Transcripts

1. Course Manual: So here's a quick overview una pretty much of course manual on how the coursework. So this is again the accounting on under an hour. Eso the quick guide is that you put out the hand out, so if you go through each section, you'll find a handout at the very beginning. Ah, we will fill out. They hand out together. The best way to learn is for you to ride it out by hand. Um, and the research has shown that there's definitely literature out there that says if you write it by hand, you learn it better. If you don't want toe, print the hand out and just want to follow along with lectures, you can totally do that. Um, I highly recommend putting out they hand out and then filling it out together with me. Our talk for over seven years and it's worked the best. But again, if you just want to sit back and watch the video lectures on your iPad or your tablet totally no problem with that, either. Some examples are we ask you to work through on your own. Um, I think it's a really great way to do this. I've taken Ah, lot of courses and through my bachelors and masters degree, like learning on your own is definitely the best way. So giving an example, you work through it on your own, and then we work through it together. So we will go over the answers together on those days. Example Problems. Ah, that being said, there will be a quiz at the end of each section at the end of each section to test your knowledge. So with that being said, let's go ahead and get started on the basic accounting equation.

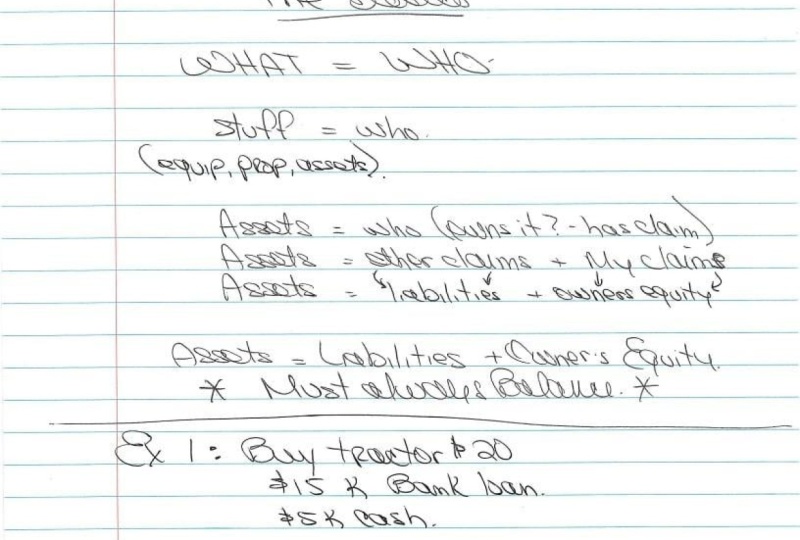

2. What = Who: So by now you should have printed out the section one hand out on day. It's called the accounting Equation. This is our first lecture. Ah, we're just going over the basics. So the basic equation is what equals who. Okay. And so what's another name for what? What is called stuff? Stuff equals who? So what is stuff? Stuff is going to be like a tractor. Assets assets also include property equipment would be another version of stuff, so stuff equals who. So then I just used the word that I'm gonna introduce, which is accounting word, which is assets. Don't be afraid of the word. It just called assets, and all it is is just the accounting terminology for it. So assets equals who is equal to who has clean. So who owns that? I think if you bought a tractor and you financed all of it, then the bank has claimed to it right. You don't own any of it. But let's say you bought the tractor and you pay for all of it in cash. Then you own all of it. And so that's the next part. So assets equals other people's claims, plus my claims so think of other people's claims is like owing the bank money, which is a bank loan, and then your claims as if you put down a deposit. So again, if you bought all of the tractor with your own money, then you have claimed to it. If you didn't put down any deposit and you just borrowed money from the bank, then the bank really owns that tractor. So then let's introduce another accounting term. Other people's claims is called Liabilities in Accounting, so the accounting terminology for other people's claims is liabilities. Um, and that's it again, just the terminology that accountant shoes. Um, So then let's add the last terminology is assets equals liabilities, plus other a new word for my people. Other or my claims is owner's equity. So owners equity are my claims. So if I bought the entire tractor than it would go their owners, equity would be my claim to it. So that being said, this is the basic accounting equation. So let's write it down here. The formal county equation equals assets equals liabilities, plus owners equity, and the way to think of this is essentially looking at it from a different perspective. You're looking at the asset, so you understand that you have the tractor and then that the other perspective is who actually owns that tractor? Do you own it, or does the bank own it, or is it a combination of the two and write this down? It must balance. This equation must always balance, so it must always balance and you'll see what I mean later on. But again, this is the formal accounting equation. Assets equals liabilities, plus owner's equity. Um, that being said, let's go on to the next lecture.

