Transcripts

1. Intro : Number one reason

that most businesses fail is because they

eventually run out of cash. And the most unfortunate part of that statistic

is that there are some very simple methods

and strategies that you can use to better improve

and manage your cash flow, as well as predict

where that cash flow is going to be up to 12

months in the future. In this course,

I'm going to walk you through those

strategies and methods, and I'm going to give

you the tools that you need to be able to

predict and manage and forecast your cash balance

up to one year in advance. Hello, everybody. My

name is Zach Hartley, and I am an entrepreneur and investor from Calgary

Alberta, Canada. And I'm currently running

two businesses where I apply all of the strategies and principles that I am

about to teach you. My first business is a three

D printing farm that is about to cross $1,000,000

in annual revenue, as well as a social media

business that currently generates several

hundred thousand dollar in revenue per year. Prior to that, I ran a manufacturing business

where we bought wine barrels from California and whiskey barrels

from Jack Daniels, and we converted them

into furniture and decor. And in that process, I not only had a $16,000 per week payroll

every two weeks. I also had to spend $30,000 per truck load of barrels

and $6,000 on rent. And when all three of those

expenses lined up in the same Cash flow was my

number one priority. So I have learned a

lot along the way. I have gone through the

School of Hard Knocks. I have made a lot of mistakes, and my goal in this course is to help you build a cash flow

spreadsheet that will help you manage

and predict where your bank balance is going to be at up to 12 months

in the future. And it is also going to, most importantly, relieve your

stress as an entrepreneur. It is going to help you

plan out your business, and it's going to

help you make sure that you never run out of money. I'm going to give you the strategies and the

principles that you best manage your money. I'm also going to give

you a tool that you can use to set budgets

for your business, and we are going to learn how to forecast and plan

for the future. It's going to be very exciting. And here's what you can expect. Number one, you are going

to get an inside look at the strategies that I have used to build

my businesses. I am going to actually show you my cash flow spreadsheet for my three D

printing business. I'm also going to give

real life examples of what other

companies have done, and I'm going to give you

actionable first steps to get your business started and get that cashflow spreadsheet

up and running. We're going to get

an entire template that is going to be in

the course project, and what I want you to do

is use that template and adjust and mold it to your business so that by

the end of the course, you have a 12 month template, a 12 month, basically

cash flow spreadsheet that you can use to scenario plan to manage and to predict where your bank balance is

going to be at in the future. Now, with regards to

that class submission, and that template that

I want you to fill out What would be amazing

is if you submitted a screenshot or a copy of that cash flow

spreadsheet as your project. But I can understand

if you want to keep those numbers secret and you don't want to share

them publicly. In that scenario, what

I would ask is that you share a website, a

link to your products, a link to your social media, whatever it might be

so that we can follow and like and support you

and build a community of the entrepreneurs

that have been through this course right now and that are going through

it in the future. The idea here is that I want to support you.

I want to follow you. I want to follow your business

and see how things going. So if you could share that, that would be

absolutely amazing. And if you have any

feedback for me, I would read every

single comment, I read every single review, and I would love if you could tell me that you

liked the course, you didn't like the course, or here's how I could

improve the course. It would mean the world to me, and it will help me

make this a better product as I make more

and more content. I sincerely appreciate it. Now, if you want to

follow me or learn more about my businesses

and see my content, I post a lot on

YouTube and TikTok. I also post on Instagram,

X, and LinkedIn. You can find me at

Zach Hartley online, and I look forward to

connecting with you there. But without any further ado, it's time to start talking about cash flow, so

let's dive right.

2. What is cash flow: Alright, everybody, welcome

to the first lesson. In this video, we're going

to talk about what is cash flow and why is it so

important to your business? We're going to keep

things very simple to get started. So

let's jump right in. Okay, so my definition of cash flow and what

I am referring to is the movement of money

in and out of the business. What I want to know about is how much money is

coming in this month, how much money do you have and how much money is going out this month so that

you can better forecast and manage

your business. Now, The reason that

this is important, and the reason that you

want to understand and manage your cash flow is because you could be

a profitable company, but you could still

run out of money. What I mean by that is

maybe you're running a good business

and you're making a couple thousand

dollar per month. But if you go out and you

buy a bunch of equipment or you try and buy a

bunch of upgrades or you want to

renovate your shop, That's going to cost you money, and you might run out

of money if you're not budgeting and planning

and forecasting for it. And that is where your cash flow statement comes in handy. Secondly, you need

to have cash in the bank for large

purchases and emergencies. Your cash flow statement

is going to tell you how much money

you have in the bank and is going to help

you plan out and prepare for those

purchases and emergencies. It is also going to help you

with timing and forecasting. You get better at

managing your cash flow, you're going to get better at forecasting into the future, and you'll be able to

run your business more effectively because

you'll be able to order the right

amount of inventory, or you'll be able to hire

the right number of people, or you'll be able to

basically just plan ahead and get ahead of the business instead of

trying to play catch up. So that's the whole goal here, and that's why this

is so important. How do we do this? How do we actually build a cash

flow spreadsheet? How do we actually manage this? How do we make decisions,

and how do we put this all together?

