not gonna walk through mint dot com. There's no reason to do that. You can just log into min dot com and learn how to use it on your own. It's really not that tough, so we recommend mint dot com or brainy money. She'd either way, you should have your first budget before you keep moving on. Now that you've created your first budget, you know where you stand on a monthly basis. Let's talk about the core four or personal finance first, earned more money than you spend and create a $1000 emergency fund. Second, pay off all your debt, starting with the highest interest rate debt 1st 3rd culture spending By practicing essential ism, this is pretty easy to understand. What do you actually need to buy? What do you actually need in fourth? Invest $10 a month using betterment or your other 41 K So some people have a 41 K Some people don't so use your $10 a month to invest, and you can use your 41 K or use betterment, which we're gonna work going to recommend, and we get no kickbacks from betterment. We recommend betterment because we believe it is the best product out there. It's the absolutely the best tool, and again we don't receive any compensation from recommending them. We use them, and it's literally the best tool because it's simple to use and makes easy to invest small dollar amounts. We don't want you to start investing a lot of money. We want you to learn how to invest and then put more money in as you gain confidence. So don't be afraid, because it's only $10 there's no need to fret. We we will explain what investing in an index fund is later on, using a game called Monopoly, just know you'll be investing $10 in over 500 companies. Thes air pretty self explanatory in general, but the details here matter. Why are these the core for and what do we really mean by them? We're going to cover that detail later on in this class. But I wanted to give you a glimpse off what the core four personal finance are.

19. 14 Financing vs: So what's the difference between financing something and owning something moving to the next slide? You're going to see how society confuses us. Society confuses us a lot. This is how they get us to spend all of our money and take on massive amounts of debt. It's not that you're stupid or I'm stupid. It's that society confuses us because these company want all of our money. The biggest way society confuses us relates the financing versus owning another key slide here. Financing does not equal own financing. Something does not mean you own it. If I buy a car and I put zero down and just sign a piece of paper, do I own that car? What happens if I put it a 1% down payment on that car? I own 1% of that car. The remainder of the car is owned by the big. Same goes for houses. People put 5% down on a house, and they say they are. They are homeowners on Facebook or Instagram of whatever. They only home 5% of that house. However, by saying that they are homeowners, they feel really proud and that that makes that banks really happy because they could start making lots of money off of them by earning interest off of the homeowners are the home buyers. The bank doesn't care that you think you own your house, but you really only own 5%. They're making money hand over fist on how much interest that you're paying on that. So now let's go to your hand out. And the first question to ask yourself or a relative is Do you own your house? So, on your handout, ask yourself this. Do you own your house and write that answer down? This is gonna be really important as we upload into the project gallery. Are you still making payments on your house? Okay. Ask yourself that question. Here's the catch. If you are still making payments on your house, then you don't own your house. You are making payments to the owner of the house, which is the bank. You own x percent of that house. Maybe 5%. Maybe 10%. Maybe 2%. But you don't own the house outright. This is the difference from owning a home and financing a home. Do you see the difference now? Do you see how society confuses us. Let's move on to the next slide. Second question. Ask yourself a relative. Do you own your car? Take the same four steps on your hand out for skill share. Do you own your car? Right that answer down. Hopefully you own your car. When I worked at CarMax in college that pay for school, I found that many people never paid off their cars. So if you write, you write it down, then ask yourself if you're making payments. If you're still making payments than the bank is the true owner of the car. Think about this. If you stop making payments on your house or if you stop making payments on your car, what happens? Someone will repo your car or they will kick you out of your house. That's how you don't you know. You don't own either of them if you're still making payments on them. I understand that I sound very passionate about this, but this is the biggest thing Society confuses people on

20. 15 How People Buy such Expensive Cars: So you may ask yourself, then why do you see so many people driving so many nice cars and living in these really nice houses? But I'm telling you, the average American doesn't have $500 right? That's the commented dissonance. How do you reconcile this? The really the way you can reconcile it is because people just take out longer and longer loans and focus on monthly payments. Bank's make more money, dealerships will sell more cars, and the average American loses even more money trying to keep up with everyone else. So what you can see here is that follow my mouth. Okay, look, a $41,000 car is how much your purchasing, if you include the interest. So we're buying a $40,000 car, and this is how many years we're gonna finance it over. If we finance it over one year, our monthly payments $3000. $3500 right? No one can afford that. Are most people cannot. But look, if I goto eight years, this red numbers my new monthly payment. I'm paying $526 a month. But look how much in the blue. How much. I'm paying an interest. I'm paying $10,000 on interest on a $40,000 car. I'm paying $50,000 in total for a car that in eight years is not gonna be worth nearly that much. So now you can tell yourself and explain to yourself when people drive really nice callers all they're doing guys ladies out there is. All they're doing is extending the number of monthly payments they're going from 12 monthly payments to 96 monthly payments going from one year to eight years. Don't pay that car off in a decade. That's horrible. That's how they focus on monthly payments, and that's how they look rich.