3. Let's buy a Tractor!: So this is just part of the same hand out. This is now a lecture to. So in this example, let's go ahead and buy a tractor, which is considered equipment in accounting terms. So the background we purchase a tractor for $20,000. We paid $15,000 by getting a loan from a bank in the remaining $5000 in cash. So we think about our equation again. What equals who? What? The left hand side is equal to our assets. The right hand side is who has claimed to those assets. Right? Um, so it's looking at the value of the asset and saying There's the bank, own it or do I own it or is this combination of the two So what we're gonna do here is go through an example together. So we purchase a tractor for $20,000 on the left side, the asset is worth $20,000 we know that now we're just looking at it from a different perspective. So the assets were $20,000. But now we're looking at who has claims, right? Who has claims to this? So who has claims is we got a $15,000 loan from a bank which is here. $15,000 loan from the bank in the remaining. We paid in cash for $5000 in cash. So take a second to think about who owns the asset who owns a tractor. Hopefully you got it right, and we own $5000 of it in the bank owns $15,000 of it. So this tractor on the right hand side, we're gonna divide it down the this part and say that we own $5000 of it in the bank owns $15,000 of it. So what that breaks down to is, let's write down our formal accounting equation again. His assets, which is equal to $20,000 equals liabilities, which is I told you several times, like the bank owns it. So that's a liability to the bank owns a 15,000 plus owner's equity. So our equity in that is $5000. So our ownership of this tractors $5000 what did I always say? It must always balance. So with that being said, does it balance? If we wrote it down? $20,000 equals 15,000 plus 5000 which is equal to $20,000 so that the county in question does balance again. This is just to show you, if we bought a tractor, we're looking at the asset side, which is $20,000 in assets. And we're looking at who has claims to those things, which is the liabilities plus owner's equity. So if we have a strong understanding of what equals who now, in the formal accounting equation, which is down here, assets equals liabilities, plus owner's equity. So the next example I'm gonna ask you to work on her own, So this will be the beginning of lecture three. Let's buy a vehicle in the background is we purchase a vehicle for $30,000. We paid $27,000 by getting a loan from the bank and the remaining $3000 in cash. So write out the accounting equation for the above transaction. So that of the lecture three. I'm gonna let you get it started on that, and then when you're ready on you do it on your own, then start lecture. Dream will go over together

4. Let's do an example!: So this is the beginning of lecture three. So this is just another example and hopefully try to do it on your own. But if not, let's go ahead and do it together. So let's buy a vehicle. So another form of equipment. The background is we purchase the vehicle for $30,000. We paid 27,000 by getting a loan from bank and the remaining $3000 in cash. So write out the account in question for the above transaction. So the county equation is what equal to that's the informal version. The formal version, Hopefully, you know by now is assets equals liabilities, plus owner's equity. So the task was right out the accounting equation for the above transaction. So our asset is equal to $30,000 equals liabilities. How much do we have from liabilities? How much do we owe other people in this case, the bank? Hopefully, you got a right You probably did, which is $27,000 plus owner's equity owners. Equity is how much do I own of this vehicle I own, and you got it right. $3000. So that's just a quick example of the accounting equation, and now you understand it. Assets equals liabilities, but stock oh, plus Owner's Equity, our assets worth 30,000 and it's made up of who has claims to that. The liability side is 27,000 and that's the bank, and we own $3000 on it again, just a very quick and simple example for you to understand the county in question.

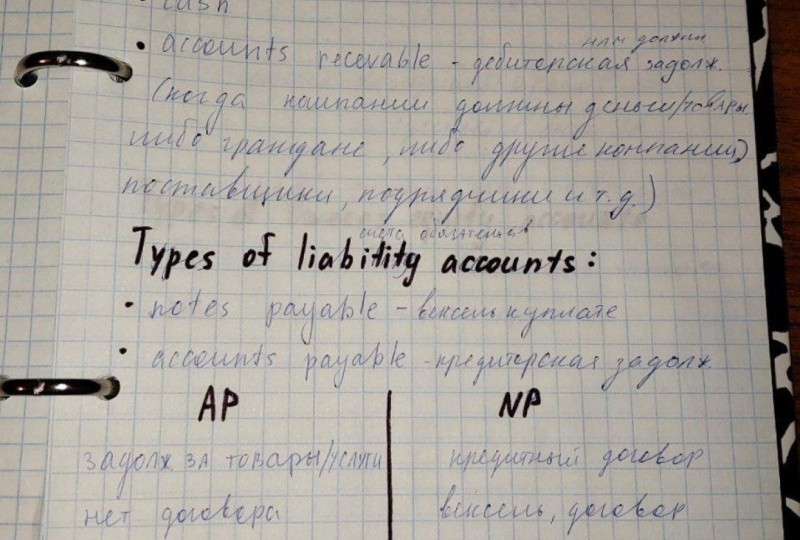

5. Understanding Accounts: So now we're on the lecture Four, which is understanding accounts. So we're gonna go over type of assets, accounts, type of liability accounts and types of owners equity accounts. The reason why I want to go over this is just so you can start understanding the terminology and seeing the terminology. So type of asset accounts. We already went through one. So hopefully you can name it. Um And it's gonna be equipment, so types of equipment, our vehicles, tractors would be an example. Another type of asset account is cash. Hopefully, every company has cash and they should always have cash. The next one would be accounts receivable. Now, I'm not gonna go into the definition of the thing. So if they're self explanatory, you understand them. Great. If not, we're going to explain them later on. In this in the next 45 minutes or so. Eso that that's another type of asset accounts type of liability accounts include notes payable. So this is like payments to a bank, for example, and then accounts payable which are like payments to vendors. We owe money to vendors. So then type of owners equity accounts is paid in capital and then net income again, We're gonna go over the definition. So if you don't understand something, mainly I just want you to see it. So you're not scared the next time you see it. So the last thing I want you to do is write down the account in question yet again. Yes, I know. But it's very important that you understand this. So assets equals liabilities, plus owner's equity and just below, make sure it must balance. So what? That said, go ahead and take the quiz. I'm almost sure you're gonna get 100 if you did this hand out together in the test, your knowledge. But with that being said, let's move on to the next section.