Well, it's very simple. We are going to build

an Excel spreadsheet. I'm going to walk you

through how to do this. I'm going to give

you a template. I'm going to give

you an example. Where you're going to

use my real business, and I'm going to walk you through everything

that you need to know. All you are going to have to do is enter in your business data, and then you need to analyze and adjust based on your

real operations. So I'm going to try and give you the best

structure that I can? You may need to make

some modifications and adapt it to your business. This should be a tool that

you can use to figure out exactly how much money you're going to have in the

next few months, hopefully one full year. Now, to do this, we are going to do everything

on Google Sheets. You can also do it

on Microsoft Excel. You will need a

basic understanding of how to use these

softwares, though. The only things that you need to know are to add to subtract, you need to merge some cells. You need to add some color. You might need to

include a hyperlink, and maybe you need to put

some border on some cells. It's not going to be

super complicated, and if you don't

know how to do this, you can watch a

few YouTube videos or check out a course on

any of these platforms. And it is going to walk

you through everything, but you do need to have

just these basic skills before you move forward

into this course, and before we start to really

use that Google sheet. So just as a heads up, if you don't have

that right now, I will link in the resources a couple of good YouTube videos. I will teach you everything

you need to know. It might be good to pause

this and check that out. Otherwise, let's continue here, but this is what you will need. Now, in my opinion, your cash flow spreadsheet

is going to be one of the most important tools that you use for your business. The reason is because

it's going to help you with budgeting

for your expenses. Forecasting your revenue and

almost all of your finances, if you have a banker that

is going to need to see this information for a line of credit or a loan or a financing, they're going to ask to

see this information, and if you have it ready

to go and up to date, it's going to look very,

very professional. You can also use it

for decision making and scenario planning. So if you know how much money you have in the bank

six months from now, you can figure out if you

can afford that equipment in three months time or eight months time or

whatever it might be. And so by knowing what

your bank account is going to look

like in the future, you can make better

decisions right now, and you can also plan

for different scenarios. If this supplier shuts down

or this guy goes bankrupt, or we have a huge spike

in sales over Christmas. Whatever it is, you can plan those different

scenarios and see what effect it has on

your cash flow and. So there's lots of huge, huge reasons why this

is so important, and we are going to basically

give you a tool that can help you in all of these

decision making areas. Now, in summary, for this video, your cash flow statement is a tool that is used to

plan your business, manage your money,

and make decisions. This course, I'm going to

help you build that tool. I'm going to walk

you through how to build it, how to use it, and how to make

decisions based on the information within

that spreadsheet. And so I'm very

excited about this. This is a super

important part of business that they don't

teach anywhere else. I have learned everything

in this course through the school of Hard

Knocks and experience, and I can't wait to share it

with you. So let's keep on.

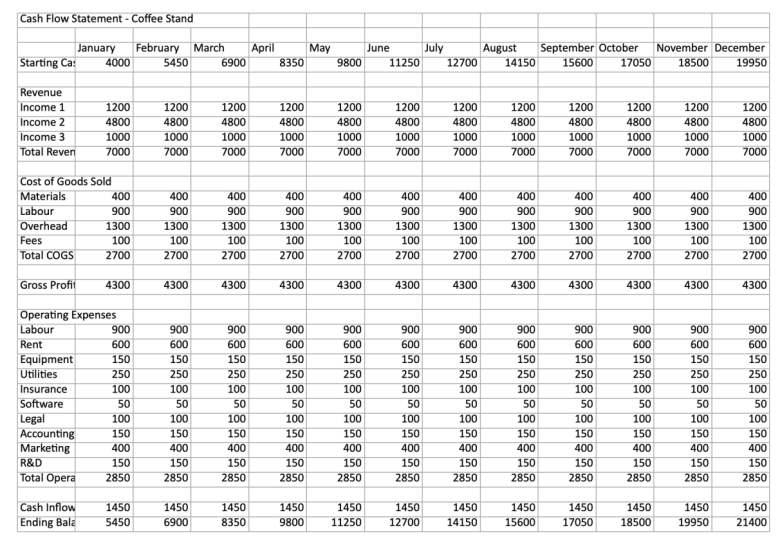

3. Cash flow structure: Alright, in this video,

we're going to talk about how these cash flow

statements are structured. How do you actually read them? How do you understand them, and how do you kind of

look at the information? So, let's jump into this. The general idea here is

that we are trying to figure out what is our

starting bank account balance, meaning how much cash

do we have in the bank, how much money's coming in, and then what do the

expenses look like, and what does our bank

account look like at the end? And so here is how

it is structured. You're usually going

to have your starting cash balance at the top, and then you're going

to have the money that is brought in that month. After that, you're

going to subtract your cost of goods sold. This is all of the expenses associated with actually

