Transcripts

1. Introduction - What does this course cover?: Welcome to accounting and bookkeeping basics in 90 minutes. My name is Shweta and I'm so excited to be your instructor for this course. I am a qualified chartered accountant and I have over 10 years of experience working in some of the top global accounting firms have helped a whole range of businesses. I understand how a difficult accounting and bookkeeping can be. So whether you are a business owner, looking to understand the basics of accounting or a student looking to kick start your career in accounting. This course should provide you with a great foundation in both accounting and bookkeeping. So what will this cause cover? Well, in this course, I'm going to assume that you have no prior knowledge and accounting. I've split the entire course into three different modules. In the first module we look at the why. So why is accounting and bookkeeping so important? Why do we need key financial reports? We then start a business together where I introduce you to our course example that we'll be using throughout the rest of the course. In the second module, we look at the what, so what are the components of a profit and loss and a balance sheet, and what information to each of these reports provide. I'll then introduce you to the accounting equation, also known as the backbone of accounting. Now I know it sounds like maths and it sounds complex, but I've tried to simplify this as much as possible using real life examples. Then we look at double-entry system and how there's two sides to every story. In the third and the most challenging module, we look at the how. So how do we use all the information that we've learned so far to produce what we call T-accounts. And how did debits and credits work? If you have any background in accounting, you might know that debits and credits are some of the most confusing topics for anyone who's new to accounting. So I've got a few special tricks here for you to help you master this topic as soon as possible. Then we have some practice exercises in an Excel format that you can download and practice to see if you've understood the concepts well. We've also included some videos where we go through the solutions together. Okay, but what makes this course so different? Why should you do this coast? Well, first of all, it's a 90 minute cause and we get straight to the point. I don't know about you, but I like to learn things that quick and easy way if possible. This course does just that. We've kept it focused on the core fundamentals of accounting. You can be confident that you're learning the concepts from an experienced and qualified accountant. Accounting can be boring and drive at a lot of concepts, but we've tried to keep this course fun and engaging by using a whole range of real life examples. I've also included some practice exercises that you can use to test your knowledge. And lastly, there's tips and tricks throughout the course to help you get started with accounting and no time. So now that you know what to expect, Let's jump right in and let's get started.

2. Why Is Accounting So Important?: Hello and welcome to the first module of this course. In this module, I'll be introducing you to Accounting by looking at the WHY. So why is accounting and bookkeeping important? Why do we need it? Why should we look at key financial reports like a profit and loss and a balance sheet? I'll be demonstrating all of this by taking you through a story, a story where you and I get into business together. But before we dive into our story, let's first have a look to see why accounting and bookkeeping is so important. So accounting is a method of systematically recording, analyzing, and reporting key financial information. This is then crucial for decision-making purposes. So when you have a good set of financial information, you are more likely to make better informed business decisions. On the other hand, if you have bad financial information or no financial information at all, then it's unlikely that you can make good and wise decisions. It's also known as the language of business. And this is because it's used to communicate financial information to all the interested parties. Now this could be internal parties like yourself as business owners, or external parties like banks. So for example, if you get a loan from a bank, they would usually request for a set of financial statements so they can assess the viability of your business before they lend you money. It also helps avoid cashflow issues. So by using historical financial performance, you can forecast and budget future business performance and identify areas or periods of time where there's likely to be cashflow issues. By knowing it in advance, you can take the necessary steps to avoid that from happening. And lastly, it's also useful for income tax compliance. So now that we know the facts, let's actually dive into a story and have a look to see how that works.

3. Let's Start a Business! - Introduction to the Course Example: So like I mentioned earlier, you and I have decided to join forces and get started on a business together. We've decided to go with the company structure because that would just soon as best in this case. And we've named our business Paw Leads. Like the name suggests, it's a business where we sell high-quality premium leads for dogs. We currently only have one product, which is the red lead that you see in this picture here. Now because this is a brand new business, we, as business owners have had to put some cash in to get started. We use some of this cash to go to our supplies and get some stock. We've also set up a very nice looking online store, so we're good to go. The first day has gone past and we have successfully made a few sales. We then repeat this process day in, day out. And a few weeks later we realized that our sales have grown significantly. So as business owners, we need to be able to ask and answer some of these key accounting questions. Like, what's our profit? Should we be changing our selling price to increase our sales? Should we sell more products and expand our business? And if so, which product will be more profitable? Should we be renting a shop as part of our expansion? And will there be enough cash to support all our growth plans? So these are just examples of some of the questions that business owners would ask and would need some solution to be able to answer these. So that's where key financial statements come into play. Generally speaking, there are three key financial statements. The first one is the profit and loss, also known as the income statement. This shows the performance or the profitability of a business over a period of time. Next is the balance sheet, and this shows the financial position of the business at a certain point in time. In other words, it shows everyone what the business owns and owes to others. And lastly is the cashflow statement. This shows the change in cash over a period of time. So these are the three key financial statements. So now that we know what the key financial statements are, how do we get them? So back in the day, board business owners and accountants use to manually maintain these books called ledgers. But these days we have one line accounting softwares that help make the bookkeeping and accounting process a whole lot simpler. These are just examples of some of those softwares available. Now, regardless of whether you're a business owner or an accountant or a bookkeeper, you will almost certainly need to use one or more of these softwares. So then you might ask, well, why do we need to learn the basics of foundations of accounting when these softwares can just do it for us? Well, yes, the softwares do make it easier. However, they are just a tool for the user. So in a nutshell, in order to be a savvy business owner or an accountant, you need to be able to understand the foundations of accounting. So you can better do the bookkeeping process and analyze the financial information produced by these reports. Not only that, when you're considering a future business opportunity, you can understand the impact of those transactions on your accounts before you make those decisions. So that brings us to the end of this module. I'll see you in the next module where we'll look at these reports in a bit more detail. See you there. Congratulations on completing this module. Please don't forget to leave a rating on a review to share your feedback. It would really mean a lot to me. I'll see you in the next module.