21. 16 Core Principal 1 Earn more Than You Spend : So let's revisit the core for personal finance and go into the details. Now go to your hand out and get ready to take notes. Now that you created your first budget, you know where you stand on a monthly basis. Let's talk about the core four personal finance again just to refresh one earned more than you spend and create a $1000 emergency fund to pay off all your debt, starting with the highest interest rate debt First. Three. Cut your spending by practicing essential ism and four. Invest $10 a month through your 41 K or betterment. So let's dive into core principle. One. Earn more than you spend and create a $1000 emergency fund. Okay, it's pretty obvious, but most people don't do this. You make a certain amount of money each year, and let's say you take home after taxes $40,000 a year. Then you should spend less than that every year because you are the CEO of your own company and you want to make a profit each year. It's that simple. Okay, second, you need to create a $1000 emergency fund. Why? So you can learn how to save because you need to cover any emergency. One thing you should know is that 60% of Americans don't have $500 in savings, so you'll be ahead of 60% of Americans if you just do this one step. How crazy is that? This is core principle number one. Finally, you should take on a second hustle or second income stream. This will allow you to make more money and then save even Mawr each month, this side hustle or second income stream, and we'll talk about that on the next complice lines.

22. 17 Side Hustles : So what we're gonna focus on now is earning more in spending less. Okay. How many hours do you spend a week watching Netflix or TV? Write that down and think about it. Instead of doing those things, you could be building skills like on skill share. Okay, you can be building skills on how to code or whatever, like how to make more our design. Freelance art. Learn how to manage your money like you are doing right now. But you could be building so many other skills. They're different modalities to accomplish your goals. OK, so what you could do is increase your income by getting a second job or a side hustle. Rent out your space or room on Airbnb or turn your hobby into a second income. Personal finance used to be in my hobby. It still is, and I've turned it into a side business. Okay, and that's what I do. One skill share is I actually earn money by you watching this course and by helping other students out. And I love that. The other thing you need to do is decrease your expenses. You can use your budget to determine what you are spending your money on and reduce those expenses. Some easy ways to do this are just spending less money running a smaller place when you when you releases up keeping your car for a really long time. I took my girlfriend to get her car detailed, and she was like, Son, it looks like it's brand new. That's true. We will talk about detail in your car once a year, making your own food, using life hacks like getting on family plans for monthly services. So think about Spotify, Netflix, Disney, plus all of those things you can share with your family members. A big thing here is a side hustle. Big take away slide. Just start and do something. Okay? You may work full time, but you need to find work on a side. So that's a side hustle. Just start and do something this week. Maybe you won't make much money at all or anything, but you're going to learn a lot and will eventually increase your income. You're gonna learn a lot from this, no matter what. When you're working full time, it's really important to have one side hustle so you can keep building your skills but hopefully it's something you love to do. Currently teaching personal finance online is a side also mine. I spend many weekends and nights. Today's a Saturday when I'm recording this video because I love it. I honestly love what I do. So this is a side hustle, but I genuinely do love it. Eventually, this will probably become my full time gig, but for right now it's awesome to do on the nights and on the weekends. So here are some examples of websites and companies that you know you have this printed out now that it can help you make money on the side. Once you have a skill that people will pay for and there are a 1,000,000 things people are willing to pay for, you could teach on skill share. Tutor up work dot com rover dot com Uber uber eats selling items on eBay photography I buy stock photos, consulting of any type. I do financial consulting, so those are all things you can do. Teoh work on your side, hustle and make more money

23. HustleVida.com = Cool website!: so I've gotten a lot of questions from students. About one are possible side hustles and a quiz that maybe help them out. And we found this really great website. Hustle vita dot com. So it's H u S t a t l e v i d a dot com. You can see the link up here. Hustle vita dot com. We found that's really great website that list a bunch of different jobs you could do so you can work. You can rent things, or you can sell things as your side hustles. They have a tip sections, Ah, blawg quiz and some tools. But like, for example, if I goto would work and then I go to Beauty, for example, I click down here. It gives me different options. Even with the Hustle Vita score, apparently that tells you how good it is, so you could just read more about it. Learn more about what it is. So style Seat is a marketing and payment platform for hairstylist, Medicare's makeup artists and barbers. It's really, really great, and we messed around with the quizas well, so click quiz and it says what kind of solo premier, a producer are you? And then you can start answering questions around it. So again, hustle vita dot com. You can take the quiz if you want to, but it gives a lot of really great options to find the best money making option for you. So the best side hustle toe you choose your own hustle. Can you work? You want to sell? Do you rent things? Has tools and a quiz. So it's a really great website that we found, and we highly recommend it. So hustle vita dot com h u S t l e vita the i d a dot com