manufacturing that product, or if somebody else

is manufacturing it, it's going to be your cost to purchase it from

the manufacturer. Then you have your

operating expenses. This is going to be things

like your management salaries or your rent in the warehouse,

whatever it might be. This is everything that is

an expense to the business, but isn't directly

associated with the cost of goods sold or with the manufacturing

of the product. At the end of that,

you're going to have your cash

inflow or outflow. And this is basically your

profit or loss for the month. So it's a cash inflow at

the end of the month, if you generated profit or it's an outflow if you lost money, then at the end of it, you're going to have your

ending balance. And so your starting

balance plus your cash inflows or minus your outflows are going to

give you your ending balance. And so This is the

general structure here. It's going to show you

what you're starting with, the money that you brought

in, the money that is out, the actual plus or minus

of those transactions, and then the final impact

on your bank account. That is what we are

looking at here, and that is how this is

going to be structured. Now, when you look at

this on an Excel sheet, here is a very, very

simplified explanation. So let's say that we have

$5,000 of cash in our bank. We bring in $2,000 worth of revenue by

selling our product, spend $100 on the

cost of that product. That leaves us with a

gross profit of $100 here. And then we have $500

in operating expenses. This would be our overhead here, maybe our rent or our

management wages, whatever it might be. That gives us total

operating expenses of $500. Obviously, this would usually be multiple line items

because it would include your Wi Fi and your utilities or your

parking, whatever it might be. And then at the

end of it, we have our cash inflow or outflow. Here it is an inflow of $500, because we brought in 2000. We spent $1,000 on the product, and we spent $500 on our operating

expenses that left us with an inflow of $500 here, and our bank ending balance

is now going to be 5,500, because it's our

starting cash balance. Plus the inflow or outflow gives us the ending

bank balance. And so very, very

simplified example here, but it breaks down all of

the different aspects of the things that we

would want to know and analyze as a business owner. Now, this is just the

general structure here, and this would just be for

one month in January of 2024. And then what you

do is you basically extend this out for

the entire year, and you basically go the starting cash

balance of February. The ending cash

balance in January. And so if you notice this, these numbers will always be basically the

same the next month. So the next month's

starting cash balance will be the last

month's ending balance. And then it goes through

the exact same process of money in money out. What is the difference there? Was it a positive or a negative? Then what is your

ending bank balance? And so if you look at

this example here, we can see that

we're starting with $5,000 worth of

cash in our bank. We're putting in about $500

per month of cash inflow, and that leaves us with 5,500

at the end of month one and over $11,000 at the end

of December here in. The idea here is that now, if this was your business, you could tell me exactly how much money you were going to have in the bank in October

of 2024, for example. What's nice about that is now you know that if you need

to go out and you need to spend $3,000 on a piece of equipment that's going to

improve your operations, well, you have the

money to do that. It's not going to stress

you out later on, and you're going to be totally fine because

you're gonna have more than enough cash the bank account to manage that expense. The overall goal here is

exactly what I just said. It's to understand

what your cash balance will look like at

different times. We use this as a tool

for scenario planning. So, for instance, in my business that I

started after University, we would convert wine

and whiskey barrels into furniture and

home to core products. And the challenge

was, I was buying wine and whiskey barrels

by the truck load. That meant that I

could spend 20 to $30,000 in a single day on

a truck load of barrels. I also had about a $16,000

pay roll for my team to manufacture those barrels into finished product

and ship them out to customers and

sell that product. On top of that, I also

had rent that was coming in at about

$6,000 per month. So there could be times

where within the same week, I could have a $25,000

barrel purchase, a huge payroll bill, and a $6,000 rent payment all coming out

within the same week. And if I didn't

have enough cash in the bank account to manage

all of those purchases, Well, unfortunately, somebody

wasn't going to get paid, and you never want to have

a scenario like that, and so using my cash

flow statement, I was able to forecast

and project around those large purchases to make sure that I always

had cash in the bank, especially when those

large transactions started to line up very

close to each other. So in summary here, tracking the cash coming into

the business from revenue and going

out of the business and expenses is what

we are trying to do. And by doing that,

it allows you to get insight into where

your bank account is going to be in the future. And when you have that insight, you can make better decisions. You can scenario plan, and you can improve

your business because you have

confidence in the future. That is the goal here. That's what I'm trying

to help you with, and I hope this

structure made sense. If it doesn't make sense, just leave a message down below and I will try and

clear everything up. Thank you so much, and

I'll see you in the next.