4. Profit & Loss Statement - How much has my business made?: Welcome to the next module of this course. In this module we'll be looking at the what, so what are the components of a profit and loss and a balance sheet? And what is an accounting equation, also known as the backbone of accounting. So the profit and loss is one of the main reports that business owners are most interested in because it tells you whether or not you've made some money from your business. Hence, it's also known as the income statement, and it shows the performance of the business over a period of time. I say over a period of time, because you can view a profit and loss over different timeframes. So it could be for a few weeks, a month, a few months, or even an entire financial year. And it shows you your net profit or loss for that period. So let's consider an example. So let's say we've made sales, also known as revenue or income, of four piles of cash, as shown in the picture here. Out of these four piles of cash. let's say we've had to spend two piles to buy some stock, also known as the inventory. Now because this relates directly to the sales that we've made, this sits under the cost of goods sold. So in this case, cost of goods sold is two piles of cash which we need to take off from our sales. Then normally you would take off any other expenses that you've incurred in your business. But for simplicity, let's say in this case our only cost is the stock that we just took off a sales. So whatever is remaining is our net profit. In another example, let's say we are still made four piles of sales. However, our cost of goods sold is five piles of cash. So not only do we need to take away the four piles of cash that we have here But we've also had to fork out another pile from our own pocket. In other words, we're out of pocket by one pile and have made a net loss of one pile. So now that we understand the concept, let's actually put some numbers in and have a look at a few examples. So in our first practical example, let's say move soil to a 100 leads at $20 each. So in this case our revenue for the period would be $4,000. Next, let's say we've had to buy those leads from our suppliers at $10 each. So our cost of goods sold would be 2000 dollars. In this scenario, our sales is higher than our cost of goods sold, which means we've made a profit of the difference, which is $2000. In the next example, both still made the same amount of sales. However, instead of paying $10 by lead to our suppliers, we've had to pay $25 each. So our cost of goods sold in this example would be 5000 dollars. So as you can see here, it's the flip side. So our cost of goods sold is higher than our sales, which means we've had to pay more to our, suppliers to get the stock, than what we sold it for. As a result, we made a loss in this example of the difference which is $1000. So these are just a couple of examples of very simple and straightforward profit and loss. Next, I'd like to go through a more detailed profit and loss because that's what you'd most likely see for your business. So in here, I've got a screenshot from an accounting software of a sample profit and loss or an income statement for a period of three months. As you can see, there's a lot more detail in here. So let's have a look at each of those components. At the very top, I've got my income. So in business, you might have more than one product that you sell and you might want to separate them out so you can see the profit or the sales of each of those items. So in our example, in addition to lead, we are also selling pet costumes. So I've got my income separated by each of those. I've also got some discounts that I gave to my customers up here, which is what we see at the very top. This is included in income because it reduces the income from our sales. When we add up the top three items, we get a total income of about 8,400. Then we have our cost of goods sold. So in the previous examples so far, we've only considered our cost of goods sold to be the stock that we buy from our suppliers. In reality, however, depending on which industry and what your business model is, you might have other things that form part of the cost of goods sold category. So for example, if you're in the manufacturing sector, you might have the cost of direct labor. So in other words, where staff, put their time in to manufacture the product. Now because this is also directly related to the product that you're going to sell. It forms part of the cost of goods sold category. Another example could be the cost of freight or shipping to get the items shipped from your supplier to your own warehouse. Again, because that's directly related to the sales, you could include that in your cost of goods sold category. You can choose to still break it down. So for example, under cost of goods sold, rather than lumping it all into one bucket here, we could have separated them out into a stock, freight costs and also manufacturing on labor costs. When you sum up all of those, you would get your total cost of goods sold. So once you've got your total income and your total cost of goods sold, like we saw in our previous examples, we find out what the differences which will give us our profit. It's called the gross profit and essentially means your true profit just purely by picking up the costs that relate directly to the sales of the products. Then we have a whole list of expenses. So you can see we have things like insurance, advertising, legal fees, rent, electricity charges, etc. And basically these are all expenses that relate to the business overall. So it's not directly connected to the sale, but they are all necessary costs that need to be incurred in order for you to be able to operate your business. So because these are all general expenses, they said below the gross profit under the expenses category. So we've got all of our different expenses listed out, which in this scenario gives us our total expenses of $7,248. Next, we take off all of these expenses from our gross profit figure, which will then give us our net income or a net profit. This is the ultimate profit after all the costs have been taken off from our sales. So this is an example of a more detailed profit and loss statement. Next, let's have a look at cash versus accrual, which is a concept that you should really know as well.

5. Cash & Accrual Accounting: In this lecture, we'll be looking at one of the other most confusing topics in accounting, which is the two accounting methods. In the accounting world, you'll often hear the terms cash was as accrual accounting. And these are basically just two accounting options that are available for business owners to choose from. The main difference between the two, the timing as to when income and expenses are recognized in the profit and loss. These differences are just temporary differences. So if you add a look at the profit and loss between the two methods at certain points in time, they might produce different results. However, in the end, the overall results between the two methods will still be the same. At the end of this lecture, you will also have a better understanding as to why profit does not always equal cash. So like I said earlier, the main difference between the two methods is the timing of recognition. So in the cash method, sales are recognized when cash is physically received, and similarly, expenses are recognized when cash is physically paid. So if we pick up our example from the previous lecture, where we sold $4000 in leads, let's say we send the invoice to the customer on the first of the month and we gave them 30 days to make payment. So in other words, they only need to pay us those $4,000 by the 30th of that month. In the cash method, we will only recognize the revenue on the 30th when the customer has paid us the money. The same goes for supplier payments. Now let's have a look at the accrual accounting method. So in the accrual method, revenue is recognized when it's earned. What does that really mean? So when I say earned, I mean when the goods are provided or the service has been provided to the customer and there is an expectation to get paid. So looking back at our example, this would mean we'd recognize revenue on the first of the month when we sent that invoice to the customer, even though we haven't actually received payment for it. Because on the first, we have provided the goods to the customer and we expect to get paid for it. Similarly, expenses are recognized when they are incurred and we use what is called a matching principle. In other words, we recognize the same amount of expense as we recognize income so they match. Now let's have a look at an example to see how this works practically and impacts the profit and loss differently. So following on from the example that I introduced, let's have a look at the net profit on the first of the month. Now remember, first is when we issued the invoice to our customers and we've also received the invoice from our supplier for those stock. So for sales, we've sold 200 leads, a $20 each. However, 100 leads were sold in cash, so customers have already paid us for it. And 100 leads were sold on credit. So customers have 30 days to make payment. Similarly for our cost of goods sold, we bought 200 leads at $10 each, but we've only paid cash for a 100 leads to our supplier of the other 100 leads are on credit, so we have 30 days to make payment. So under the accrual method, the sales would be the entire amount. So 200 leads times $20 each being $4,000 This is because on the first we earn the revenue on the entire 200 leads. We have sent the invoice to the customer, we have provided them with the goods and we have an expectation to get paid. So we'd recognize the sales on the full amount. Similarly, the cost of goods sold would be using the matching principle and recognize the cost on the entire 200 leads. So thats 200 leads times $10, which will give us $2,000. The net profit therefore is $2,000. Now let's have a look at the cash method. So in the cash method, if you remember, income and expenses are recognized when cash is transferred. So for sales, we've only received cash for 100 leads. So our sales would be 100 leads times $20 each, which will be 2000 dollars. Our cost of goods sold will use exactly the same principle. So 100 leads times $10 each, which will be $1.000. Our net profit is $1,000. So as you can see, there's a difference in the net profit between the two methods. And in terms of the physical cash that we have left in the bank account, this would be a more accurate description of that. So we actually only have one thousand dollars left in the bank account. Yet the accrual method shows a net profit of $2,000. So this is where profit does not always equal cash, especially if you're using the accrual method. Now let's jump forward to the 30th of the month where the rest of our customers have paid us cash. And we've also cleared at debt with the supplier. So the sales and the cost of goods sold are still the same. However, the 100 leads that were on credit have now been paid by our customers. And we have also paid our supplier for the 100 leads that we owed them. So under the accrual method, there's going to be no sale is no cost of goods sold and net profit on the 30th, because we recognized the entire amount on the first. Under the Cash method, we recognize the cash that was received and spent. So for sales, we received a 100 leads times $20 each being $2000 and for cost of goods sold, we received 100 leads times $10 each, which is $1,000, being a net profit of 1,000. Again, you see a difference between the cash and the accrual method where the accrual method shows 0 profit and the cash method shows a $1000 profit. Now if you remember when I introduced this concept to you, I mentioned that these timing differences are only temporary and at the end, they still work out to be the same. So let's have a look at the net profit from the first to the 30th. So the entire month. Under the accrual method, like we saw two slides before, the sales were 4000, cost of goods sold was 2000, and our net profit was 2,000, all of which which was recognized on the first, which is when we issued the invoice. Under the Cash method, we had some income and expense on the first and some on the 30th. So now we combine the two I sales where $4,000, which is made above 2000 on the first and 2000 on the 30th. Our cost of goods sold is also $2,000, which was 1000 on the first & 1000 on the 30th. This gives us a net profit of $2,000 for the entire month. So as you can see now that we've reached the end of the month, the cash and the accrual method show the same net profit figure. So now let's have a look at the advantages and disadvantages of using each of these methods. So under the cash method, the positives are that it's very simple and easy to maintain. So if you are a very small business and you don't provide credit terms to your customers, meaning all your customers pay back cash and you pay your suppliers in cash right away as well, then you could probably get away with using the cash method. It also shows you the true cash position at any point in time, which is pretty much your net profit. You pay tax only when you receive the money because you only recognize income and expenses when the cash is transferred. The negatives however, is that under the cash method it shows incomplete information. So if you remember on the first, the accrual method showed a profit of 2000, whereas the cash method only showed a profit of 1000. So it might not show the true financial performance. Also, you're unable to track any receivables and payables under the cash method. The accrual method, on the other hand, provides more complete information. And it is a bit more complex to maintain compared to the cash method because you have to keep track of those receivables and payables amounts. Also, you can't track cashflow purely by using the accrual method because like you saw, the net profit did not always equal the cash amount, in the accrual method. So that's why you need to use other reports like cashflow statements in order to understand your true cash position if you are using the accrual method. So that's a quick summary of the cash and accrual method and accounting. I will hope to see you in the next lecture.