24. 18 Emergency Fund = Screw You Fund: So now we focused on earning more. Let's focus on this emergency fund. When I told you to create a $1000 emergency fund that's for small emergencies, thinking about like, Hey, I need to get four new tires. One of the things that one of my grad school professors told me was, how important a screw you fund is? What is a screw you fund? It's at least six months of living expenses saved up in cash. Essentially, if you don't want, like your job anymore for any reason you can leave and walk out. It doesn't have to be that dramatic, either. The most simple I example I have is, Let's say you live in a big city like Houston. Your company's moves their headquarters from one side of Houston to the other. If you've ever been to Houston or any major city, you know how big a deal that is. This could easily make your commute double, and you could be driving four hours a day, two hours each way. Do you want to say at that job personally, I would not, and I would use my screw you fund. I would say Look, I'm leaving and I'm looking for another job. I would think most people would actually say No, I'm not going to move in Drive four hours a day. That's the importance of a screw you fund. This is something I teach because of how important it is. Later on, you'll want six months of living expenses saved up in a liquid cash account. That way you can quit whenever you want, and if you get fired, you're good, too. You never know when you could possibly get laid off, get fired or your company's headquarters move, or so many a multitude of other things could happen where you want to quit your job. In the end, this gives you massive peace of mind. It's how I sleep so well. I don't care what happens at work because I know I'll be fine for several years without working

25. 19 Core Principal 2 Pay Off All Your Debt: The second core principle is the pay off all your debts, starting with the highest interest rate debt first. Why? Because paying interest is the biggest barrier to building your net worth. You are literally losing money in your asleep interest expense. Accrues while you sleep, and you're never going to be able to build a high network. If you lose money while you sleep, you should be making money while you sleep. Pay off all of your debt, use your hand out and write down all your debt that you have. And I know this can be scary so you can do this in your hand out. But you should have already done this in the budgeting one on one class. That's why it's so important to take that class on skill share. Then, after you've written down all your debt, find the interest rate for each one of these types of debt. Your debt may include student loan debt, car debt, house debt and credit card debt. Rank them from highest interest rate to lowest interest rate. You need to pay off all your debt for the highest interest rate debt and then move down the list to the next highest and the next highest in the next highest interest rate debt. So you start from the highest interest rate, and you go to the lowest interest rate. Pay them off one by one. In practice, this usually works by paying off credit cards and payday loans first, then moving on to student loans, car loans. And finally, your house loan should generally be your lowest interest rate. Okay, so, again, to recap if you follow my mouth, pay off all your debt, starting with the highest interest rate that first avoid credit cards. So until you have all your debt paid off, you got a you know, avoid them. And if you if you decide to have one, you need to pay it off every week, using it just like a debit card. If you cannot pay off your credit card every week, you need to get rid of it. And then we already talked about how it works in practice and don't get discouraged. Even small amounts of payments against your debt will have a big impact later on

26. 20 Incentives For Banks Explained: How are incentives for banks work? Okay, incentives for banks work like this. Banks want to charge you as much interest as possible. Okay, That's why current cards have a 25% interest rate. Houses have a 5%. Interesting as much as they possibly can. They want to charge you as high as interest rate as possible is legally allowable. That's what they want to do. Then they want to borrow money from you and pay you nothing for it. If you don't believe me, go ahead and go to chase dot com and look up what their interest rate to pay you is. If you put in five $100,000 into a checking account, it is usually less than 1%. So they're gonna pay you less than 1%. But if you go back and then borrow money from the bank, if you're buying a car, the bank the interest rate should be between five and 10%. If it's a credit card, 25% interest rates are very common. So what you're going to see years? The incentive for the bank is a gonna borrow money from you at 1% interest rate and they're gonna loan it back to you at between five and 30% interest rates. Okay, that their incentive. That's why they want you to take out loans for cars, take out loans for houses, use credit cards because all of these things allow them to make massive amounts of money off of you without doing anything.

27. 21 Core Principal 3 : the third pillar our personal finance is practicing. Essential is, um, this is directly connected to living below your means. Essential ism is asking yourself what you actually need versus what you want. A big example for me is you need a car. Do you actually need a car or can you take the bus depending on where your job is, You may need actual car if you can. Can you drive a 10 year old Honda Civic? That is really reliable? Would that work? Or do you need the new truck that cost 40 or $50,000? This is what essential ism is asking yourself what you actually need versus what you want, focusing on big items or where you really want to start. So think about housing. Can you live with a roommate or in a small house? Do you really need a 2000 square foot or 3000 square foot house when you're living alone or just with your partner and transportation? Can you buy a cheaper car? That is just a reliable Other things you should think about are finding free ways to have fun. There are so many freeways out fine Mike Girlfriend did the calm. You know, they Santiago, which he spent biking for almost a month, staying at hostels in Spain. She pretty much has paid for the flight, and the rest was sheep. There so many ways to have fun. My girlfriend and I walk our dogs several times a week at the local park, and we love it. It costs us nothing. Focus on what is truly essential. For example, I only own five work shirts because that's all I need. I don't need 50 work shirts. There's no point, and it just costs money. I'd rather not buy those shirts and invest the money. Finally, avoid lifestyle inflation, which we will explain in our next video. When you get a raise, don't go buy a new car and upgrade your house. Then you will never be able to create a profit because as your income just increased your expenses, just increase. That's what lifestyle inflation is and why we're gonna explode it in the next video

