Accounting Terms You Must Know

Accounting Term Definition, Example and Importance:

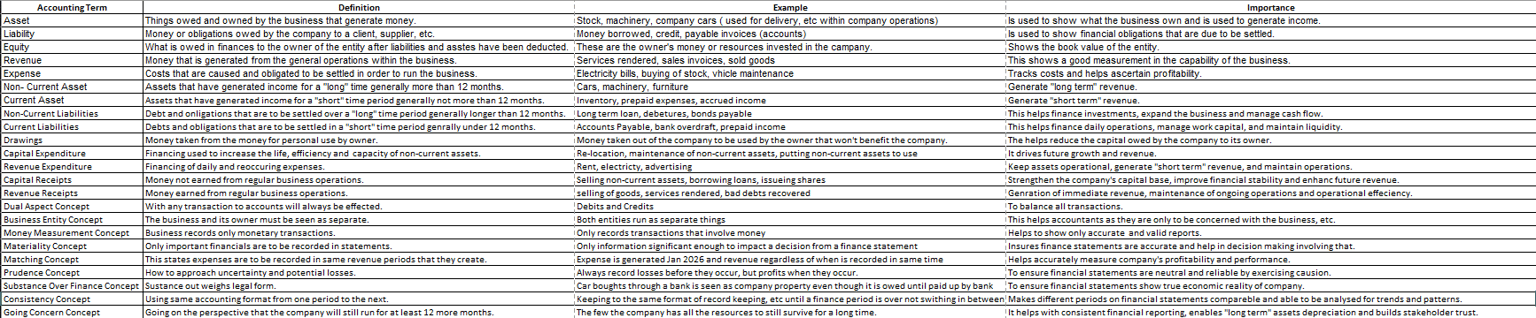

Asset - Things owed and owned by the business that generate money. Stock, machinery, company cars ( used for delivery, etc within company operations). Is used to show what the business own and is used to generate income.

Liability - Money or obligations owed by the company to a client, supplier, etc. Money borrowed, credit, payable invoices (accounts). Is used to show financial obligations that are due to be settled.

Equity - What is owed in finances to the owner of the entity after liabilities and asstes have been deducted. These are the owner's money or resources invested in the campany. Shows the book value of the entity.

Revenue - Money that is generated from the general operations within the business. Services rendered, sales invoices, sold goods. This shows a good measurement in the capability of the business.

Expense - Costs that are caused and obligated to be settled in order to run the business. Electricity bills, buying of stock, vhicle maintenance. Tracks costs and helps ascertain profitability.

Non- Current Asset - Assets that have generated income for a "long" time generally more than 12 months. Cars, machinery, furniture. Generate "long term" revenue.

Current Asset - Assets that have generated income for a "short" time period generally not more than 12 months. Inventory, prepaid expenses, accrued income. Generate "short term" revenue.

Non-Current - Liabilities Debt and onligations that are to be settled over a "long" time period generally longer than 12 months. Long term loan, debetures, bonds payable. This helps finance investments, expand the business and manage cash flow.

Current Liabilities - Debts and obligations that are to be settled in a "short" time period genrally under 12 months. Accounts Payable, bank overdraft, prepaid income. This helps finance daily operations, manage work capital, and maintain liquidity.

Drawings - Money taken from the money for personal use by owner. Money taken out of the company to be used by the owner that won't benefit the company. The helps reduce the capital owed by the company to its owner.

Capital Expenditure - Financing used to increase the life, efficiency and capacity of non-current assets. Re-location, maintenance of non-current assets, putting non-current assets to use. It drives future growth and revenue.

Revenue Expenditure - Financing of daily and reoccuring expenses. Rent, electricty, advertising Keep assets operational, generate "short term" revenue, and maintain operations.

Capital - Receipts Money not earned from regular business operations. Selling non-current assets, borrowing loans, issueing shares. Strengthen the company's capital base, improve financial stability and enhanc future revenue.

Revenue Receipts - Money earned from regular business operations. Selling of goods, services rendered, bad debts recovered. Genration of immediate revenue, maintenance of ongoing operations and operational effeciency.

Dual Aspect Concept - With any transaction to accounts will always be effected. Debits and Credits. To balance all transactions.

Business Entity Concept - The business and its owner must be seen as separate. Both entities run as separate things. This helps accountants as they are only to be concerned with the business, etc.

Money Measurement Concept - Business records only monetary transactions. Only records transactions that involve money. Helps to show only accurate and valid reports.

Materiality Concept - Only important financials are to be recorded in statements. Only information significant enough to impact a decision from a finance statement. Ensures finance statements are accurate and help in decision making involving that.

Matching Concept - This states expenses are to be recorded in same revenue periods that they create. Expense is generated Jan 2026 and revenue regardless of when is recorded in same time. Helps accurately measure company's profitability and performance.

Prudence Concept - How to approach uncertainty and potential losses. Always record losses before they occur, but profits when they occur. To ensure financial statements are neutral and reliable by exercising causion.

Substance Over Finance Concept - Sustance out weighs legal form. Car boughts through a bank is seen as company property even though it is owed until paid up by bank. To ensure financial statements show true economic reality of company.

Consistency Concept - Using same accounting format from one period to the next. Keeping to the same format of record keeping, etc until a finance period is over not swithing in between. Makes different periods on financial statements compareble and able to be analysed for trends and patterns.

Going Concern Concept - Going on the perspective that the company will still run for at least 12 more months. The few the company has all the resources to still survive for a long time. It helps with consistent financial reporting, enables "long term" assets depreciation and builds stakeholder trust.

by Eevee_247