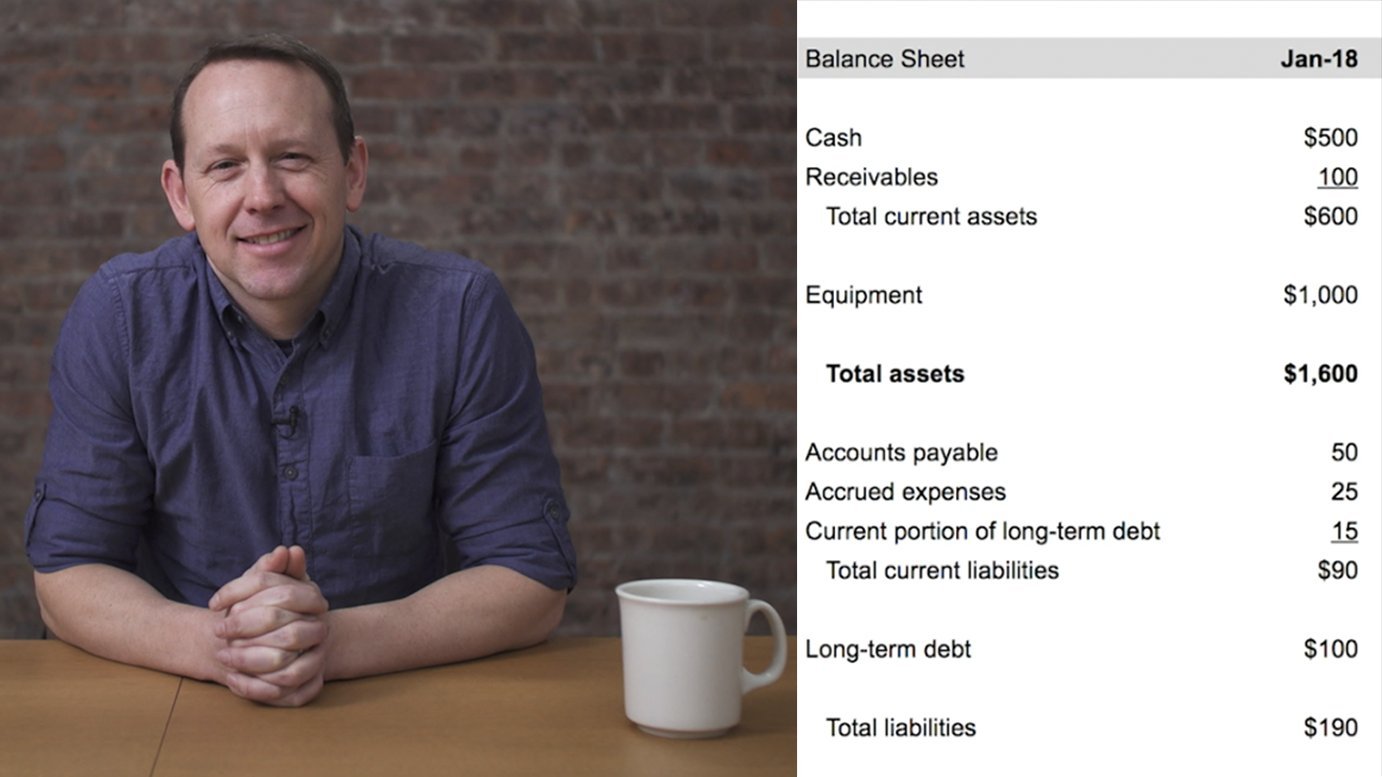

6. Balance Sheet & The Accounting Equation "Own = Owe": In this lecture, we'll be looking at the second most important financial statement, which is the balance sheet. A balance sheet is also known as the statement of financial position. And that's because it shows a snapshot of the financial position of a business. You always view a balance sheet at a certain point in time. So this could be at a specific date at the end of a month, quarter, or even a financial year. It's different to a profit and loss which you run over a period of time. So a balance sheet usually shows you anything that the business owns. In the accounting world, this is called assets. And it also shows you anything that the business owes. So it could all money to others, which is called liabilities. Or it could own money to the owners of the business, which is called equity. So you now know that there are three components and a balance sheet, which is assets, liabilities, and equity. Let's have a look at each of these components to understand them a bit better. So assets, like a said, is anything that the company owns. Examples of acids include cash in the bank, inventory or stock that's been purchased, accounts receivable for money owed to us from our customers, any property that's been purchased. So for example, let's say we bought a store for our business. Paul leads, that would be an asset of the business. Similarly, any plant and equipment that's been purchased would form part of the assets as well. So these are just examples of some of the assets. We could then group these assets into two categories, current and non-current assets. Current assets are any assets that we expect to use within one year's time. Examples include cash, inventory, and accounts receivable. Non-current assets, on the other hand, assets that we expect to last for more than one yo examples of this include property, plant, and equipment, because these are things we purchased ones and expect to use them always several years. So that is assets. Now let's look at liabilities. So liabilities are everything that the company owes to others. Examples include bank loans, accounts payable. So any money that we owe to our suppliers, salaries payable to our employees, and even taxes that we owe to the IRS, like we did with assets where we group them into current and non-current, we could do the exact same for liabilities as well. So under current liabilities, we expect any liabilities that are due within one year is time, such as accounts payable, salaries and taxes payable. Under non-current liabilities. We include any liabilities that are due in more than one year's time. A typical example of this would be a bank loan, because we expect to pay that loan over several years. So that is liabilities. Now let's have a look at the final piece of the puzzle, which is equity. So equity, like I mentioned earlier, is any amount that is owed to the owner of the business. It is the owner's bucket. And the reason I say that is because it's the residues amount that's left in the company. If it was to sell all of its assets and pay out all of its liabilities. So if I was to put that into a formula, it would look something like assets minus liabilities equals equity. So as you can see, it's not as straightforward as assets and liabilities, but it's in fact a residue amount that's left over after all of these have been taken into account. So if we look at equity into a bit more detail, weekends fit that into three main components. The first component is called paid-up capital, also known as share capital. This is pretty much the owners initial investment or shares in the business. The second component is called retained earnings, and it's the cumulative profit and loss amount. It pretty much goes up or the balance increases when there has been a prophet and the balance decreases when there's been a loss. This balanced fluctuates month, month on month depending on what's happened in terms of the financials. The last component of equity is called dividends. So dividend is a withdrawal of profit from the business. Now because we are taking a portion of the profit out of the business, it reduces this retained earnings cumulative amount. That brings us to the end of the equity section. So you now know what the three components of a balance sheet up. We know what an acid is, what a liability is, and what equity means. If I was to recap the formula for equity, we know that its assets minus liabilities equals equity. In other words, it's the residual portion in the business that's owed to the owner. We can then take this formula one step further and rearrange it. So if we move liabilities from this side of the equation to the other side of the equation, it would look something like this. Assets equals equity plus liabilities. In a more pictorial form. We can see we've got acetone one side and liabilities and equity on the other side. I would like to focus that both the sides must always equal. And hence it's called the balance sheet because it always balances. On one side we have assets and on the other side we have equity and liabilities. This is also called the accounting equation, and we'll keep referring to it throughout the course, is known as the backbone of accounting because it forms the basis of all accounting concepts. The key message out of this is to remember that both sides always balance and assets equals liabilities and equity. We can also draw a line at the top and in between these accounts, sort of in the shape of a T. This is what accountants referred to as T-accounts and it's a method of visualizing the impact of each transaction. We will cover T accounts in more detail in the next module. But for now, just remember that assets equals liabilities and equity. But then you might wonder, how do we make sure that both the sides always balanced? Well, that's where the concept of double entry system comes into play. We will look at this in more detail in the next lecture. So I'll see you there.