28. 22 Lifestyle Inflation Animation: So what is lifestyle inflation To explain lifestyle inflation? I'll tell you a quick story. Me cross. He's 22 years old and just got his first job. He's been skimping on nice meals and has had roommates the last four years. After he gets his first job, he decided to buy a brand new car and moved into a nicer apartment. His current vibrio old Toyota Camry has had no problems. He just wants a nicer car. No problem, right? Well, fast forward. Three years and now Ross's 25. He gets his first raise, and he decided to trade his car in again to get a luxury car. He decides a one bedroom isn't nice enough, either, and decides of finance an entire town hall in the city that is three bedrooms and two baths . Even though he is just a scene guy. He wants to impress girls, and he believes that upgrading his lifestyle will make him happier. However, he feels like he's living paycheck to paycheck. Despite making significantly more than he did three years ago. Ross is actually more stressed now about his finances and realizes he doesn't need all this nice stuff but is now stuck with a large carpet in a large house. This is what we call lifestyle inflation. It occurs when your income increases, but so does your lifestyle. You get a $10,000 raise, but you immediately by a brand new car that costs $50,000 south. Familiar? It should, because many Americans deal with. According to a Harris Poll survey, 78% of Americans feel like they are living paycheck to paycheck. This affects everyone, including people making more than $100,000 a year. This also affects the majority of professional athletes who filed for bankruptcy within five years of retirement. No one isn't means falling prey to lifestyle in place. So to summarize lifestyle inflation is when you upgrade your lifestyle every time you get a raise, assuming it will increase your happiness. This in turn creates financial stress because you always feel like you are living paycheck to paycheck. Here's a secret. Upgrading your lifestyle increases your happiness for a month or so, and then your happiness level regresses back to meet its called the Madonna Trent. Feel free to look it up. The solution to the lifestyle inflation problem is to create garnering that won't allow you to increase your spending with every raise. The best way to do this is to increase your automatic savings deduction, which is usually your for one for every raise you get. Did you get a 5% raise? Increase your savings percentage 55% 2 years later, it get a 10% raise. Increase your automatic savings percent by another 10%. This will force you to live within your means. I personally do this through two different ways. I used to increase my 41 K automatic deduction, but I maxed out on my 41 K deduction, so my next step was increased my tax withholding percentage for each race. It doesn't matter which savings account used in American Express Online savings account for one K Roth IRA or increasing your tax withholding. Use any of these accounts that put your paycheck into a savings and not into your checking account. Putting it into your checking account will allow you to spend. The key to the savings account is that it must not be easily accessible. This will prevent you from spending all the money in your savings account when you have an impulse purchase evidence to easily excessive increasing your automatic savings every time you get a raise. Prevents lifestyle inflation because for every raise I've received over the past five years , my net pay check stays the same. Yes, I get a big refund at the end of the year, but I just invest this money. Thistle is probably the biggest tip I can give you when it comes to personal finance, and this is probably the biggest reason why I'm financially independent at such a young. It's like pursue mission driven jobs and do what I love, like making this class and cool animated video like this. So revisiting Ross a story, he should save the majority of this raises by increasing his 41 K contributions. Instead of buying a new fancy car or house, he doesn't

29. 23 Core Principal 4 Invest 10 a month through Betterment: the last core principle is investing $10 a month. Why $10? Because it's a small amount that everyone on skill share can afford. You should invest more, but let's just get started with 10,010 $10. This is really small amount of money, which will teach you how to invest and what investing is. Most importantly, it's going to remove the veil of fear. Everyone thinks investing is scary, and I'm going to show you that it's not at all we're going. Invest $10 not in one company but in 1000 cos we're not only going to invest in stocks, but we're going to invest in bonds to How is all this possible? Because another CF A started a company called Betterment, and it's one of the most amazing companies out there. They're a robo advisor, which means they use technology to make things super cheap for you to invest. And, yes, you only need $10 to start. To be honest, if you truly don't have $10 please go find $10 to invest. That's what you need to do. What you'll see is that the richest Americans are heavily invested in the stock market, and that's why I want you to start investing now as well. This is one really important way to build your network. In the next section, we'll explain what an index fund is and how you could invest in over 500 companies would just $10.