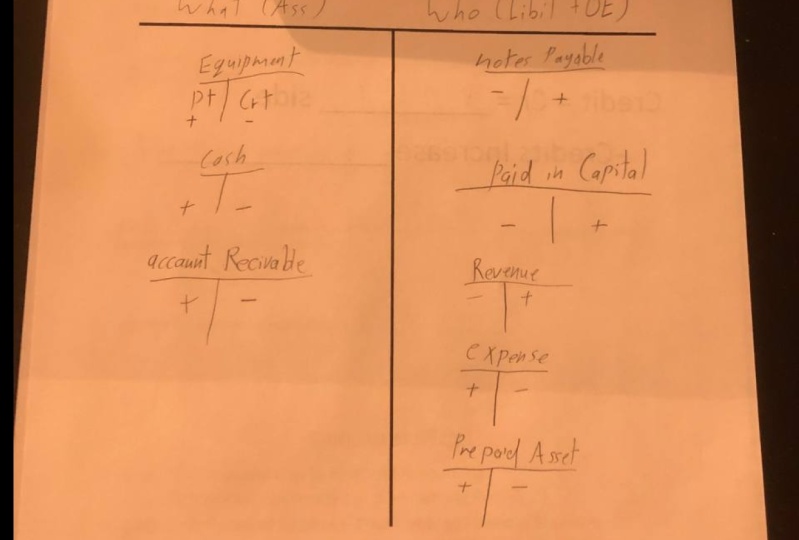

6. Debits and Credits: So now we're gonna go over that debits in the credits, and we're to de mystify them because I'm sure a lot of you've heard debits and credits before and now winning over what they are and it's bashing pretty darn simple. So at the end of this lecture, you'll have a pretty good understanding of it. Obviously, by the end of this course will have a very strong understanding of debits and credits. Just like you know, this is generally this is always done on a computer, not general. It's always done on a computer. This is a graphical or picture representation of it. Um and so the reason why we present it like this is so you can understand the concept. If you decide to pursue a career in accounting, then what will happen is that you will enter these things into a computer. But again, you won't be able to do that unless you understand the concepts behind it. So this is what we call a T account because it looks like a T. So hopefully you've again put out your hand out. So this is what we call a T account. So what, We're gonna right on the top here is winter right on the left hand side. What? Which again we know means assets and on the right. And so I want to write who, which is, who has claims, which is gonna be our liabilities in our owner's equity. And so hopefully you're writing this down, too. So with that being said on the left hand side went right down some types of asset accounts and we already went over some, right, so equipment would be here down here we can we can write cache. And we're just, you know, riding it over are drawing the smaller T counts and on the right hand side with write downs , types of liabilities which we over win over some notes payable and then paid in capital. So now you see, why introduced, um, the terminology in the previous example previous lecture. So this is now the second time we've seen that the more more you see it, the more more comfortable you're gonna feel with it. So these are what we call debits and credits. Um and so the debit side is always the left hand side, so this is gonna be the debit side and the right hand side will be the credit side, okay? And to increase them, what we need to do is follow the side that it's on. So for assets to increase them, we debit it because it's on the left hand side. And to decrease it, we use the credit and to increase notes payable, for example, since on the right hand side, we use the right hand. So we put a plus sign over here paid in capital increased paid in capital. We use the plus side, which is, um, the credit side, the right hand side. So again, this is just the concept. It's gonna come together very quickly here. So with that being said, ah, please fill this in with me. Debits equals abbreviation for debit is D are just in case You ever see that? So you know, and it's always equal to the left side or the left hand side. Okay. And debits increase assets Credits is, um is CR, and credits are the right hand side or the right side and credits increase liabilities and owner's equity. And we just went over that above. So again, a debit is abbreviated d r. It's the left hand side debits. Increased assets credit equal CR, which is equal to the right hand side and credits increased liabilities and owner's equity so you can see that look again. OK, so assets equipment we debit it, which is the left hand side. It increases it and liabilities to increase it. We must credit it, which is the right hand side paid in capital. Same thing right side, which is a credit is the way we increase it. Credit equals C R, which is the right hand side credits, increased liabilities and owner's equity. So with that being said, let's go through an example together. Background. I put in $10,000 into a checking account in open a brand new business. I then purchased the tractor for $5000. I pay for the tractor using $5000 in cash. So what we're gonna do is we're gonna make the tea counts for this. OK, so we're going to use our formal accounting question cause I think you're used to it now. Assets equals liabilities, plus owner's equity. So the first thing that happens is I put $10,000 into a checking account, so that's cash So let's draw a little t count for cash here and open a brand new business. Okay, so what? Two accounts are affected? First it's gonna be cash. And we know that the other account is because we own all of it. We own all of this who has claimed to this cash and we do is going to be paid in capital. I'm writing it over to the right because it's part of the owners equity accounts so paid in capital. So what happened is we have $10,000 in cash. So how do we increase cash? Let's go slow and go through this together will still finish in under an hour to increase in asset. Which passage cash is We debit it. So we go into the left hand side. So cash $10,000 and then paid in capital to increase that. We credit it, which is the right hand side for $10,000. Hopefully you understand that. And now move on to the next part. I then purchase a tractor for $5000. I pay for the tractor using $5000 in cash. So that would be equipment draw the T count for that. And then we just bought a $5000 tractor. So hopefully you heard that we will increase this herd is And that's what you heard in your head and which you probably did. And that's probably what you thought. And you're right, that goes up 5000. How did we pay for that tractor? We paid for that tractor using cash, so we have to reduce cash. So to reduce it, we have to credit it, which is $5000 over here. So what that has now is let's total this and then checker accounting equation. So total cash on hand will be $5000. So it's 10,000 minus five because it's 5000 equipments 5000 and paid in capitals 10,000. So now let's see if our accounting equation sorry that we owe our county equation works. So our assets equals the 5000 here. Plus, the 5000 year, which is 10,000 is equal to our liabilities, which is zero plus our owner's equity which paid in capital part of Owners equity is 10,000 and as 10,000 equal 10,000 the answer is yes. Sorry. County equation balances and it must balance, as we said in as, Oh, that is our first step in understanding debits and credits. So now you understand debits and credits, and you understand that the left hand side is always a debit and the right hand side is always a credit. Um, so with that being said, uh, let that student her head for a few minutes and let's move on to the next lecture.