7. Double Entry System - The Two Sides to Every Transaction: Welcome to the final lecture in this module. In this lecture we'll be looking at double entry system, what it means, and work through some practical examples to make more sense of it. So double entry system is the basis of all of accounting. It's the way of making sure that the accounts always stay in balance. And the way this works is that there's always two sides of a real transaction. Based on the notion that there is an economic benefit that flows from a source to a destination. Source being one side and destination being the other side. Both the sides are always equal and opposite. And this is how the accounts always stay in balance. Now this is a lot of theory. What does this actually mean? Let's walk through a few examples and then we'll make a lot more sense. So in our first example, let's say we as owners have lent money or $1500 to our business. Pauline's. What are the two sides of this entry? The source is us, the owners. We have length $1500 to the business. So remember, this is called equity. The other side is the destination, which is the bank account where the money has been deposited. So the other side of this double entry would be cash. Like I said, the two sides are cash or bank account and the owner's equity. Let's now put this in the form of a balance sheet and see how this is represented. So remember from our previous lecture, we've got assets on one side, liabilities and equity on the other side. We've drawn a T through the middle. And now let's put through our double entry. So we've got cash on one side. Cash is an asset and therefore it would sit on the left side of this T. So we've got cash of $1500. The other side of our double entry is equity, because we've lent some money to the business. Equity is on the right side of the team. So our equity, also known as a paid-up capital, goes up by $1500. If we sum both the sides, we will see that the assets add up to 1500 and liabilities also add up to 1500. Both these totals balance and therefore, a balance sheet is in balance. We put through two sides of the transaction, which is the double entry. They are of equal amounts. And the end result is that the accounts balance. Let's have a look at another example. So let's say now we borrowed some money from the bank, which is a $1000. What would the two sides of this entry be? Feel free to pause this video, have a think about it and then play it. So the double entry for this transaction would be the sauce, which is the bank. So we borrowed some money from the bank, which is a loan. And the destination again is the bank account. So two sides are cash or bank account. Loan. Again, let's put this in the form of a balance sheet. So our cash has now gone up by a $1000. Remember, it was 1500 before, and now we're borrowed an additional $1000 from the bank. So a cash has gone up to 2500. The other side of the double entry is the loan. Loan is a liability. So we need to put the loan under the liability of a $1000. Again, we sum both sides up and we noticed that the left side of the T, which is assets, equals the right side of the T, which is liabilities plus equity of 2500. And our accounts, again balance. Let's have a look at the third example. So in this example, let's say we've bought some stock of 2000 dollars. The two sides of this entry would be the source, which is a BankAccount. We've had to pay some money from a bank account. And the destination would be inventory, because we've received some inventory in return for the cash. So the two sides are inventory and cash. I've got accounts payable here. That's if you use the accrual system and you haven't paid the money by cash, it would go to accounts payable instead. So again, let's put this into our balance sheet. So remember we are reducing our cash by $2 thousand because we bought some inventory. So a cache now has gone down from 2500 to $500. The other side was our inventory. Inventory is also an asset, so we just need to put that on the assets as inventory of 2000 dollars. So again, our totals for both sides balance, annular accounting equation works. Now let's have a look at our final example. So here we've made some sales of $4 thousand. So the accounts that would be affected would be our cash because we've received some money for the sales. We need to also reduce our inventory because we have sold all of it. And we also need to recognize the sales income. So you'd see that there are three accounts affected here rather than two, but it's double-entry system, isn't it? So I'd like to mention here that in double-entry system that needs to be a minimum of at least two accounts that are affected. It can be more it can be 34 or five accounts, but there needs to be at least two accounts that are affected. In this example that we're looking at, there are three accounts that are affected. So overall, they should still balance. So like I said, the three accounts that are affected, our sales income, inventory, and cash or accounts receivable. If you use the accrual system. Let's put this into our balance sheet again. So our cash has now gone up to 4,500. Remember, it was previously 500 dollars and we've made sales of $4 thousand. So our cash is now 4500. Inventory has gone down to 0. It was previously 2000, but we've sold all of us talk. So the left side of our balance sheet is 4500. However, the right side of a balance sheet is only 2500, so our totals don't balance. This can't be, let's jump back and look at our profit and loss. So we remember that we have made sales of 4 thousand. We've got our cost of goods sold, which was our inventory of 2000 dollars. So our net profit is $2 thousand. Now this profit is what's missing a non balance sheet and we need to bring it into debt in order to balance it. So in order to bring it up profit into our balance sheet, we need to put it through retained earnings. Because remember, retained earnings was the cumulative profit or loss amount. The retained earnings sits under equity. So under equity, we just need to add retained earnings of $2 thousand, which is our profit amount. Now, the right side of our balance sheet adds up to 4500 and our totals balance. So at this point, I'd like to reiterate that the retained earnings is the link to the profit and loss, which is why we brought in the $2 thousand, which was up profit from this transaction. So now you have a better understanding of double entry system and a few examples as well. At the end of this lecture you will find two attachments. One is the set of exercises for you to work through. Once you have worked through those exercises, you can look at the second attachment which will provide you with the solutions for you to check. So give it a go and I'll see you in the next module. Congratulations on completing another module. I hope you're getting some value out of this course. Are really appreciate if you could leave a rating and a review to share your thoughts. See you in the next video.