30. Only Invest What You Can Lose: so one thing that we wanted to add to our investing courses. This you should only invest what you can lose as you see in this recession in 2020. And we have a recession class now, So please take it is that you can lose a lot of money. So when we talk about risk tolerance in the market going down 30% it's done that do not invest money you cannot lose. Okay, So to invest in the stock market, you have to hire, have a high risk tolerance. So if you cannot lose that money, do not invest those dollars. I cannot stress that enough. I have a lot of money in the stock market. It's gone down 30%. But as I've said, I have a long time arising. I'm very young, so I don't care that it went down. I'm actually investing Mawr, but for you, if you cannot stand to lose those dollars or if you need them for whatever to buy a home or whatever, you should not be investing. I cannot stress that enough. During Cove in 19

31. Investing is not gambling but you can lose money: another keys take away slide here. Investing is not gambling, and it's not scary. Okay, so we want you don't understand that. And we're gonna use Monopoly to help you understand what investing is like. Okay, so on the next slide, you'll see that this is Monopoly. So here's Monopoly. Everyone knows this game. If you don't. The purpose of the game is a by oppa's many properties. Okay, follow my mouth. All these properties here, you wanna buy as many properties, you can go bankrupt. All the players, when they land on your spot, they land on your slot, they pay you rent, then you have all the money, and everyone else has nothing. Each of one of these faces represent a property. Okay, let's focus on the property everyone wants. Look to the right here, and that's boardwalk. If I ask you to want, If you want to own for Boardwalk, what would you say? Most people would say, Yeah, but you condone boardwalk. And because there are 40 spaces on the monopoly board, there's a 2.5% chance that someone lands on. That's not exactly right, but it'll work for this example. So you have a 2.5% chance of somebody landing on Boardwalk. Now let's say I give you the option. Toe own 10% off every property on the monopoly board. So you own 10% of Pennsylvania Avenue, 10% of North Carolina, 10% of Pacific Avenue, 10% New York Tennessee ST. James Place. You own 10% of everyone, including Boardwalk and Park Place. Would you rather own 10% of every property on the monopoly board or 100% of Boardwalk? Hopefully, your answers. 10% of every property on a monopoly board. That's the difference between gambling and investing. Gambling is betting on one company. Let's say Apple or Netflix to do really well. Investing is saying I own a small percentage of the top 500 companies in the United States . That way, when any of these companies being money you to you will as well defining the term index fund, an index fund is like owning 10% of every property on the Monopoly board. You own a small percentage, also known as a share of each property. That's what we recommend investing in an index fund run by Vanguard and you can invest in these two betterment. No. You know, now you know something that most American Americans will never understand wanted index fund is and how it actually works. This is gonna be a very short video. The rich on the S and P 500 which are the top 500 companies in the United States. As you can see, percent of us hustle toning $10,000 in Warren stock by wealth class top 1%. 94%. The bottom quintile. 4%. So you can see the rich owned the S and P 500. And that's why I'm telling you to investment s and P 500 through betterment.

32. 25 The Power of Compounding Interest: so the title of the slide is starting early in calm, pounding interest. If you know you're a little bit older than an average person, look, starting now is what's important if you're young and you're like, just out of college, start early and it's gonna change your life. Okay, so let's move on to the next slide here. Key to investing is to grow. It needs time. 10 plus years. Okay, If you want to grow anything and plant or your salary, nothing happens overnight. Even Facebook did not happen overnight. Just like anything to grow your investments, you need to give it time. And when I say time, I mean at least 10 years, the strategy is easy. When we talked about it, invest in the 500 largest companies in the United States and wait, that's it. Don't do anything. Keep investing and give it time. The reason why it takes time and patience is because your earnings need to compound. This means that your money will start making money on itself. We will do a quick Google sheet together to show you how compound interest works, but just understand that you need to leave it there you cannot take the money out and spend it and expect it to grow. Obviously, that's not going toe work. So hopefully there are a lot of things mentioned so far that are truly going to change your life, for example, learning what net worth is. And that was what the definition of being rich is, is having, Ah, high net worth. This chart will hopefully change your life. In summary, it shows two different people one person who starts investing seven years earlier and then stops investing altogether. The other person waits until they're 27 to start investing and never stops. What you will learn from this chart is that the more time you give your money to grow, that better off you are. It's not always how much you put in. It's the amount of time that it goes untouched is allowed to grow. If this chart doesn't completely change your view on saving and investing, I don't know what else to say. To be honest, I mean, look, the person who invested from age 19 to 26 on Lee put in 16,000 of their own dollars and walked out with a 1,000,000 age 27 to 65. That's how long they invested. They put $78,000 in, and they walked out with almost $200,000 less because of compound interest.

