Transcripts

1. Class Preview: This class is the first in a series of classes that dives into the world of investing for the millennial generation. Those born after 1980. Although all ages and generations been greatly benefit from this class, you under invested scared to invest. Not sure exactly what to invest in will review the risk reward ratio. The best thing. The power of compound interest, proper diversification, historical stock market returns and how investing is critical and keeping up with inflation will do case studies that help us figure out you're right mix of stocks, bonds and alternative investments in your portfolio. So joining me for a Siri's that gives you the confidence to start investing and take charge of their financial future.

2. The Power of Compound Interest: Did you know that the millennial generation those born after 1980 are the most under invested generation? Is that even a bad day? They are protected stock market downturns, right? The power of compound interest gives us a good reason to think about deploying more of our cash into stocks and other investments. Compound interest works like this. Let's say Mary has $10,000 saved up in cash and 30 years Mary will end up with $10,000. Still invest in cash. But since there's inflation, which factors in for the increased of the cost of goods and services in the future and 30 years, Mary will actually end up losing money. $10,000 is only worth a few $1000 in cash 30 years in the future because of the cost of living increases, even if for savings rate stays the same value to the buying power of $1 decreases throughout time. Having some of our money invested is not only good for growth, but it's also good for keeping up with inflation. As time goes on, our money becomes less and less valuable. That's why I could buy a brand new car in 1964 for only 3000 bucks in cash. Forget about that. Today. The average new car would cost $25,000. Bob is smart, though. He invests his money at the age of 30 with $10,000 puts it in a nice balance mutual fund. His average returned over the next 30 years of 7% which is close to the stock markets. Historical return. Bob does not contribute any more money to the stock market, and he'll still end up with $76,123. Not bad Bob, but he could do a lot better. All right, so now let's say Melissa, invest $10,000 at the age of 30. But she also contributes $500 every month into our investment account and keeps it invested . $500 per month ends up being about 6000 per year in savings, and she does this for the next 30 years. Melissa will end up with a whopping six, $182,560 when she's the age of 60. That all sounds great, but inflation will end up making her amazing $682,560 seem a lot less because buying a new car may cost $150,000. The average inflation rate historically has hovered around 3%. So if your investment returns average 7% a year, that you would subtract the rate of inflation by your investment returns to get your real rate of return, which in this case will only be 4% which is great. But it makes the point of how investing and investing well is your best way to not only beat inflation to make best use of your cash and maximize the sides of your network 5 10 20 years down the road. So now that you understand why investing is so critical to building your net worth vs holding just cash, let's go over some investing basics.