8. Quick Recap & Introduction to T-accounts: Welcome to the most interesting and challenging module of this course. But before we dive in, Let's first step back and have a look at the highlights so far. So in the first module we had a look at the why. Why is accounting so important in answering some of those key questions that business owners have when making those important business decisions and how financial reports can help answer those questions. We also briefly touched on how accounting softwares available and can help simplify the accounting and bookkeeping process for Business Honors accountants and bookkeepers. In the next module, we had a look at the what. So what is a profit and loss and what the components of a profit and loss are. You now know that income minus cost of sales minus expenses is what gives you your net profit or net loss figure. We then had a look at the cash and accrual accounting methods. And depending on which method you choose, there might be some timing differences. We also saw the advantages and disadvantages of each of those methods. Then we had to look at the balance sheet. You know, know, the three components of the balance sheet, which is assets, liabilities, and equity. Assets, is everything that the business owns. Liabilities as everything that the business owes to others. And equity is what's leftover in the business after the assets and liabilities have been cleared and is what's owed to the owner of the business, retained earnings. And do Newton's form part of this equity figure. Then we had a look at the double entry system and how each transaction should have at least two sides, the source and the destination, and how they should always be equal. Then we had to look at the holy grail of accounting, which is the accounting equation. You now know that assets equals liabilities plus equity. So what's next? Well, next we're going to look at the how, how do all these components that we've learnt so far come together and producing the T-accounts. And how do debits and credits work? Debits and credits are some of the most confusing topics for new accounting students. And we've tried to simplify this as much as possible for you. You can quickly understand this concept and get started. So let's jump into it. All right, so when I talk about T-accounts and debits and credits, I will keep referring to concepts that we've already looked at in the past. The first one being the T-accounts. So in the previous module, we use the T-accounts to explain the concept of the balance sheet where we had assets on one side, liabilities and equity on the other side, represented by the T in the middle. But in reality, we can have T-accounts for anything and everything else, to be honest. So what does that really mean? Well, if we look at the balance sheet, we can have T-accounts for each of the asset accounts, liability accounts, and equity accounts. So like you can see, under assets, we have cash, inventory and plant and equipment, and each of those have their own T-accounts. Similarly, liabilities have their own T-accounts and equity have their own T-accounts. The same concept also applies to the profit and loss. So we have income, cost of goods sold and expenses, and each of the accounts under these have their very own T-accounts. Now, you'll notice that I've got debits and credits inside these T's. And that's where we would like to introduce you to the concept of debits and credits because they work hand in hand with T-accounts. But before I do that, I would like to mention that accounting is generally all logic. You can always use logic to explain different components and apply different concepts and accounting. However, when it comes to debits and credits, we have to keep in mind of certain rules. And these rules dictate how debits and credits work and not logic. So you can see how Davidson credits could confuse people. But as long as you remember these rules, the whole concept of debits and credits will be very simple.

9. Debits and Credits Rules 1 & 2 - Simplest Explanation Ever!: So to introduce the first rule, I would like to go back to the concept of double entry system. We know that there are at least two sides of every transaction and that there is a flow of economic benefit from a source to a destination. So it's being one side and destination being the other side. All we're going to do now is replace the word source and destination, but the words credit and debit. So, so since the credit and destination is the debit, a couple of examples. So we as owners, lend some money to the business. The money is coming from us. So we are the source, which is the credit. The money is going into the bank account, which is its destination. And so that would be the debit. In another example, Let's say we have made some sales to our customers and they paid us some cash. So the source in this case is our customers. So the sales are the credit. And the destination, again is the bank account, which would be the debit. So this is how you can apply the concept of source and destination to understand debits and credits. From double-entry system, we also know that the two sides are equal and opposite. So that brings us to our first rule, which is debits equal credits. You already knew this concept before that the two sides must always be equal. And now because we've replaced the two sides with the words debits and credits, that forms our first true, which is debits equal credits. Next rule, we are going to look at how debits and credits are presented. So you need to remember that debits always go on the left side of our T and credits always go on the right side of the T. The words DR and CR. I just short forms in the accounting world for debits and credits. But the main concept here is that debits go on the left and credits go on the right. You need to remember that one isn't good or bad, or one isn't a positive or a negative, there are just two sides of the transaction. Think of it as two sides of a coin, heads and tails. One's not better than the other. They just are the two sides. Similarly, debits and credits are just two sides of the transaction, and one's not better than the other.

10. Calculating the Balance of T-Accounts: Next, let's have a look at how to understand the balance of a T-account. This isn't a rule. This is just a concept that we need to understand in order to be able to understand how to calculate the balance of each of these T-accounts. So we've just got three t-accounts of just any accounts. We don't have any assets or liabilities name TO and just three random T-accounts. In the first transaction, let's say Acumen one is debited by 1000 and account two is credited by a 1000. We've satisfied rule number one, because debits and credits equal, they are both for $100, will also satisfied rule number two, because debit is on the left side of tea and credit is on the right side of this T. So rule and 12 have been satisfied. Next, in the next transaction, we have got a credit to account number 1 of 500 and a debit to account number 3 of 500. Again, 12 has been satisfied. In the next transaction is a debit to account number 2 of 200 and a credit to account number 3 of 200. Now, how do we calculate the account balances? So let's say we start with account number one. You always subtract the larger number from the smaller number. So in this case, because we've got a high a debit balance, then our credit balance, the net balance of the T-account would be a debit. And it would be the difference between the two, which is in this case 500 debit, because that's the larger number. And account number 2, we've got credit which is higher than a debit. So the balance would also be a credit of the difference, which is $800. Account number 3, same concept, but in this case, debit is larger than our credit, so the balance would be a debit of $300. Now let's say we've had another transaction, switches affected all three accounts. So account number one has been debited by 100. Account number 2 has also been debited by 100, But account number three has been credited by 200. Rules 12 have still been satisfied. We've got equal amounts of debits and credits. And debits are on the left and credits are on the right. Now, let's obtain our balances. So account number 1 now has 1100 on the debit and 500 on the credit. So the balance here will change to 600, which is 1100 minus 500. Account number 2 will also change. So now we have a credit of 100 by the debit of 300. So the balance would be a credit of the difference, which is 700. Account number 3 will also change. So we've got a debit of 500, but a credit now, or 400. So balance will be a debit of 100. Alright, so we now know how to calculate the balances of the T-accounts. But did you notice that both account number 12 had debits? However, the balance for account number one went up, but the balance of account number 2 went down. That's where rule number 3 comes into play because there are some accounts that are normal debit accounts and there are some accounts that are normal credit accounts. And depending on whether they are normal debit or credit, these transactions will affect the balances accordingly. It's a lot of words. Let me simplify it for you. In the next row.