7. The Trial Balance: So now let's go over. Um, we're in lecture. Six down. Let's go over an example. Eso when interest the trial balance and work a little bit. Work with MAWR with debits and credits and t accounts. So the background is. I put $10,000 into a checking account and open a brand new business. That should sound familiar. It's the same examples above. I then purchased a tractor for $5000 in cash. Again, it's familiar. Same example. Um, and as I say that next line, same examples above. But now I borrow $6000 from the bank to get mawr cash. Okay, for the first step is, let's make the tea counts for each account. Okay, so the first account we're gonna have is cash. Make a T account for that, uh, and then toe open up a new business. And so on the right hand side, I'll have paid in capital. I really love, um, introducing the same example over and over so you could really pounded into your head and really understand it. Okay, let's make this a T account. That looks better. Um, so $10,000 in cash paid in capital is up by 10,000. Hopefully, you remember that. We debit cash, um, to increase it and we got it. We have to credit paid in capital to increase that. Um, I then purchased a tractor for $5000 in cash. So the equipment is here. That's an asset account. How do we increase in asset account? We debit it, which is Deb. It's always on the left hand side. So $5000 here. How do we reduce an asset account? We have to credit it. And that means on the right hand side, because we paid for the tractor. The equipment with $5000 in cash. So now we borrow $6000 in the bank to get more cash. So what do you think? That IHS. You're right. What it is is a liability account on what we call it. Isn't notes payable? Notes payable is a liability account. What we do is we borrow $6000 in the bank to get more cash. So the first thing is, what do you think cash goes up by $6000? Okay. How do we make cash go up? We debit it because it's an asset account, which is the left hand side? Notes payable. Now think about it. Knows people's a liability account. Flip back in your notes. How do we make a liability account go up? Because we owe the bank money. You're right. It's $6000 credit. So we credit that for $6000. So that's it? That's all of the transaction. That's our T count. And now what we have is 40 accounts, and now we have to some each account, which is step two. So step one is done. Step two, we have to summit. Okay, so we don't have to really some paid in capital notes, payable or equipment, because there's only one transaction, so, really, we only have to do to cash. So to sum cash, we have 10,000 plus the 6000 which is 16. We minus the five. We subtract the five, which leaves us with $11,000 in cash right over here. So our total is $11,000 in cash. Okay, so now with that being said, we have some to each account. So now what we have to do is make a trial balance. Well, like son, I don't know what a trial bounces. Well, that's what we're gonna do right now. So all the tribe ounces is the check to make sure our accounting equation works and what it is is just a listing of every account. So what we do here is we write down our account, which is cash and what we don't have here do a line you should do a line to. We're gonna have a debit and a credit balance. And this is what a trial bounce looks like out of the computer out of the software that most people use that everyone uses, really? So cash has a debit balance of $11,000. Then we have equipment which has a debit balance of $5000 debit balance because on the left hand side, so if you're thinking that it's because it's on left inside, so then we'll go to notes payable. That has a balance of $6000 it's a credit because it's on the right hand side over here and then finally paid in capital, which is has a credit balance of $10,000. Okay, so now you are debit. Seek war credits. This side has 16,000. This side has 16,000. So yes, it does. Let's do one more check. Okay? Because I want you to see it all tie together. So we made the trial balance, and this is the child balance right here, which is a listing of the accounts, and that doesn't have a debit balance or credit balance. And it does tie what it does balance. So now let's just quickly write out the accounting equation. Assets equals liabilities. I'm a shorthand. It plus owner's equity on the shorthand. That too. So our assets equal right here, 16,000 0 sorry. Right here. 16,000 and there are liabilities equals 6000. And our owners equity was 10,000. So now the 16,000 equals 16,000 and it does Okay, so because 22,000, 16,000 it works. So this is also equal to it down here. So again, our trial balances a listing of a recount and seeing if it has a debit balance or credit bounce. So with that being said, let's move on to lecture seven. Let me give you a little preview. Lecture seven is an example that I want you to do on your own. So let's do lecture seven on your own, and then we're gonna do it together once you start lecture seven.