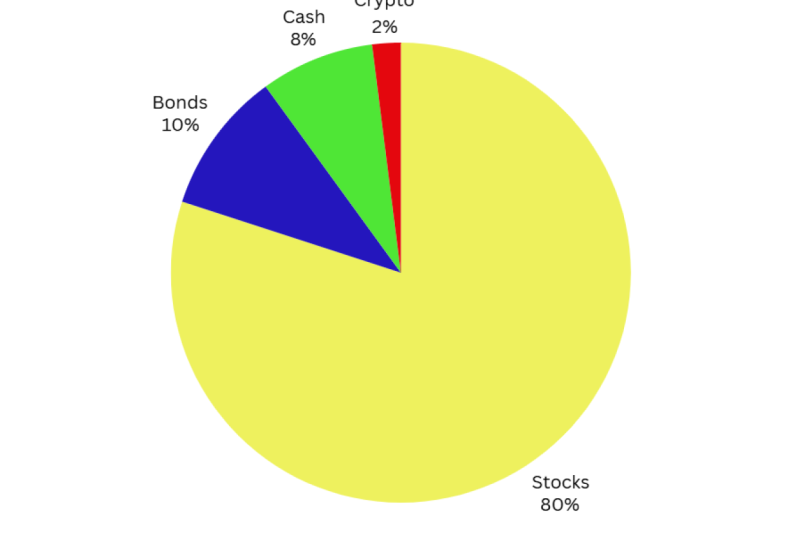

3. Risk/Reward and Different Investment Types: before we dive into your investment options, we need to go over the idea of risk and reward. The greater the rescue taken investing, the greater return you should expect to receive. Also, the greater risk you take the greater chance for losses. The biggest challenge that hedge fund managers and institutional investors battle is balancing this risk. Reward factor. Too much risk leaves you open to big losses in stock market downturns. Too little risk gives you a return barely over our even under the rate of inflation. So you might as well just have your money in cash, which is not a good option either. So finding that right balance between risk and reward can be as easy as diversifying your investments. Diversifying your investments This a simple act of spread your money across multiple investment types to balance your risk. More diverse you are the better chance you have of surviving its stock market crash simply because you have a mixture of home equity gold bonds to help offset moderate the losses experienced during the stock market correction. Also, this is the reason you don't have most of your bunion a wealth tied up in your house as a housing crash. Wipe out on the stall your savings, having your money and different pots with different rates of returns hopes to moderate that risk. You have a little cash and you're ready to start investing. There are several options available to you, even if you don't have a lot of cash stashed. Stocks the most well known investment vehicle and for good reason. These could be some of the most volatile options for your cash but can offer a stolid return. Historic stock market returns have an excellent. The average return on the S and P 500 has been a little over 11% from 1973 to 2016. Not a bad return. That's an excellent return. But if you look at the 2008 horrible, terrifying, gut busting negative 37% return, you'll see why you dont invest 100% of your money in the stock market. But don't let that horrible return fool you, though. If you don't panic and you did not sell any of your money in 2008 you would have doubled your money invested before the 2008 dip. That means after the horrible, worst case scenario. Return of the negatives 37% and the long run. He still would have come out making money. The majority of millennials like myself group at a time when nothing could be trusted and the best place to put your money was under the mattress. That's caused us to be a little more frightened of the stock market than our parents, who experienced what seemed to be a constant stock market boom. But throughout time, they have been years of horrible returns. Take, for instance, 2002 after the dot com bust or tech stocks blew up and crashed down to reality. The return for 2002 was a negative 22.1%. Yikes, that's pretty bad. But what about 2013? A stellar positive? 32.4% or 2000 threes? Positive 28.7% return. There will be ups and downs in the market, but staying invested and not panicking can give you a better chance of increasing your returns. Fidelity Investments did a study a few years ago to find out which age group and generation had the highest return. Do you know who had the highest return on their investments. Baby boomers, maybe hedge fund managers? Nope. Dead people. Yes, the ones who forgot they had a 401 K or investments, which later were found by relatives. And they had the highest return, why they did not try to time the market. This also proves that panic selling and being afraid of the stock market because of those few very bad years of returns is not warranted. It can actually decrease your potential for growth of your net worth. As I mentioned earlier, investing 100% of your money and stocks is not a great idea. There's something called index investing, though. This is where you put a chunk of your money in index E T F or exchange traded fund, and these funds tracked very closely the S and P 500 index, the Dow or a wide range of other indices. Well, that's a great idea for a portion of your cash. The better thing to do is diversify some of that cash into bonds. Bonds usually moved counter to stocks, so when stocks are doing well, bonds usually do not do well. While when bonds are doing well. Stocks usually are struggling. This is why having a mixture of both stocks and bonds will help the balance that risk reward meter. The younger you are, the more risk you could take on the older you are, the less risk you should take, since you'll be wanting to spend some of your investments and retirement very soon. That is why the mix of stocks and bonds in your portfolio should be determined by your age rather than other factors. If you go to vanguard dot com and look at their target retirement funds, you'll notice the ratio of stocks and bonds changes as you get closer to retirement. If you're a millennial, for example, let's say, 28 years old, you may wanna have 80% stocks in 20% bond. Mix it for 34. Like myself, I may want to increase that slightly to 25% bonds and 75% stocks. Someone closer to 60 may wanna be 60% bonds and only 40% stocks during stock market corrections bonds tend to actually increase in value. So once again, this is why diversification help you feel better about your investments as a whole. When a wide variety of issues come up in the world and markets is your home a type of investment will find out next.