11. Rule 3 - Normal Debit & Normal Credit accounts (With a Special Trick): So like I mentioned, rule number 3 tells us how the different accounts behave in specific it relates to normal debit accounts and normal credit accounts. A normal debit account goes up and balance when it's debited and goes down and balance when it's credited. Think of it as a dish, a sweet dish. In order to make it sweeter, you'll add more sugar. And to make a less sweet, you might add salt. So it's the same concept here. If it's a normal debit account, in order to increase the balance, you would do more of the same witches debiting it. And to decrease the balance, you'll do the opposite, which is crediting it. A normal credit account, on the other hand, still follows the same logic. So to increase a normal credit account, we will do more of the same mature B2 credited to decrease the balance of animal credit account, we would do the opposite, which is debiting it. And that is rule number three. No debit account goes up with a debit and down with a credit. Normal credit account goes up with the credit and down with a debit. But how do we know which accounts are normal debit accounts and which accounts are normal credit accounts. Well, that's where I have a trick and it's called dealer. I will go through this in a bit more detail. But first, let's have a look at what the normal debit accounts are and what normal credit accounts out. So normal debit accounts go up with a debit and down with a credit. The types of normal debit accounts are all the destination accounts. So remember from rule 1, debit was the destination. So that's what we've got here. The destination accounts are dividends because that's amount being paid to the owners from profits. So the dividend is the destination. Expenses are another example of destination. So we pay cash from a bank account to a supplier's for the different expenses. So the expenses are the destination. These are costs incurred in order to generate some revenue. Another example is assets. These are items that we own in order to produce future economic benefits. So examines could be the cash in our bank account, that's the destination. So when VS owners put money in the business or when customers buy some of our goods, then all of that money goes into the bank account, which is the destination. Similarly, if we buy assets like dot and equipment or machines, they are also the destinations. So these are all types of normal debit accounts. We've got dividends, expenses, and assets. These are all destination accounts. Then we have normal credit accounts, which go up with the credit and down with a debit. Now credit accounts are the source. Remember again from rural one source was the credit. So examples of credit accounts are liabilities because these are money that's owed to others. So for example, if a bank lends us money, that's the source. The money is coming from the bank, which is a liability. Another example is equity, which is money coming from owners. So again, that's the source. And lastly, we have revenue, which is income coming from goods, sale of goods and services. So this money is coming from our customers, which again is the source. So liabilities, equity, and revenue are the three credit accounts. If I was to put them in a T as we always do, we have our debit accounts, which is dividends, expenses, and assets. If I pick the first three initials of each of these, we have DEA and we know that the debit accounts go up with a debit and down with a credit. Then we have credit accounts, which are liabilities, equity, and revenue. Again, if we pick the first three letters of each of these, we have L, ER, which is this. And we know that the credit accounts go up with a credit and down with a debit. So this is where dealer comes into play. That's the trick that I mentioned earlier. So the DEA of the de la represents the debit accounts, and similarly the LAR represents the credit accounts. D stands for dividends, E Fi expenses, a for assets, Alpha liability for equity, and alpha revenue. So this way by remembering de la, you'll also remember which accounts are normal debit accounts and which accounts are normal credit accounts. Once you know that, it's as simple as debiting or crediting them depending on which way they're going. So hope this simplifies the third rule, which is for normal debit and normal credit accounts.

12. Debits & Credits Examples - Making Sales in Cash & Accrual: Okay, so now that we know that three rules of debits and credits, let's actually make it a bit more interesting and practical and work through some examples together. When we look through these examples, we'll be looking at five steps. Will be given a certain transaction and we'll work through each of these steps one by one. In the first step will be looking at rule number 1, where we'll identify which accounts are impacted or what the source and the destination accounts are. Then in steps 2, 3, and 4 will be applying rule number three, which is the dealer rule. So we'll identify the appropriate category of the accounts that are impacted. So is it a dividend and expense, asset, liability, equity, or revenue account? And knowing this will know if it's a normal debit account or a normal credit account. We can then decide as to whether the account is increasing or decreasing. And using the steps above, we should be able to record the debits and credits using rule number two, which is debits on the left and credits on the right. So as you can see, these five steps already include the three rules that we've looked at so far. Now let's have a look at our first example. So in our first example, we as owners have provided 1500 and investment to our company polychaetes. So step number one would be to identify which accounts are impacted or the source and the destination of the transaction. So we know that the source is us as owners, which is known as equity. And the destination is the BankAccount, which is cash. So there's only two sides that are affected, one being cached and the other one is owner's equity. Then step 2 would be to determine if. So in our first example, we as owners have provided 5700 and investment to our business. So step 1 would be to identify the different accounts that are affected. We can tell that there are only two accounts that are affected in this transaction. One being the cash that's coming into the bank account, and the other side being the equity, which is owner's equity because the money has been lent by the owners of the business. So those are the two sides of the transaction. Then we'll work through steps 23 where we'll apply the dealer rule. So we need to identify the category of these accounts and whether they are normal debit accounts are normal credit accounts. So let's bring up our dealer. So we've got our dealer, but we've got TEA on the left, which are normal debit accounts, and Ellie are on the right, which are normal credit accounts. Dividends, expense, asset, liability, equity and revenue. Cash is an asset. Because it's money that's owned by the business. And asset is a normal debit account because it's sitting on the left side of the T. Equity, on the other hand, is, as the name suggests, equity and that sits on the right side of our T here. It's the e. So this would be a normal credit account. So once again, cash is an asset which has a normal debit account because it's on the left side of the T. And equity is equity and it's a normal credit account because it's on the right side of the team. So we've worked through step one, step two, and step three. Step 4 is to identify if the account is increasing or decreasing. So in this particular transaction, we know that the cash is going up because we've now got more money in our bank account. So cash is increasing. We also know that the equity is going up because we now all more money to the owners of the business, owes more money to the owners. So therefore, equity is also going up. So that's step number four, complete. Now we can put this into our T-accounts using our rule number two, which is debits on the left and credits on the right. So if we set up T-accounts for both, note that cash is going up, it's increasing. It's a normal debit account. So to increase a normal debit account, you would debit the balance, which is why we've debited the 1500 debit is on the left, remember? So we've debited cash by 1500. Owner's equity is the normal credit account. It's also going up. So to increase a normal credit account, you would credit that balance. So we're crediting 1500 under equity because it's sitting on the right side of the T and that's a credit. So we've debited cash by 1500 and we have credited equity by 1500. The totals of our T-accounts are asset would be a debit balance of 5000, and equity would be a credit balance of 5000. We've worked through our five steps now and we can see that the net result is that our debits and credits balance. So that's example number one. Okay, so now I would like to take this one more step further. We have looked at the five steps and may have clearly identified the debits and credits in our T-accounts. Now, let's pull this information through to our profit and loss and our balance sheet. In this particular example, we know that our profit and loss has not been affected. The husband no sale of money coming in from customers or we haven't paid for any expenses either. So there should be no impact on our profit and loss. However, there will be an impact on our balance sheet because now we have more cash in our bank account and we've also increased our equity by $1500. So let's have a look. So in our reports will know that our profit and loss as to all 0 because there has been no changes here. But in our balance sheet where we have assets on the left, liabilities and equity on the right. Our cash balance has increased by 1500. So we've got 1500 against cash. And our equity is also gone up by 1500. So we've got paid-up capital, also known as equity of 1500. I total debits and credits 1500. So it's all making sense. So that's how you see that the T-accounts then flow into the different reports on the financial statements. Now let's have a look at our second example. In the second example, we have borrowed at $1000 from the bank. So step one, as we did before, was to identify the different sides of the transaction. In this example that again, there are only two sides. The first side is the cash that's coming into the bank account. And the other side is the loan because we borrowed some money from the bank. So they are the two sides of the transaction. Now we'll apply steps 2 and 3, where we'll identify the appropriate category and whether these are normal debit accounts are normal credit accounts using D low. So as we saw from our previous example, cash is an asset which has a normal debit that account. So that's pretty clear. Alone now is a liability because it's money that's owed by the business to others. So loan is a liability, the L and D low. And that sits on the right side of our T, which is a normal credit account. So therefore, a loan will be a liability, which is the normal credit account. Next is step number 4, where we need to identify if the balances are going up or going down. So in this case, a cash balance of course is going up. We now have a $1000 more in our bank account. So cash is going up alone is also going up because now we owe the bank at $1000. So loan is also increasing. Now let's put them into our T-accounts like we did in our previous example. So without cash account, we will have to debit $1000 because cash is a normal debit account and because it's increasing, we will need to debit that balance. The loan is a normal credit account, and because it's increasing, we will need to credit this balance. So a loan will be credit of a $1000 credits on the right, which is why it's sitting on the right side of our team. Now if you sum up our balances for each of the T-accounts, we know that cash has a debit balance of 1000 and loan has a credit balance of 1000 at transaction balances. Again, let's put this through into our reports or profit loss and our balance sheet. Again, in this case, the profit and loss is unaffected, but our balance sheet has now changed from when we last saw it. So a cash balance was previously a 1500, which is what we had lent as owners to the business. Now, let's see what the cash balance looks like. So it previously was 1500. Now we have another $1000 that we borrowed from the bank. So the cash balance now do 1000, 500. The total debit is 2500. The loan is now a $1000 because we now have a loan that we owe to the bank of $1000. Paid-up capital, as before was 1500, which doesn't change. And therefore, our total debits and total credits balance. The total debit is just the cash account and the total credit is total from the loan and the paid-up capital. So $1000 plus 1500, which gives us 2500. So our debits and credits balance.