4. Build our cash flow statement: Alright, everybody, welcome

back to another video. This one is going to be very exciting because we're

actually going to start to build our cash flow

spreadsheet in this video. And I'm going to

walk you through everything you need

to know. Let's go. To get us started

here, this is what the template is

going to look like. You can find this template in the resources section

of the course. It's going to be there. It's easy to download it. You should be able to find it in Excel or on Google Sheets. I should have two

options for you there, so you should be able to

open it on any platform. What I will say upfront is that you will need

to slightly tweak or adjust this template to match your business and your

expenses or your revenue. So this is not a static template that you have to

follow line by line. It is something that I want

you to adjust and mold so that it best

suits your business. Now, let's dive into it. Here is the actual template, and I've already filled

in month one here, but I just want to walk you

through how this works. So starting cash

balance, $5,000. This is going to be

for my pistachio ice cream imaginary business, and then I'll show you my

real cash flow spreadsheet. It's a little bit

more complicated. Here's a little sneak peek, but let's just walk through

this template first. Now, first thing here,

starting cash balance. This is going to be just

the amount of money that is in your bank

account right now, obviously, start with

whatever month you're in, but this is just going to

be your starting balance. I want you to pull a real

number for this one. But everything else

on this spreadsheet, for this example, I

want you to forecast. And if you can do this, while

you're watching this video, if you can download

the spreadsheet and do this while you're

watching the video, it'll be very, very

helpful, otherwise, do this right after this video, and then we're going to

build on it from there. So, starting cash balance, in this example, we have $5,000. Now, I run an ice cream company, and we make $1,500

in sales online. We do $5,000 in our store, and we do $1,200 from fairs and Festivals

and trade shows. So for total revenue in

the month of January, we brought in $7,700. Now, the cost of

goods sold for that $7,700 worked out to $500 in materials

hundred dollar in labor, 1,500 in overhead and $100 in fees for a total cost of

goods sold of $3,100. And so on my $7,700 in sales, that product cost me $3,100, and it left me with $4,600 leftover to cover the rest

of my business expenses. Those business expenses

included labor, rent, utilities, insurance,

software, legal, accounting, Wi Fi, marketing, research and

development, equipment, whatever it might be, here's where you put all of

your other expenses. If you need to add

line items in here, you just right click and

you go insert one row above and then put in equipment,

and you're good to go. Now you've got an equipment

line item in here. So again, adapt and mold

this to fit your business. But this is where you put all of the expenses that are not directly associated with the manufacturing

of that product. And then at the end of it, you have your total

operating expenses, and when you deduct that

from your gross profit, it leaves you with your

cash inflow or outflow. This is the total amount

of money that you either added to or subtracted

from your bank account. And at the bottom here,

if you made money, we obviously add it to your bank account

so that we can see how much money is going to be in that bank account at

the end of the month. That is the goal here and If we have $5,000 at the

beginning of the month, we hit our revenue targets and all of our

costs are accurate, and all of our expenses

are also accurate. That means that at

the end of the month, we'll have $66,500 or

$6,650 in the bank account. Now, once you've

done month one here, Basically what you want to do is you want to take

this entire rote. Well, actually, so at

the end of month one, your ending bank

balance is 6,650, and that means that at the

beginning of Month two, your beginning balance

is also 6,650. Now, once you have that, we are basically just

going to copy this over. Just like that, and then

we're going to make sure, well, this needs to be linked

here, sorry, equals that. And then we're just

going to copy this over across the entire

spreadsheet, just like that. And now you have a forecast

for the entire year. And that will tell you

exactly how much money you're going to have in

your bank account at the end of the year. Now, one thing that you do need to do is adjust

for seasonality. So for instance, if we're

selling an ice cream company, we're probably going to do

very well in the summer, and we might do $2,500 for the three or four

months in the summer. And then during the winter, we might only do $100

instead of $1,500 online. So what you need to do is

you need to go line by line, and you need to

adjust your forecast based on what you know

about your business. Ideally, you adjust

the forecast based on previous data that you

have about your business, but more than likely, you

don't have any of that data. And so you need to put

together your best guess or your best forecast based on what you know

about the industry, what you know about

yourself, and what you know about

your business. If you are not sure and

you're lost on this, and you don't know what

numbers to put on here, figure out what you did

in month one and just try and do maybe 5%

or 10% better than that each and every

month until you get to the point where that level of growth becomes a

little bit too high. Now, when you're first

getting started here, it's not going to matter

a whole lot about how accurate you are five

and six months from now. All you're trying

to do is just put a number in there so

that we can go through this exercise because

what's going to happen here is that as soon as

you're done your first month, We're going to add a column

just to the right of it, and you're going to put in

your actual numbers here, and then you're going

to compare them and see where you were higher,

where you were lower, and you're going to use

that data to readjust all of your forecasts and make

them better in the future. And so it doesn't

matter what the number is ten or 12 months from now because it is going to change, and it's going to get updated as we get more and more data. That's the entire idea here. As we're just getting started, all I want you to do is put in your best guess with regards to what your revenue