4. Housing and Alternative Investments: believe it or not, your house counts of your investment mix. You have some stocks, maybe a bond fund, but your house is now 1/3 way you can invest, but you don't have to own a single family home to benefit from the housing market. There are now ways to invest using E T EFs or exchange traded funds that help you get a piece of real estate without ever having to have a home loan. The most well known way to do this is buying a REIT or real estate investment trust. You invest in a basket of real estate businesses who owned properties who then tell you it dividend or return from those properties. But you don't actually have to own the properties. You just own the stock of the company that owns the properties. That means new landlord ING are worrying about needing a new roof. This is an easy, low cost way to invest in housing. Bangar just happens to have a low cost re TTF called V in. Q. You can look up those symbols on their website to find more details. Obviously, owning a home is a great investment, but not because the returns are very great. They actually have less than a 2% historical return, which is less than 3% inflation rate. So it sounds bad. I lose 1% a year after inflation. What could be good about housing? It's It's a great forced savings vehicle, meaning of pay or mortgage every month. But some of that mortgage payment goes toward the principle of your home, so each month you reduce how much you owe on the loan. So if that keeps happening, if you sell your house 20 year from now, you will have some nice home equity. Also, you get to enjoy living in the home. And if home prices have a higher than average return while you're owning the home assistant added Bonus is investing in a home a surefire way to get a solid return. Not always the case. People are just now recovering their losses from the 2008 housing bust, But the good news is they have recovered, and now they could finally start to add equity into their homes. And during those 10 years they have been making principal payments. Thus, they came out on top with some nice equity, even though the value of their home stayed the same. This is everything that does not fall on your stocks, bonds or housing. This could be commodities like oil or gold. You could buy these E. T. ETFs or exchange traded funds that trade just like stocks. But I don't always suggest these types of alternative investments until you feel very comfortable with investing and could put a lot of time researching the oil market. For example, crypto currencies is a hot topic in the investing world, even though I do recommend that can have maybe 5% of your total investment portfolio invested in alternative or risk your investments. I just cannot recommend Krista currencies at this time too volatile for my taste, although you can always try and test the waters. But I like to stay safe and dry too many solid companies to invest in. Instead, there is an alternative investment option called Peer to peer lending. Lendingclub dot com is an example of one of the more popular peer to peer lending sites. This is where you can invest $5000 for example, and break it up into small chunks toe loan out to a wide array of people needing to borrow money for car loans, home loans or personal loans. You can increase your return by investing in riskier borrowers are those with a lower credit score off course. You increase your chances of them defaulting on the loan and losing your money with little chance of getting it back. You could play it safe and only invest in those with excellent credit scores and get a okay return. But it's not. Without its risks and the economic downturn, investing in peer to peer lending will have more risk. As people lose their jobs, they lose the ability to pay back these little loans. So how do we find the right investment mix? We'll go over that next.

5. Case Studies and Finding The Right Mix: Let's build a few investing mixes for some different investor types so we can get a good grasp on what is a good risk. Reward balance and investing Knicks. Nikki is a 31 year old teacher married to a 34 year old police officer. They have $4000. They won't invest right now, but they also want to start saving $4000 each year. What types of investment should they make? So let's look at their age. They're relatively young, so I'd recommend a mix of investments that tends to be higher on the risk reward scale. So perhaps the lion share of their mix would perhaps be in stocks. Let's say 70% with the second highest category would be bonds at 20%. I would take 5% of their portfolio. And put that in a mix of alternative investments, like reads peer to peer lending. Maybe pick a few individual stocks and solid blue chip companies with great dividends. This mix provides enough risk to increase the return while they're younger. So as they age, their high return when they're younger would compound to create a bigger nest day when they retire in 30 years in 30 years. Based on the 7% average return, they'll come away with about $434,741. But we need to factor in inflation. So let's take away 3% from their average 7% return. Their money in 30 years will be like having $246,286 in today's dollars. So not as much as you'd hoped for after 30 years of savings. Let's also say they save 10,000 additional dollars for down payment on a home. Or they took some of what they were gonna put in their bond fund and and use that as a down payment on a home. 30 years. That loan will be paid off in full, will also be able to retire without a mortgage or downsize and cash out the value of the home and add that chunk to their investment stash, giving them a better chance at a reasonable retirement. We have Mark a single man who's 25 years old. He has zero to invest now, but he wants to start investing $300 a month into a brokerage account. By 62 years of age. He will have $617,619 saved. That's factoring in an average 7% return. After you account for ablation, he'll have $300,463 in today's dollars. Since markets still really young, he could afford to take on more risk. So let's put him in 90% stocks in the Lincoln percent bonds. He might be able to increase his return to 8% over the long run, giving him a $789,537 return at 62 years of age, or $375,606 return after adjusting for inflation. Let's say he decides to buy a home at age 30 and keeps it, and he owns until he's 62. With a 30 year mortgage, he'll have his home paid off and will be able to add his own equity to his investments and his networks. Let's motivate mark a little bit, and he decides to increase his monthly savings rate from $300 to $900 adding only 600 additional dollars of savings each month. By the time markets 62 years old, we'll have a whopping 2,368,007 $12. Holy moly. What a difference it makes tweaking your monthly savings rate. Of course, investing wisely as well. Are you starting to see the power of compound interest? So now that I know the right mix for my investments, how do I get started? What E. T F stocks bonds door by. This is work. It's a little complicated. There are no perfect right answers to this, and it varies wildly depending on your own unique situation. New lessons will be added to this class very soon. That will dive into more details about exactly which stocks in TFC mutual funds or bonds fund should have picked for my investing mix.

Lindsay Marsh, Over 600,000 Design Students & Counting!

Lindsay Marsh, Over 600,000 Design Students & Counting!