33. 26 Types of Savings Accounts: it's important to know about the different types of savings accounts. You should have two types of savings accounts retirement counts which are to be used decades from now. OK, and thats in this yellow here, on the left hand side, you can see retirement accounts and yellow, and then on the right hand side are the current savings. Okay. And that's in case you need it right now in the green shaded box. Okay, On the right hand side, you can see the green shaded box. You have your emergency fund and your screw you fund all in an online savings and council. You can easily get to it. This is your current savings on the left. Inside, you see your retirement accounts. Long time from now. This you could never touch. You can. But there's a huge penalties related to a pretax retirement accounts and post tax, which will talk about on the next slide. So on the next line focusing on the left hand box, you will see that there are two types of recurrent retirement accounts pretax right here and then post tax right here on the right. What that means is that when the money comes out of your paycheck. If the money comes out of your paycheck before you get your paycheck. That's called pre tax. If the money comes out after you get your check, that's called post tax. As I don't want to overwhelm you with information, I want you to focus on your 41 K You're pretty tax accounts. Start saving money in those accounts. Now, if you are contributing anything to these accounts, start with $10 a month. Start saving $10 a month into your for a one k this week. If you don't have access to a 41 K or if you're a government job for 57 B, then create a Roth IRA account using betterment and invest $10 a month into that account. Traditional IRAs and Roth IRAs offer different tax benefits, but I don't want to get into that right now. I want you to focus on saving $10 a month and then taking my advanced personal finance class to learn the difference of differences between all types of retirement accounts. What I don't want you to do is to get overwhelmed with information and don't do anything so go to betterment and create a Roth IRA account and save $10 a month. If you have access to a 41 K and you aren't investing in one right now, start with $10 a month. Contact your HR department to get this set up. The last reason why I ask you to start with $10 a month is because you cannot touch these amounts for at least 10 years. So I want you to start with a small number $10 a month right now and then increased out of Mount over time when you have more confidence that you can say more than $10 a month. But again everyone should be able to save $10 a month. Everyone should be able to save $10 a month and not need it for 10 plus years. Now let's focus on the writing inside, which is a for current savings. It's a lot easier to set up because this is all money that is saved after you receive your paycheck, so focusing on the writing inside you should open up an online savings account. I use American Express online savings because it's easy to set up and Frito have. Plus, you're gonna multiple savings accounts again. We receive no compensation for recommending them. Go with any online savings account. With the high interest rate, no fees. You could easily google it and find one. But American Express online savings are really easy to open. That said, open up an account, but your savings in there you have two accounts, one called emergency fund. There you'll put $1000. And after you say that $1000 you will start saving six months of living expenses in the other account. Check your budget. See how much you spend each month. Multiply that amount by six and that will be your amount in this crew. You fund account as an example. Say my monthly expenses from my brainy money spreadsheet. My budgeting wanna one class for house car food and everything else is $2000 a month. Then, mathematically, I need six months times $2000 a month that I spend. I need put $12,000 into my screw you fund account. So have access to that whenever I need it, okay, and that's what's really important. I personally have both of these, but my screw you. Fund is actually about 24 months of savings saved up because I don't want to make sure that I'm not in any weird situation that I have to work. I know that I could walk away from my job and walk away from everything for these two years and be OK.

34. 27 401K and IRA Basics: so they're the basics of a 41 K It's a retirement plan where you can put your money away and avoid taxes for the year. You'll eventually pay taxes when you take the money out. But that's so long term from now. Let's get not get caught up in those details. It's a savings vehicle. It works really well because you can set aside part of your paycheck and never see that money. That means if I contribute $10 a month into my floor one K, then I will never get that $10 in my paycheck. I don't have to decide each month a save. That decision is where things can get really screwy because my savings will happen automatically. That's the best part. Your money will go into your 41 K before you even get to see it. That's the key to getting ahead. Automate your savings so you never see the money. You will learn how to live without that money, I promise you. In addition, there are usually employer matching. Ask your HR department if they match any contributions. If they do, you need to put at least that amount in your 41 K Therefore, if they match up to $1000 then you need to put in $1000 each year because that is absolutely free money. Ask your HR department if they match anything in your 41 K Finally, look to investor for one K into Vanguard funds because those have the lowest fees. Look for S and P 500 index fund or something similar to that. On the next line, we'll see what IRA basics are. Let's cover the difference between Roth and traditional IRAs. IRA stand for individual retirement accounts With both of these, you get your paycheck, then you decide to put your money to your Roth or a traditional IRA. You also get to decide how to invest these funds, However you wish. If you qualify for a Roth IRA, I recommend it because you can take your money out of a Roth IRA whenever you want without pendency, because you've already paid taxes on those amounts before you put money in when I say qualify. If you make over a certain amount of money, check Google. You can no longer use a Roth IRA Day or traditional IRA. Traditional IRAs reduce your taxable income for the year, but you have to pay taxes when you take the money out if you don't qualify for either focusing on maximising your 41 K For most people, I would say this is good information, but focusing on contributing as much as you can into your 41 K is the best thing you can do this. This section is mainly for people who don't have access to a 41 K If you don't have access to a 41 K use one of these IRA accounts.

35. 28 Lets Invest $10 with Betterment: So what I want you to do now is go to betterment and actually invest $10 goto betterment dot com or Google betterment. It's very, very straightforward, so we don't need to do that together. I want to cover understanding, betterment. Let's talk about betterment and why are recommended again. We don't receive any compensation for recommending betterment. First, you can start with a really tiny amount of money. Anyone? Everyone has $10 a month to start investing with. I love betterment because you can start with such a small amount of money so you can learn for or learn about it yourself to its simple and efficient. It's one of the most simple tools out there. It will take you through a step by step process on investing and does it all using a great our of them. Three. It's truly advanced investing and not gambling. Betterment will investor $10 into thousands of companies across the United States. It's truly awesome. You're buying a small part of every property on the Monopoly board. Fourth, they are incredibly low fees. You have to be careful about all these companies out there, and we checked better mints fees and they're the only 1/4 of a percent. Finally, that leaves you with no excuses. Betterment removes all barriers and all excuses. You have the knowledge. Betterment has the tools for you to invest. Now it's up to you to do it.