13. Debits & Credits Examples - Lending & Borrowing Money: Okay, so in our next example, we bought some stock or inventory for a business for $2 thousand and we've paid for it in cash. So the two accounts that are affected in this case would be the stock or inventory and of course the cash account. Now, we then need to apply our dealer rule. So we know that inventory is an asset account because it's something that the business owns. Similar to cash, which is also an asset account like we saw in our previous two examples. So they are both asset accounts, which are normal debit accounts because they sit on the left side of our tea. So inventory and cash are both asset and both normal debit accounts. Now let's see which account is increasing and which account is decreasing. So a stalk in this case is increasing because we now have more stock in our accounts than we did before. Therefore, stock goes up. Our cash balance, on the other hand, is decreasing because we've had to pay some cash in order to buy the stock. Therefore, cash is going down or decreasing. Let's now put this through into our T-accounts. So stalk is a normal debit account, and because it's increasing, we will need to debit this balanced by $2 thousand. Cash is a normal debit account, but it's decreasing and therefore we'll need to credited by 2000 dollars. Does that make sense? So cash being a normal debit account, remember rule number three, if it's a normal debit account, you debit to increase and you credit to decrease. So inventory was increasing. So we debited, cash is decreasing, so we need to do the opposite, which is crediting it. Therefore, we have credited cash which is on the right side of the team. If you sum up both parties, they now add up to 2000 and this transaction balances. Now let's look at our profit and loss and our balance sheet. Again, profit and losses and affected because we haven't really sold anything. But a balance sheet has changed. So our cash, which was previously 2500, has now gone down to $500 because we've had to pay $2 thousand to buy the stock. I inventory balance, which was previously 0, has now gone up to 2000 because we now have inventory that's worth $2 thousand. So basically we just converted some of our cash to get some stock loan account and a capital doesn't change. Therefore, if we sum up our debits and credits, they bought add up to 2500 and the balance sheet balances. Thanks. I would like to take the same example from before. So we've still bought stock for $2 thousand. But I would like to make it a little more complicated. So instead of paying the full $2 thousand in cash, we've only paid at $1000 in cash and the other $1000 are on 30 day credit. In other words, we have 30 days to pay our suppliers the remaining $1000. So in this particular transaction, there's not two, but three accounts that are affected. The first account is the stock. Inventory. Second is the cash account because we have still had to pay a $1000 in cash. And the third account that will be affected is the accounts payable that's in relation to the $1000 that's payable on credit. And the accounting world, any money or to the suppliers is called accounts payable. And therefore, that's our third account that's affected. Now again, let's apply our dealer rule. And we know from our previous example that bought stock and cash, our assets and our normal debit accounts. With our accounts payable is a liability account because it's money that's owed by the business to others. Therefore, it's the L in our dealers sitting on the right side, which is a normal credit account. So accounts payable is a liability, which is a normal credit account. Now let's see which accounts go up and which accounts go down. So a stock balance still increases by $2 thousand, and therefore it's going up. Our cash balance has gone down not by two thousand and ten hundred dollars in this case because we only paid 50% of the total in cash. Our accounts payable balance, however, is increasing because we previously did not owe any money to our suppliers. But now that this transaction has happened, we owe her $1000 to our suppliers. So our accounts payable balance has increased or a liability has increased by $100. So that's our increases and decreases. Now let's put them together into our T-accounts. So with our stock account, we're just going to debit that by $2 thousand like we did before. Our cash account is a normal debit account, but in this case it's decreasing. So we will credit it by one hundred, ten hundred dollars because that's all that we've paid. And our accounts payable is a normal credit account. And it's increasing and therefore will do the exact same, which is credit. Therefore, we will credit it by one hundred, ten hundred dollars. Now, if you look at the balance of each of these accounts, we can see that our stock has a debit balance of 2000. Cash is credited by 1000, and accounts payable is a credit by 1000 and our total debits and total credits balance. So this transaction works. Let's update our balance sheet in this case. So our cash balance has gone down by as much as it was previously 2500. And in this case we have only spent $1000 out of it. So a cash balance, and this scenario is one hundred, ten hundred five hundred. Inventory balance is still $2 thousand because we've got $2 thousand in stock. Our loan account and a paid-up capital hasn't changed, but now we have an accounts payable to our suppliers of one hundred, ten hundred dollars. So if, if we add up our total debits and our credits, they still add up to the same amount. And our balance sheet balances.