is going to be, what your cost of

goods are going to be, and what your

expenses are going to be so that you can

get a template here, and basically a model that we can start to

scenario plan around, we can start to

analyze and we can start to improve over time. So that's the goal here. That's the idea. All you're

going to do is make sure that you have an accurate

starting cash balance. You're going to make

sure that your cash inflow or outflow. Adds to your ending

bank balance. You're going to make sure that your ending bank balance from January is the starting

balance for February. You're going to go

through here, make sure these numbers look correct. Then you're just going to

basically highlight and copy the information all the way over through the

rest of the spreadsheet, just like I did, just like this. Oh, you're gonna click

this blue button. You're just going to transfer all of that information over. You're going to update

your spreadsheet and then adjust for seasonality. That's what we're

trying to do here. And by the end of it, you should have a

spreadsheet that looks roughly like this where you have a little bit of seasonality

based on your business, or maybe you run a business with absolutely

zero seasonality, so you don't really

have to adjust it. Maybe you're on a

subscription basis, so your revenue is

actually just based on number of users and

maybe your churn rate. In that case, you need to kind

of adjust your revenue to the point that you should

be consistently building, and then maybe you

lose one, two, 3% of your customers per month, something along those lines. And so need to adjust this spreadsheet based

on your business, but it should give you a starting cash balance

for every month, an ending cash balance

for every month, and it should represent what is happening within

your business during that month with regards

to the cash going into your company or

coming out of it. So once you have this

template ready to go, we are going to start

to analyze this. We're going to build

on this. We're going to scenario plan on this, and we're going to use this to improve your business.

So let's jump.

5. Analyzing our cash flow: Alright, everybody.

So now that you have a template of your cash flow

spreadsheet filled out, what we want to start doing

is building this so that we can compare what we forecasted

in our projections here. And I know it's early days. Our projections aren't great. We just started the business, and so you're kind of

pulling numbers out of thin. Air, that is totally okay. What we're going to do

here is we're going to add actual column here so that we can compare what

our forecast was to what we actually

did as a business, then we can use that data to better forecast

into the future. So let me show you

how this works. Okay, so here is our

spreadsheet, and as you can see, we've got our month

of January rate here, where we started with $5,000. We projected to do

$7,700 in revenue. We projected $3,100 in

cost of goods sold. That left us with $4,600 in

gross profit leftover as a business of which we

spent $2,950 on expenses. Then that left us with $1,650 of cash inflow into the business that we added to

our bank account, leaving us with $6,650

at the end of the month. Then in February, I should say, we started with

that same amount. We did another 7,700, and it goes on and on and on. Now, what's interesting here, and what's very

exciting about this is that we have got a

12 month forecast here. And what I want to

do is we're going to click on the

column or the yeah, the column at the top here. We're going to right

click, and we're going to insert one column

to the left here. And it's basically we're going

to move everything over, and then we're going

to go January actuals. And what I like to do here is I'm going to just correct

this a little bit. We'll open this up a little bit, and then what I like to do is I actually color the

entire column in blue. And so now we've got

January actuals. We did start with $5,000. That was a real number here. But what we can do is we

can go through and we can actually fill out what

our company actually did. So at the end of the month, on the first of the next month, or the first business

day of whatever the next month is, you

need to go through this. You need to manually

fill this out with whatever your

numbers actually are. So, let's say that we

did 14 35 in revenue. We did 5,500 in store sales, and we did $1,350 at Festivals. Our total revenue here, and all you have to do is just kind of drag this over now. Our total revenue

here was $8,285. So we actually

beat our forecast, which is really nice to see. That's always a good

sign when you bring in more revenue than

you had forecasted. Now, with regards

to our materials, because we sold a

little bit more, we actually had

$600 in materials. We only had the same

amount of labor because the guys just worked really fast and they got

everything done. Overhead didn't really

change a whole lot here, and our fees, they actually

stayed the same as well. And so our total cost of goods here, when

we moved this over, was only $100 more expensive, leaving us with a gross

profit of $5,085. Now, all of our

operating expenses, just for this example

and speed here, we will say that all

of the operating expenses were the exact same. They probably weren't the

exact same in your business. You probably have to make

some small adjustments, but they shouldn't be

changing too drastically. That will leave us with a total operating expenses

here of the exact same number. It should be 2,950, and a cash inflow that should be slightly higher

coming in at 2,135, and that gives us an ending

bank balance of 7,135. And so here is our

actuals column. We'll just highlight

this again in blue. And now we can see that we are forecasting to

finish with 6,650. We actually finished with 7,135. And when I analyze this, if these were my actual numbers as a business, here's

what I would think. I would think, Okay,

our revenue target for income source number one online revenue,

very, very accurate. We were only off by $65.