36. 29 Automate Your Finances: how to automate your finances. Automation makes financial management very, very easy. Okay, automation of your finances is very important. The reason is because if you're given the choice that saver spend every day you will likely spend you had a choice. You have to remove the choice of being able to spend money from the equation. Don't even allow yourself the choice. Automation means that you will never see the money. It automatically goes into your 41 K or other savings accounts. Everyone believes that if they're given the choice, they will say. But we all know that's not true because 60% of Americans can't even come up with $500 in savings tomorrow. What I'm teaching you is that your irrational and that's okay, I'm irrational as well. If money comes into my checking account, I will immediately spend it. That's why I automatically have money taken out of my paycheck and directly into savings accounts. I never see this money and thus never have the opportunity to spend it. And since I don't take out any debt, I never spend what I don't have. The only thing that comes into my checking account each month is what I have to spend. I end up spending literally every dollar, but that's OK because I've saved everything I needed to before any money got deposited it into my checking account. Thus, the key take away from the slides are save it, invest automatically, which we've talked about. This includes automatic 41 K deductions. Automate all your bill payments. You can set up online building made payments or everything. Now it's not 1995 finally, and this is key. If you use your credit card, pay it off every 2 to 3 days. You're probably like Son. That sounds insane. It is honestly, but it will prevent you from overspending if you pay off your credit card every 2 to 3 days , then you'll use it like a Democrat debit card and never overspend and never get into a situation which were paying a bank. Massive amounts of interest 20 and 30%

37. 30 Long Term Savings Rate Goal: so your savings goal should be 10% of your paycheck. That's how much should be saved. We start with $10 a month, Okay? Because we need you to do something. Now you've got to take action. Now, as you get more confident, you should move up from $10 a month to $100 a month to eventually 10% of your entire paycheck should be saved. Neither your 41 K or some sort of other savings vehicle. So now you know your goal is 10%. Personally, I will tell you this. I save over 40% of my income. That's not your goal off the bat. That's too overwhelming. Your goal right now, say, $10 a month with betterment or through your 41 K

38. 31 Credit Scores Debunked: so we've covered a lot of information so far. It's an amazing amount of information. You're still far ahead of every other American out there. So thank God for this kosher glass. Really? Now we're gonna focus on credit scores and some other miss out there. Okay, so going on to the next slide, you'll see that your credit score doesn't really matter. People always talk about carnet scores because that's what major banks want you to be focused on because credit scores are a measure of how likely you're gonna pay back debt. But you shouldn't really be focused on debt. You need to get rid of your debt. You should focus on your network if you're focused on debt and taking out more debt and paying back that death, and you're just paying tons of interest. Banks want you to focus on your credit score because that just means you're paying lots of interest. Remember, our goal is to avoid interest expense making minimum monthly payments on your debt keeps your credit score high. Don't focus. Under credit scores, focus on your net worth moving on to the next line. Things that won't change your credit score so you can actually see your credit Score is made up of payment history, credit mix, length of credit history and new credit. Okay, it does not take your network into consideration. So, for example, if I give you $5 million your credit score won't change. If your income increases by 100 times, your credit score won't change. Vicryl scores do not take into consideration network and Onley takes into account payment history and the things listed toe left here, which is amounts old payment history Credit Mixed link. The length of credit history. New credit. Higher FICO scores are generally tied to how much interest you paid over your life. The mawr interest. You pay the banks, the higher if Eichel score will be as long as you're making on your payments. So what I'm trying to tell you as that you need to increase your net worth and not worry about your credit score. So here's some key takeaways for credit scores. If you want a higher credit scores. And here in the Big Bold, it's easy. Just pay off all your debt. Okay, your goals that have no debt, a high net worth in the high credit score by the time you're 30 again. Biggest. Take away here. You can read all this stuff, but the net worth your network is the most important metric. Nothing else. Your net worth is the most important metric.