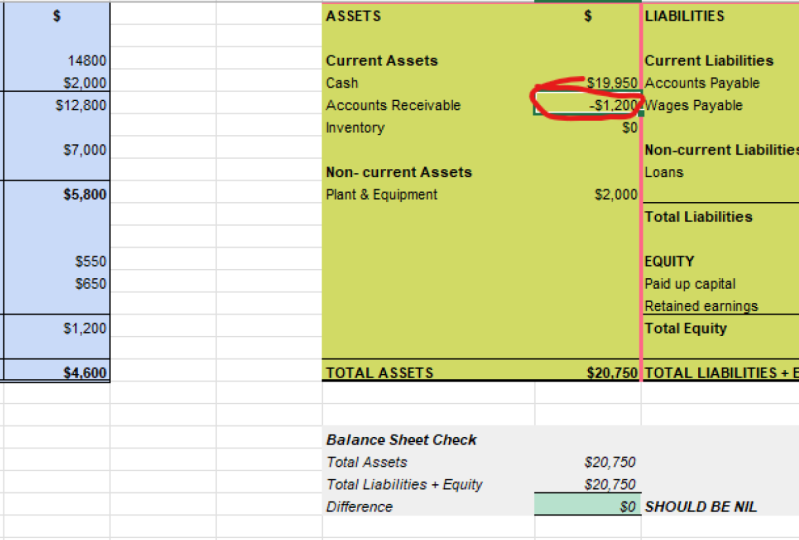

14. Debits & Credits Examples - Buying Stock with Cash & Accrual: In our next example, we have made some sales. So we've solved 4000 dollars of leads to our customers and they've paid all of it in cash. So when we make a sale, we need to think of it from two perspectives. The first perspective is obviously the sales perspective. And the second perspective is in terms of recognizing the expense. It will make a little more sense when I explain it a bit later. But first, let's have a look at it from the sales perspective. So in this case there will be two accounts that are affected. One would obviously be the cash account because we receive $4 thousand into our bank account. And the second account would be the sales because we need to recognize the income or the revenue for $4 thousand. So cash and sales are the two accounts. Applying the dealer rule, we know that cash is an asset which has a normal debit account. Sales is the revenue account. So it's the R in Dealer, which is a normal credit account. So therefore, sales would be revenue, which is normal credit account. We know that the cash balance is increasing because we have more funds in our bank account now. And we also know that our sales are, our revenue has gone up because now we've made some sales for our leads. So sales is also increasing. Putting this into our T-accounts, we know that cash normal debit account, if it increases, we need to debit it by $4 thousand. Sales is a normal credit account, which is also increasing, and in this case it needs to be credited by $4 thousand. So our totals balance here and our debits and credits both equal $4 thousand. That was from the sales perspective. Now remember I told you we also need to consider this transaction from an expense perspective. So if you think about what we covered a few modules ago where we went through the expense and the matching principle with expenses. We noted that when we make a sale, we need to recognize the corresponding expense. So, so far, when we bought the stock will be ported to the balance sheet as inventory. It did not go through into our profit and loss at all. But now that we've sold that stock and will receive $4 thousand for it. We need to move that inventory balance of 2000 dollars from the balance sheet into our profit and loss as the expense. So in order to do that, we need to consider the two accounts that are affected. So first account is obviously the inventory account because we now need to move that inventory balance from the balance sheet. And the second account that is affected is the cost of sales account. And if you remember, cost of sales sits on the profit and loss. So remember it's income minus cost of sales minus other expenses gives you your net profit. So inventory is a balance sheet account and cost of goods sold is an expense account on the profit and loss. So like I said, we're essentially moving that $2 thousand from our inventory to our cost of goods sold. So applying the dealer rule again here, we know that inventory is an asset which is a normal debit account. Cost of goods sold is an expense. So if you go back to d log, we know that it's the first E and D low dividends expense, right? So E is expense, which is a normal debit account. So cost of goods sold is an expense which has normal debit. We know we're moving that $2 thousand from inventory to cost of goods sold. So our inventory balance is going down. Our cost of goods balance is going up, correct? So therefore, we have reflected the two sides of the transaction. Now let's put them into our T-accounts. So in 90 accounts, inventory being a normal debit account because it's decreasing, we need to credit it by $2 thousand. Remember, $2 thousand is what we bought the stock for. And now because we're moving it from balance sheet to profit and loss, we need to just move that $2 thousand. Our cost of goods sold is a normal debit account. And because it's increasing, we need to debit it by $2 thousand. So from this perspective, again, debits and credits board balance by $2 thousand. Let's have a look on our profit and loss and a balance sheet so it make a little more sense. So now that we've made some sales, we've got $4 thousand in revenue. We've also got $2 thousand in cost of goods sold. This is what was sitting in inventory before. And now we've moved it from inventory to cost of goods, which is on the profit and loss. So we've got $2 thousand in cost of goods sold. This gives us a net profit of $2 thousand. Looking at our balance sheet, cash balance is now 5500. Remember before it was one hundred and five hundred and now we've made $4 thousand and sales that were received in cash. So one hundred ten hundred, five hundred plus 4 thousand gives us 5500. Our inventory balance was previously $2 thousand, but now we've moved it to cost of goods sold. Therefore, the inventory balance here is now 0 alone is still the same. Accounts payable is still the same and are paid up. Capital hasn't changed either. But we need to put in an amount under retained earnings. If you recall again from our previous modules, you remember that retained earnings is the link to the profit and loss. So anything that's a net profit needs to go to the balance sheet under retained earnings. So net profit in this case is 2 thousand, and therefore we need to put the same amount under retained earnings, which will be $2 thousand. Now, our debits and credits both balance and our balance sheet works. This is a slightly more complicated topic example. So if you feel like you didn't completely understand and feel free to replay it so it makes a bit more sense before you progress to the next example. In our final example, I would again like to do the same that I did before, where I picked up the previous example and made it a little more complicated. So we've suddenly $4 thousand of sales, but instead of selling all of it in cash, we've sold half of it in cash and half of it on credit. It's not. The words will receive $2 thousand from our customers in cash. And the other $2 thousand is receivable from our customers in 30 days time. So from a sales perspective, there will be three accounts that are affected. The first one would obviously be the cash account. Second would be accounts receivable. That's the accounting term for any money that's owed to us from our customers. And last, as we saw in the previous example, would be the sales account. We know that cash is an asset which has a normal debit account. Accounts receivable is also an asset which has a normal debit account because it's something that the company owns. Customers need to pay us money. So that's something that's owed to us as the business. And therefore, it's an asset which has a normal debit account. Sales, as we saw previously, is revenue, which is a normal credit account. We know that the cash balance is increasing, although not by as much. It's only going up by 2000 and still it is going up. And therefore, we've got an increase in cash. Our accounts receivable balance is also going up. We previously had no money owed to us from our customers, but now we have $2 thousand owed to us. Therefore, the accounts receivable balance is increasing and sales is also going up as we saw in the previous example. So if we put these through into our T-accounts, cash normal debit account increasing, therefore needs to be debited by $2 thousand, which is the amount that was received in cash. Accounts receivable also a normal debit account which is increasing and therefore needs to be debited by the remaining $2 thousand, which is the amount that's on payment terms. A sales is a normal credit account and it's increasing and therefore it needs to be credited, which will be for the full amount because we've stood main sales for the total for $1000. So only that we haven't received all of it in cash yet. Therefore, the sales will be $4 thousand. So if you sum up all our balances, this will result in a total debit of 4000 and total credit of also for $1000. Now from an expense perspective, like we saw in our previous example, that would be exactly the same. So will still move the inventory balance of 2000 dollars from our balance sheet to our profit and loss. I'm not going to cover that again because that process is exactly the same. So if we look at a profit and loss and our balance sheet now, the profit and loss is still the same. Revenue is $4 thousand. Cost of goods sold is 2000, which was moved from inventory to our profit and loss. So our net profit is $2 thousand, exactly as that previous example. Our cash balance, though in this example, wouldn't go up by $4 thousand. It's only going up by $2 thousand. Therefore, the cash balance is only 3500. Remember at the end of example three, we had 1500 and our bank account, and now we've had an additional $2 thousand in cash sales. Therefore, our cash balance has gone to 3,500. We have money or to us from our customers for $2 thousand. Therefore, accounts receivable is now $2 thousand. Again, we put the net profit figure in our retained earnings of 2000 and a total debits and total credits balance. So that's how you'd work with accounts receivable and accounts payable in these different scenarios. Hopefully that made sense for you and please feel free to work through the next examples on your own. I've also included some explanatory videos at the end of those, so you can look at how we worked through the solutions together. I'll see you in the next one.