8. Example together!: So this is the beginning of lecture seven. We're gonna go to another example where we make a trial bounce. The background is I played $13,000 into a checking account and open a brand new business. I then purchased the tractor for $3000 in cash. Now I borrow $2000 in the bank to get more cash again. This example is very similar to the number, the ones above, with numbers being changed. But again, I wanted to do it together. And hopefully you did it on your own. Because that's the way you learn. So let's make the tea counts for each one. Okay, so I know the first t count I need is cash. And then I open a brand new business so paid in capital I purchased hope. Sorry. So then I put $13,000 into to the business, So $13,000 in cash and then paid in capital was up by 13,000. Hopefully, by this point, you can remember and you see that increase paid in capital? We credit it, which is the right hand side. Go back in your notes if you forget that. No problem on that. That's why have you put out these notes? I then purchased the tractor for $3000 in cash. So down here on the right equipment and I purchase it for 3000 and I use cash. So that reduced cash. I credit it for 3000. Now, I bar 2000 from the bank to get war cash. Okay, so you're right. That's called notes payable to increase notes payable. Because I'm borrowing money, I have to credit it. So you're right on that to 2000 and I increase it. The amount of cash I have. So now we have made the tea counts for each account. So now it's some each account. So the only one we have the sum is cash, cause it only that's the only one with multiple transactions. So 13,000 plus 2000 and 15 minus three gives me 12 $12,000 in cash. So with that being said now, we have to make the trial balance. So trial bounces just a listing of accounts and then do I have a debit balance or credit? Bounds the cash? I have a debit balance of 12,000 equipment. I have 3000 notes payable. All right, a little bit neater for you. Sorry about that. Notes payable. Have a credit balance of 2000 and in paid in Capital, I have a $13,000 balance. So on the left side, on the debit side we have 15,000 and then on the credit side we have 15,000. So our trial balance balances, and that's why we make a child balance. And that's why the computer does, too. To check the balance is so. And then let's do our accounting question really quick, and I'm gonna show you a little short hand. Assets equals liabilities, plus Owner's equity. Obviously, that's just an abbreviation. Assets equal 15,000 liabilities equal 2000 and the owner's equity equals 13,000. Does this match does it balance 15,000 and 15,000 here? So it does. Doesn't it make you happy? So that being said, let's move on to the next section

9. The Balance Sheet: So hopefully Verdy you did well on the quiz. First of all, on section three, if you have your hand out in front of you, should have gotten 100 which is my goal for you. This is Section four, lecture eight. So we're going over what the balance sheet is. You probably heard that term the balance sheet. It's a financial statement and we're gonna go over it, and now you're gonna know what it iss the balance sheet going over the definition. The balance sheet shows the financial position, assets, liabilities and owner's equities of the company at a point in time. And that's really important to understand. The balance sheet shows the assets, liabilities and owner's equity the financial position at a port point in time. So we usually measured at the end of every year. But if you're about to buy a business, then you'd want to know what the financial position of that company is at that point that you're about to buy it. Okay, so again, very important to know. So now let's do let's create a balance sheet together. So the background is. ABC company has $12,000 in cash, a $3000 tractor, $2000 is owed to the bank and there's a 13. There's $13,000 in owner's equity. The current date is January 31st 2020. Making balance sheet. So what I want to show you is on the balance sheet. Always have the company name. So at the top you want a list what it is. It's a balance sheet and then the date that the balance sheet is prepared. So this is the point in time that point in time, you should write that down. Okay, so now all we have to do is list out their assets, liabilities and owner's equity. So the assets that we have our cash $12,000 a tractor, which is equipment for $3000. The liabilities we have is we owe the bank $2000. That's and notes payable for 2000. And then we have Owner's Equity, which is $13,000. So we have total assets of and this is this line here. 15,000 total liabilities and Owner's equity of we add the two plus the 13 is $15,000 so you can actually see the accounting formal equation on the balance sheet. Total assets equals liabilities, plus owners equities and then cool that it's actually on the balance sheet. So now when you're looking at Balanchine's of other companies, you can look and check to see if that's right or not. Um, and so that is the balance sheet. Very easy. Ah, that's the end of this lecture and of the quit, I mean and of the section. So now you have a quiz over this, but that's has that's as easy as a balance sheet is again. Put the company name at the top that it's a balance sheet, the point in time that the balancing is measuring and just list out your assets. Have your total assets, your liabilities, your owner's equity and then total liabilities and owner's. That's it. Now let's move on to the next lecture after you take the quiz. Good luck on the quiz