That's pretty good. Income source number two. We are off by $500, but it's a much larger number. So we're not off by a whole lot, but maybe moving forward, I think we can continue

to do 550 $500. And so I'm actually going

to use that number, and I'm going to update my forecast for the

rest of the year. Income source number three, we actually did $150 more, but I think we got

lucky because we had an extra trade

show this month. And so in this scenario, I'm not going to

adjust that number. And so now what

we're doing is we're using our actual data here to better adjust and infer our forecast from

the months ahead. And what we're going

to do is we're going to gather this data

every single month, and we're going to

compare what we actually did versus

what we forecasted. We're going to try and analyze that to adjust our forecast into the future so that our

numbers become more accurate. Now, just to show you how

I use this in real life, This is my actual spreadsheet. This is my real business and

some of the real numbers. And so I sell a lot of

product on amazon.com. I get paid twice a month, and this is all in US dollars. So I get paid amazon.com, and then my amazon.ca

payments are much smaller, but they also get paid

out in US dollars. And so in January of 2024, I was forecasting $16,200

in revenue coming in. We actually ended

up with 19,723. My employee cost me $4,000

per month, what I forecasted. In reality, he only

earned 3,040 that month. My filament cost was very

high this month, though, because we printed

a lot of product, and it came in at over $12,000. Now, with you line, that's

my supplier for boxes. I paid a lot in boxes because we shipped

out a lot of product. As you can see, I was up by about 50% on my forecast here

for shipping in January. And because of that, I actually adjusted the numbers

moving forward, and I continued to do that

to this day moving forward. Now, my total cost

of goods sold in the month of January

was forecasted at 11. It actually came in at $19,000 because mostly of

that filament cost, and then my design and

research and development, I wasn't paying any

rent back then, electricity, insurance,

Amazon monthly fees. I didn't have too many

operating expenses that gave my total operating

expenses at just under $1,500. And a net profit of under

$2,000 or a $2,000 loss. Now, this spreadsheet does not have my beginning

bank balance and my ending bank balance

because I'm actually running two or three

different businesses through the same bank account, or I run a media

business as well. So everything that you see

from me on social media, it also goes to the

same bank account. And so the beginning and ending bank balance for me

isn't necessarily as important as what my company

is actually generating for cash inflow or outflow at the

end of every single month. And just another reason

is because I keep a very, very large cash balance. So at this point in

my business career, I am almost never worried

about running out of cash, because if it ever got

anywhere close to that point, I would have a lot

of heads up and there'd be a lot of changes being made long

before that point. But for most people, when

you're just starting your business and the amount of cash you have

is a huge concern, That's when we're going to use this spreadsheet right here that shows us our

starting cash balance and our ending cash balance. Now, in the month of January, you can see that I was

projecting to make about $4,600, but we actually ended

up losing $2,000. That's because a lot

of my expenses or at least this

filament expense was a lot higher than I was

expecting it to be. However, I was able

to adjust for that, and you can see that over

the next few months, I was able to bring that

filament expense down. I was also able to

find a new supplier. And now we are far below

that expense in January. And as you can see, in

the month of February, we generated $11,000

in profit and then 2200018000210002500016000

in July. So the company is generating

some really nice cash flow, and I already have a large

balance in the bank. So I'm not worried

about my bank balance. Me personally and my business, I am more concerned about the monthly cash inflow and outflow. And like I said

at the beginning, you need to adjust

this spreadsheet to meet your needs

as a business owner. If you're in the same

situation as me, congratulations, maybe it

doesn't matter as much. If you're just getting

started out and cash is a super precious resource

for your business, then that is something that

you really need to focus on. And so, again, adjust and tweak, everything that I

am giving you to match and mold to your business, your needs, and your situation. Then as a final note, just as what you need

to do for a routine here is you need to go in at the end of

every single month, and you need to kind of update this spreadsheet and say, Okay, here's what I forecasted

for the month, here's what I actually did. Then you need to analyze

that data and say, where was I high?

Where was I low? Why was there a significant discrepancy there

if there was any? And do I need to

update my forecast for this row for the

next six to 12 months? Is there a new piece of data

that I need to factor into my forecast that could change

my revenue or my expenses? Or I'm generating a

lot of cash flow. Your business could be

generating a lot of cash flow? Maybe there's a piece of

equipment that you want to buy or something you want

to invest that money into? You can start to plug it into your cash flow

statement so that you can plan and forecast for it. So The whole goal here is to just give you basically a map and a directory of what

your cash is going to look like throughout the year and how well your

business is doing. So I hope this helps. We're going to keep

building on this. We're going to keep going, and I hope to see you there. Talk to.