39. 32 Understanding Student Loans: Now that we've covered credit scores, let's go over student loans. A lot of people have student loans. If you don't just get this section, it's only a few minutes. So we're not gonna go into a deep dive. So truly understanding student loans. Spoiler alert. The Onley way to get rid of your student loans are to pay them off. You cannot discharge them in bankruptcy. They will follow you until you die because there are two types of debt secured debt. An unsecured debt, types of debt, the secured debt Rx secured by collateral, something that the bank has to repossess. Think about a car. Unsecured debt is like a credit card. They cannot. I mean, they could, but they're not going to come get your yeti cup or your microphone or your iPhone. They can do that, but they're not going to, cause it's just too too costly to them. So credit cards are no collateral. Nothing for the bank to claim. So secure debt is collateral, like a house or a car. Unsecured debt is no collateral. But what about student loans? Are they secured or unsecured? Technically, they're on secure because of bank cannot repossess your diploma. However, reality you the person, are the collateral. And based off of bankruptcy acts of 2005 federal and private student loans are unforgettable. You cannot get rid of this debt and bankrupt Lissy like almost all other types of debt. To get rid of this debt, you have to pay it off. Student loans will fall you for your entire life. They will even garnish your wages. Wage garnishment means that they will take your money out of your paycheck before you actually get your paycheck. So this is separate class. The student loan Deep dive, What will cover in the separate classes and types of student loans. Private and federal types of repayment. Standard graduated extended income based repayment. One really important type of thing to get take away from the types of repayment. Is that there? Some repayment types where you're not even paying down principle. You're only paying off your interest or your balance is actually getting bigger. Even though you're making a payment. It's crazy, so not making payments. You can defer payments. And then there's four Barents, which you can see here which interested cruise, and you must pay it or add it. It is attitude of principle balance. Okay, so for Barents is not good. Deferment is generally not good, either. You just want to pay him off as quickly as possible and forgiveness. Any forgiveness of loans will be taxable, and you will owe the IRS money if you are any of debt forgiven.

40. 33 Financial Freedom: so financial freedom. Take control of your finances and you'll take control of your life. This is one huge thing that people think it is out of control and you can take control of it. OK, so now let's go into it. What does financial freedom mean to use? Use your hand out on skill share. You should have downloaded it right down. Your answer. What does financial freedom mean to you? Okay. Doesn't mean you can take whatever job you want. You can work where? If you want to, you can live outside the United States if you wanted to. What does it mean to you? Okay. What financial freedom means to me is that you can live a life with no financial stress. It doesn't mean that you're not gonna work. It just means that you're not stressed out. You have an emergency fund and you have a screw you fund. If anything were to go wrong, you know, you and your family are gonna be okay for a really long time. Okay? So we want you to own your life, not a bank or some other company toe own your life. And that's what financial freedom means. you have control of your own life to do this, you've got it. Get your finances in order and then you gotta build some passive vs active income. Okay, So passive income is something that you invest a lot of hours on the front end, and it earns money as you sleep. Okay. So ah, lot of my courses are actually like that. I put a ton of time into building out this live recording. The video editing the video is getting the mic all of this stuff, right? But it's passive. Once I'm done with it once I'm, like, created the class and I posted it on skill share. I'm done. Those classes will eventually make money. And that's the difference from active income. Active income is I've actually got a trade. My time for money. Okay, so I'm also a CFO. I have to go into work, or I'm not going to get paid. So I'm trading time for money, and I'm actively involved in that job I love my job is a CFO, but it is different from the passive income that I get from teaching personal finance online. So you want to build up your passive income. So it is there on the side and just makes money while you do nothing. And the last thing is financial freedom can lead to retiring early. You can retire early. Retired doesn't mean you sit on a beach and drink. Mai tais all day, though retired me to do the job you really want to do and live where you really want to live. When I first started working, I thought you had to work at the job until you're 65 then you retire and die. What I learned is this is not true. And as I said at the beginning of the class at age 30 I did a semi retirement. It took a year off. Travel the world. You can do that exit well. You just cannot live an extravagant lifestyle. You'll be able to retire early if you live below your means and follow the core four and everything else that we talked about in this class

41. 34 Irrational Behavior and Treat Yo Self: So what are the challenges to financial freedom? The biggest one is that we're all irrational, and that's OK. As a personal finance expert, I have a rational behavior. The biggest one that I talked about already is that if money hits my checking account, I'm automatically going to spend it no matter what. Okay, So to avoid the biggest pitfall, automate everything. Don't allow your yourself the decision to spend or save save automatically. Then you know whatever's in your checking account is you know, you are able to say to spend that, and that's what I would say. We're all irrational. You've got to recognize that you've got to create guard rails to protect yourself from yourself. And that's what I have done. My money automatically get saved without me doing anything that way. I know I can not overspend because I save X amount per month without ever it every coming into my checking account. So your goal is the pay off all your debt except your house in the next three years. Okay, Pay off all your consumer debt, all the high interest that you want to pay it off in the next three years and then start attacking your house. Big key slide here. This is your goal. Moving on to the next slide. Incentives matter. You gotta treat yourself OK. Don't go overboard, but treat yourself. You know, it does matter that this is a fun, long term journey. This is not like live as frugally is possible in hate your life type of thing. So treat yourself. When should you do that? If you have a one month emergency fund, complete that $1000. Treat yourself paid on all your credit card debt. Treat yourself paid off. Lawyer Carloads Treat yourself Paid off your student loans. Treat yourself invested $10 a month for a year. Treat yourself. You should define your next momentous goals. Follow us on Instagram for more motivational videos at Breaking Dot money.