10. Making Money and Revenues: so hopefully you did well on the quiz. And now we're going to Section five, which is lecture nine, hopefully printed out the hand out. So making money in what we call revenue. So another word for making money is when we just went over it. It's called the revenue. Okay, so now let's go through an example. Obviously, always the best way to learn. We make money by doing consulting services. We charge $500 to a customer to do some consulting around farming, so, you know, to teach them to farm better. We were paid in cash. Our current account balances are as follows Cash. We have $12,000 tractor. We have 3000 notes payable to the bank 2000 and owners Equity 13,000. How do we make a T account for the $500 of revenue in the above example? Okay, so let's just go and make a t count for all these accounts just really quickly, because it shouldn't take that long. Cash $12,000. The tractor, which was just gonna call equipment 3000 on score back up here, notes payable, which hopefully you remember is a liability which means 2000 and Owner's Equity. We have 13,000. So you may be saying, Son, how do you know that stuff goes on the left side of the right side? We'll remember that cash is an asset account, and so we should always keep it on the debit side, which is the left hand side liabilities and owner's equity. We keep it on the right side, which is the credit side. So the next question says, How do we make a T count for the $500 in revenue in the above example? Okay, so we were paid in cash. So the first thing you should think about is did cash go up? Yeah, we did $500 consulting him. You have $500 in cash, so $500 in cash went up. So now the question is the revenue. Where did the revenue go? Well, the revenue went to our company. And when you write it out over here for revenue and to increase revenue, we credit it. And so we put $500 over here. So you're like, son, Why did you credit revenue? How did you know to credit it because revenue in the end will flow in tow. Owner's equity. Okay, so it behaves like owner's equity. So to increase owner's equity, we put $500 into it. We credit it. Okay, So to increase owners equity and credit it to increase revenue, we credit. Okay, that's verily important. Really important to know. Um, so that being said, that's the end of this lecture. Let's move on to the next one.

11. Spending Money and Expenses: So now we're in lecture 10 which is spending money and expenses. Now we don't learn another accounting term. Another word for spending money is expenses And give you a hand up there just like I did with refugees. So the background using the same example, we now have to pay $200 for a gas bill. We pay this amount in cash. How do we make a T count for the $200 in expenses? Okay, so since we're building on this, I'm gonna actually scroll back up and use the same information so I don't have to redraw the tea accounts, and neither do you. So we spent $200 on our gas bill. We paid it in cash. So what What entry do you think has to happen? The 1st 1 we know is cash. Cash went down by $200 cause we had to pay our utility bill. Okay, so over here, we're gonna write $200. That's going to reduce our cash. Crediting cash reduces it. So now we have expenses. So we have a $200 gas bill. So what we have to have is we don't have an expense account yet We're gonna write it down here. So here's a new T account. So this is expenses and we have $200 in expenses. So the question you should ask yourself is, Where should I put the expenses? Will do it by debit it, or do I credit? The answer is that you debited in. The reason why is because revenue and expenses will flow into owner's equity. They flow in here, okay? And so we're reducing owner's equity because we're paying out money. We're paying out expenses. And that's why we debit. Because if we were to debit owner's equity, that's what we would do to reduce it. It's gonna make a lot more sense very quickly here. So that's what we do. We debit expenses for $200 that's how we make the T count for that. Um, and that's, um, yeah, I mean, we debit expenses to to increase expenses, which eventually reduce his owner's equity, which you'll find out in a second here. So to increase the revenue account, I want to reiterate this to you. To increase the revenue account, you must credit the account and to increase an expense account. You must debit the account. And this is why we have the notes so you can always go back to this. So now with that being said, we move onto the next lecture.

12. Net Income: So this is beginning of lecture 11 and we're gonna go This thing called net income, which you've already heard, um, during a previous lecture. And this is a reason why introduce it to you then. So this is now the second time you've heard it. So net income, what is Eagle Net income equals revenue, which we just learned minus expenses, which we also just learned. That's it. That's all net income in. So whenever you hear the term, net income is just revenues minus expenses. If we made $500 from consulting, which is equal to our revenues and spent $200 on our gas bill, which are expenses, what is our net income? Obviously, this is from the previous example. So net income, That's right, it out here. Net income equals revenues minus expenses. So let's do this together. Our net income is equal to revenues of $500. I'm getting that from here minus their expenses of 200. I'm getting that from here, which is equal to $300. So are net income in this example. Is he going to $300? Eso you probably got a right and you finished before me, and that's no problem. I like it when you understand it. The income statement measures income or profitability for a period of time. Okay? Which now if you think back the balance sheet measures it at a point in time, the income statement measures over a period of time, usually one year. So now let's make the income statement. Assuming it's the end of the year now in its 12 31 2020. So all in income statement is you show your revenues 500 you show your expenses and you can list out what kind of expenses you have. It's up to you $200. Um, in this example, it's up to you. Cos have the different types of revenues they have. So consulting revenue, selling other products, revenue and then expenses would be like utility expenses, rent expense. They break it out in this case because it's so simple. We're not gonna do that. And then you have your net income $300 and you're gonna say, Yeah, so that's really simple. And it is that's what an income statement is, and that's why we have this courses. So you understand it Um and we simplify it for you. So that's an income statement. You do revenues, you subtract out your expenses and you show your net income. So the net income for this business was $300 for the year. Eso that being said, let's move on to the next lecture.