6. Budgeting: Alright, everybody, it is time to officially start talking about the most exciting

topic of this entire course. And that is budgeting. Now, I know this is usually not everybody's

favorite topic, but this is the one

topic that will help keep your business organized more than

anything else. And so when it

comes to budgeting, you need to understand

that budgets are made using your

cash flow forecast. That spreadsheet that we

have been working on, that spreadsheet

that we have built. This is how you build your

budgets for marketing, your budgets for research

and development, your budgets for travel

or meals or expenses, whatever it might

be, your budget comes from this spreadsheet. So Here's the idea. Let's say that you need to spend

money on marketing? You may need to advertise online to send customers

to your business. And so in your cash

flow spread sheet, you need to set a monthly budget for your basically

marketing expenses. For us, let's just say, as an example, every month, we are going to spend $500 on advertisements to

try and send customers to our website or to

our business or to whatever it is so that

they can buy our products. Now, how do we do this? Number one, you need to define

the goals of the business. First of all, if

your goal is to sell pistachio flavored ice cream

to the people of your town, you need to have some

way to reach them. You can do that

through marketing. If your goal is to be B to B, you sell a business to business service that makes

business owners lives easier, then you probably don't

need to be advertising on the same channels as

the pistachio company. And so number one, you need to define the

goals of the business. Number two, you need to set

the priorities in order, and number three, you need

to allocate those resources. What I mean by this is if

you are a business owner, you are sold out of your three best selling

products right now, and production can't keep up and you can't make

them fast enough, you should not be devoting

any resources to marketing. You should be devoting

all of your resources, time, energy, and people

to increasing production. You need to look at

your business and figure out where

the bottleneck is, and then you need to

devote resources from your cash flow spreadsheet to try and eliminate

those bottlenecks, whether it's marketing and sales, whether it's

manufacturing, whether it's your

equipment, or your labor, whatever it might be, your job is to play chess with

the resources within your cash flow spreadsheet

so that you can generate the most profit

over the long term. And so if marketing

is not a priority because you're sold out of your three best selling products, then you need to take that $500 a month and put it

into production or to manufacturing

or to getting more efficient equipment,

whatever it might be. And so this is how you need

to kind of think about your budgets and how you

manage your resources. When it comes to an

actual example here, I have put a marketing tab on the bottom right here, it's basically

just another sheet here in the Excel template. And to give you an example of

what this could look like, let's say that you give your marketing

employee or department a $500 budget per month to spend on

online advertisements. They can break it down by these four different categories. They can measure

their total spend, and then look at their

remaining budget at the end of that month. This $500 this needs to be in your cash flow template rate here under marketing for $500. So, as you can see, it's in here already.

We're good to go. Now your marketing department

knows that they have $500 set aside for them

in the month of January. They can use it

however they want, but they cannot go over $500, or if you have some

specific requirements for how they must spend it, you can communicate

that to your team. But what happens here is you, as the business owner, you go through your cash flow

forecast, and you say, Okay, here's what my

business looks like. Here are the resources

that I have planned to allocate to these departments

and these expenses. Does this make sense? Or should I reduce

the marketing budget and increase the

equipment budget? Should I increase

the legal department because I'm worried

somebody's about to sue me? Do I need to set aside

some money because I think somebody one of my suppliers is about to go bankrupt?

Whatever it might be? You need to look at

your business and basically play chess with

the resources that you have. And then what you do

there is you adjust those budgets for your different departments on a monthly basis. And so let's say we're sold

out a product right now, I'm going to scrap my

marketing budget in February, and I'm going to

scrap it in March, and I'm going to put all of that money into

buying new equipment. And so we are going to spend $1,300 in March on a new piece of equipment that is going to speed

up our production. That's the idea here, and that's how you need to

think about your business. Your job as the business

owner is to be Judge, the Dragon, sitting in the den, the shark in the

tank, whatever it is. Your job is to be that

outside perspective looking down at your

business and saying, How can I make this better?

How can I improve this? How can I make it

more efficient? And then you need

to come in, and you need to move the pieces around to make that business as efficient as possible.

That is your job as the entrepreneur,

the founder and the CEO that is

running this business. Now, just in summary here, budgets are a tool that you use to give the

different areas and departments of your business a limit on how much

they can spend. They're also something

that you use by adding or subtracting

to that budget so that you can control the different

pieces and the resources within your business so that you can optimize for the results. Your job as the

business owner and the founder is to continually

adjust those budgets as your business grows or as your business levels

off or as your business changes so that those budgets reflect the most efficient

way to run your business. That's how you need to

think about things, and I hope this video helped, we'll see you in the next one.