13. Tying it all together!: So this is lecture 12 and want to do something really cool here when it's high, the income statement and the balance sheet together. I know that sounds really nerdy. Sorry about that. I am an accountant. And so anyways, um, and you'll hear that term. If you decide to pursue accounting, you hear the term tying it out. Ah, lot in so many ways we're gonna tie the income statement on the balance sheet together. So it says, using the above example and continuing that example. You know, I like to do that. Let's answer the question below the trial balances. Cash 12,300 tractor. 3000 notes payable to the bank 2000 owners Equity 13,000 and net income, $300. And just so you see where those numbers came from, the cache of 12,300. Okay, so let's go back up or for you. You're gonna flip back to the previous page. Where did they get 12,300 or where did we get it? Cash is 12,000 plus. The 500 is 12,500 minus 200 gives us $12,300. So that's what? We got the cash. So let's again flip back to this page. If I were you for me, it's gonna scroll down. So that's where we got the cash of 12,300. The rest of the counts are very easy. But now, net income. I'm introducing something kind of new here. We win over net income of $300 here. But look on our T counts. We see it too. That's where I said that she's gonna become very obvious to you. Revenue minus expenses gives us our net income. Here we combine these two accounts of $300. Okay? And that's in our trial balance. It's our $300. Notice it. That's a debit or credit. You're right. It's a credit. What credits going to do is increase owner's equity. You're right. So now let's see how that happens. It's gonna be pretty cool. So again, with with a balance sheet, we always put the company name ABC Company. We put Balanchine and we put as of a certain point so it's 12 31 2020. So now we write out our assets, we have cash 12,300. I'm not trying to write a little needle. Here we have our equipment, which is our tractor. Just $3000. We have our liabilities, which is notes payable just $2000. And now we have Owner's Equity. But here, Owner's Equity is equal to paid in capital of 13,000 and our net income for the year of $300. Hoops no common there. You race that, so you'll get confused. $300. So now the question is, does it balance our total assets equal $15,300? Our total liabilities and Owner's equity equal $15,300. It's or assets equal are liabilities. Post stockholders equity. Now let's take a second. Let's see just what just happened. Okay, so had the income statement interact with the balance sheet? Look, our income statement is here. This is the income statement for ABC company. Here's the $300. I'm gonna keep drawn this line so you can see, connect and literally see connecting your head here of $300. So the income statement for the year ends up in owners equity. And so that's what I was saying. That when you debit expenses is the way to increase expenses because it interacts with the owner's equity. Look, net income interacts with owners equity. And if you go back up and this is our final tie out, revenues and expenses flow into Owner's equity are total owners equities 13,300 because this is the net income. So now you're seeing it all tied together. Isn't that pretty cool? I mean, I know that sounds very nerdy, but hopefully you think that's pretty cool. So that's the assets. Equal liabilities, stockholders Equity. That's our balance sheet, and it ties out, and that's what we want. So now go and take the quiz. Pretty sure you're gonna get 100 if you did this time with me and you have your notes in front of you. So, um, hopefully that sign of a good teacher, Um, but more importantly, it's a sign that you're actually understanding this information, which is awesome.

14. Timing Matters!: So this is a section six handout lecture. 13. I know we're actually coming close to the end, and, you know, I'm gonna miss all of you all too. So the timing of revenues and expenses So we're gonna introduce some new accounts here because it's really important that you do understand them. Um and so it's important to understand that profit does not equal cash, okay? And we're gonna go through three examples out here with revenue in which we were paid before we did the work. At the time we did the worth. And then after we did the work, OK, so we did perform some consulting services and we were paid before we did it were paid at the time, and we were paid after, and you'll see the difference in the examples. So the first example is we were paid $200 cash for consulting services, but we have not performed the work yet. Therefore, we receive the cash before doing the work. So what accounts are affected here? So our tea accounts here are cash, obviously. And our second account you don't know, right? It's like, what is that account? So the account is actually called unearned revenue, and I'll explain it in a second. So unearned revenue is actually a liability account. So let's go. Let's just write it down first. So the cash went up by $200 but our liability count, how do we increase the liability count? You're right. We credit it for $200. So you're like, son, why is it a liability? Well, because we actually haven't done the work yet. So before we have done the work, they can come back to us and they can say, Hey, you haven't done the work. I want my $200 back and we'd like, from a legal perspective, have to give it back to them because we haven't We haven't done anything yet, So that's the reason why receiving money before you do. The work is actually called unearned revenue, which is a liability account. So now that you understand that, so let's say that were paid $200 cash for consulting services at the same exact time as this service was provided, therefore receive the cash at the same time of all work. Well, we've done several examples like this. Okay, so are two accounts would be cash. Just $200 in this case would be a revenue account. And how do we increase our revenue account? We credit it for $200. So in this case, because it's simultaneously done, we literally finish. Our consulting services were paid immediately. There is no difference here from other examples that we've done so receiving it at the same time. So now when introduce a new account, another new account. We performed our consulting service, but we were not paid $200. Therefore, we're waiting on the cash and were being paid after the time of work. So I'm gonna write the T count cashier, but does anything go in there? No, we didn't receive anything. So what is the asset account? The acid account is actually called accounts receivable. You probably seen this and you're like, Son, I know what to do. We're gonna debit accounts receivable for $200. And you would be exactly right, because it's an asset account and we're gonna receive this money at certain at a point later on. Um and then the other question is, Did we perform the work yet? Yes, we have. And that's $200 okay, and so that's where it is actually earned. So this is earned revenue, and that's the $200. So this is what happens when you receive the money after the time of work. So this is the reason why profit does not equal cash is because we could be doing tons of consulting work right for a bunch of different clients, and we might not get paid. Most likely we will, because it's accounts receivable. But that's where you have to understand that profit on the income statement does not equal cash. Until we receive this money, we actually haven't got the cash it. So it's the same exact thing with expense. Examples is that we could pay for the expense before at the time of incurring the expense. And then, after we occur, the incur the expense. So let's go through these examples. We paid two and draws for utility bill, but we have not used any gas or electricity yet. Therefore, we paid for the expense before incurring the expense. Okay, so what happened here? We pay $200 in cash. So here's our cash account. It went down by $200 but we haven't incurred any expense yet because we haven't used any gash in so well. That is called is a prepaid account. So it's called a prepaid asset, and that went up by $200 because that's what happened. We nothing's actually happened yet, So that's why we have a prepaid asset of $200. If we didn't use any gas or electricity, we can ask for that money back. And so that's what happens when you incur expense or you pay for an expense before actually incurring it. So at the time off, we pay $200 for the utility bill, this example to we paid $200 for a utility bill, and we consume the gas electricity at the same exact time. Therefore, we paid for the expense at the same time, time as incurring the expense. So what are T counts here? Cash goes down by $200 our expense account is here. And do you remember how to increase an expense account? We went over this in the previous section. You're right. You debited by $200 that's it. So that's incurring it at the same exact time, which is the examples that we've used so far. So our 3rd 1 is we incur $200 for a utility bill, but we have not paid any cash at this point. Therefore, you'll pay for expense after we incur the expense. So does cash get affected? I'm gonna write it down here. Know what does not what does get affected? It's called actually right on the right hand side because it's a liability called accounts payable. It's a liability account. So how do we increase the liability account? You're right. We credit it and we have incurred the expense because we used the gas, right? So this goes up by $200 all of these examples notice that that credits equal the debits so our expenses go up by $200 we owe somebody $200. Why does this matter? Because let's say you're trying to buy a business. You'd want to know whether accounts payable is, and that's why balance she matters because you don't want to buy a business and then understand that they having actually incurred any of these expense, they haven't put these expenses on their books yet, so that's why it's important to record all of these things as they happen. So what we're talking about here in these examples is thing called accrual accounting. Okay, and this is a really important term. Not everybody covers it, and I think it's really important. A cruel is counting is when you record expend record expenses and revenues when you incur them. So in all of these examples, when we incur the expense is when we booked it. So in these two cases, we encourage it, and that's why you see an expense account. We have not incurred it yet, so that's why we have a prepaid account. Same thing up here. We incur the revenue when we've earned it. In these cases, you see the revenue here. In this case, we haven't done anything, which is why it's a liability called aren't earned revenue. What we're doing here is called a cruel accounting. So again, accrual accounting is when you record expenses and Romney's when you incur them cash basis . Accounting is different. Cash basis, accounting. When you're recording expenses and remedies when you receive the cash or expend the cash, some companies do this most to do Not because it can be very deceiving. Um and so almost every company will do accrual accounting. If it's a public company and by public mean publicly traded on public stock, they will definitely do accrual accounting. So cash is king because I feel like they're gonna be a lot of people taking my course that own businesses. Cash is king. If you're not collecting that cash, you could go out of business very quickly. There are lots of businesses that go out of there a lot of businesses that go bankrupt not because they weren't profitable, but because they didn't actually have enough cash. So for all businesses out there, we want to delay paying for all of our expenses. You know, explain this in a second and we want to collect, get cash for Oliver accounts receivable slash revenue as soon as possible. So why is that? If there are no consequences for paying later for the utility bills, we book it on our income statement. So we have the expense and we delay paying it as soon as long as we can. That way we can have cash in our pocket for business as long as possible and that people always money. Obviously, we want that money as soon as possible. So with that being said, that's the end of this lecture.

15. Journal Entries Explained: So we're almost done with the basics of accounting. And it's been as I promise you, less than an hour. You're picking up tons of information very, very quickly, and I'm really proud of every student who's taking this course so. Section seven Handout Lecture 14. The difference between tea accounts in a journal entry So you probably hear all these accounts talking about journal entries and T counts. And what's the difference between the two should be a very short lecture because there's not much difference between them. T account is a picture representation of a journal entry. So when we work in computer systems in all the software that we use, we don't actually make tea accounts. You would never actually see T accounts in any of the accounting software or financial software. What you see are journal entries, so a T count is a pitcher representation of a journal entry. So, example, ABC company bought a tractor for $3000 make the T count and the journal entry so that two accounts or cash we bought it. So for $3000 we have equipment over here, which at this point is gonna be very easy for you. Um, that went up by $3000. So what's the journal entry? Okay, so now all we have to do is write it out. So, cash, We crediting cash, right? That's right. We did credit cash. So we're gonna right the account name here. And because we credit it, we're gonna put credit cash for 3000 and then what we're gonna do is debit equipment for $3000 you see your that I kind of indented debit over here. So it's on the left hand side, and I pushed the credit to the right hand side because it's easier graphical represent. I mean, it's easier to see it that way. And that's actually how um, financial software works as well. You'll see a left inside on the right hand side, the left hand side will always be a debit in the right hands. I will always be a credit. And that's what a journal entry is. All it is is taking the T account into writing it out. So I wanted you to know that because I think it's really, really important that you know what a journal entry is now. So now you know what a journal entry is And you've done your own journal entry at this point, Um, you been doing journal entries all along? Um, you just been using T accounts. And now you know how to convert your T count, um, to a journal entry by looking if it's a debit or credit when you make your t count and that will determine if you debit or credit, Um, your journal entry in what you write on this side, the debit or credit, and that's the end of this lecture.

BrainyMoney And Son Han, CFA,CPA, Personal Finance Made Easy!

BrainyMoney And Son Han, CFA,CPA, Personal Finance Made Easy!