7. Principle and strategies: All right, everybody, welcome

back to another video. In this one, we're going

to break down a couple of different principles

that you should be applying to how you think about

your cash flow statement. Then I'm also going to

give you a couple of strategies that you

can use to improve your overall results and make some adjustments if you ever get to a pinch,

let's jump right in. Okay, so to start us off

here with the principles, I know this sounds

kind of obvious, but the larger the

cash position that you can keep for emergencies

and downturns, the better and the safer

your company will be. If something like COVID

happens again and your business gets forced to shut down or close or adjust, You have a large cash reserve, number one, it's going to be

way less stressful for you. Number two, you're

going to be able to manage your business

much much better. And number three, you're going

to be able to stay alive when a lot of your competitors

will not be able to. Having cash in the bank

is not a terrible thing, even if you're losing

money to inflation. It can be a safety

net that keeps your business alive in the event of a downturn

or an emergency. Number two here, try to

accelerate your collections. Shorter payment terms for

your customers is better. What I mean by this is

that if you can collect money before somebody even

receives the product, that is best case scenario. If you can collect money when

they receive the product, that is second best

case scenario. But if you have to

wait 15 or 30 days or 45 days for your customer to

pay you, that is a problem, and you need to try and do as

much as you can to shorten that time period

because it's going to significantly help your

cash flow situation over Number three here,

reviewing and adjusting your cash flow forecast should be done on a monthly basis, and honestly, you should

be reviewing it on a biweekly basis in

case anything change. Your goal is to increase

revenue or decrease costs. That is the overarching goal of the business and how you're going to generate more profit, but you need to make sure

that you're going through the routine every single

month of updating your actual and your forecast

so that you can get the data that you need to not only improve that

cash flow forecast, but improve your decision

making as the business owner. Principle number four here, you need to completely

separate your personal and your

business expenses. Keeping your personal life

completely separate from your business life is not

only a legal obligation, but it is going to

make everything much, much simpler, especially if you ever bring on

business partners. Nobody wants to see that their business partner

is expensing all of these lavish dinners or

expensing their vehicle or expensing their cell phone if they're not able

to do it as well. And if you are able

to do it as well, I'm telling you right

now that you need to follow the rules of whatever

country you live in you need to make sure that you're paying the

appropriate tax, and if they catch you expensing something that is not

business related, they're going to

charge you for it. It is going to be a nightmare. You're going to raise red flags, and they are going to go through every business document that you have and looking

for other problems. And so keeping your business and your personal

finances completely separate is the best

thing that you can do. If you need to pay

for your cell phone or a vehicle or whatever it is, and it is related

to your business, yourself an allowance. Do not pay for it directly

through the business, give yourself $500 a month

as a vehicle allowance or $100 a month as a cell phone allowance and

build it as a business policy. Do not expense it directly

because it will just eliminate all of the red flags and it'll help you keep

everything separate. Principle number

five, take advantage of payment terms when available. This is kind of the opposite

of number two here. Basically, as a business owner, you want to collect cash

as much as possible, and you want to pay your

suppliers as late as possible. The idea here is that you eliminate any of these

timing issues. For instance, Let's say that you got two

large orders right away, but they weren't going

to pay you for 60 days. That means that you need

to go out and buy all of the inventory to

manufacture that product. You need to pay for

all of the labor. You need to pay for

all of the overhead. You need to pay for all of

the expenses to ship it out, and then it needs to sit in their warehouse or

on their shelves, and they're not going

to pay you for 45 days. And now, all of a sudden, you've laid out all of this

money up front, and you're not getting

paid until way later. If you can shorten

that time period, it's going to help

your cash flow and eliminate any of

those cash pinches. If you can pay your

suppliers later on, it's going to do the

exact same thing. It's going to allow

you to keep more of your money in your account, and it's going to allow

you to invest it into your business and hopefully

grow at a faster rate. That's the entire idea here. Now, when it comes to

strategy number one, these are just things

that you can do to help improve the cash

flow of your business. They are not all necessary. They are not all things

that you need to do, and if you're in a position

where you don't need to take advantage of

something like factoring, then it's probably

a good situation. But the idea here

with factoring, that you're going to

sell your invoice to a third party at a

discount for cash upfront. So let's say that Walmart comes

to you and they say, Hey, I want to buy $100,000

worth of your product, but you don't have the

money to afford all of that inventory and

overhead and upfront labor. Well, what you can do is you can sell your invoice to Walmart To a third party, and they will buy that invoice from you, but instead of

paying you $100,000, they're only going

to pay you $96,000, and they're going to go

collect $100,000 from Walmart, and they're going to make

that $4,000 difference here. That's their business model, but the advantage for

you is that you get $96,000 up front to

go and manufacture all of that product and get

it out the door and basically not being a concern or a pinch or be stressed

out about your cash flow. And so if you're ever in a position where you

have a large order, somebody's willing to

pay for your product, but they're not

going to pay you for 45 or 30 days or

whatever it might be, and you need the money up front, go through a process

called Factory. There's lots of companies

that will do this for you. There's probably

one in your area. All you need to do is

a quick Google search, and they will help you figure out what is going to be the

best situation for you. Okay, strategy number two here, and this is actually

one that I just started trying out recently. It's a company

called Plastic Pay, and they allow you to pay by credit card even when

it is not accepted. So if a supplier will not accept you paying

by credit card, this service allows you

to pay by credit card. And you get to keep number one, the points on that transaction. But you also, what's really

nice about this is you get the 30 days payment terms that you get from

your credit card, because when you make a

transaction on your credit card, you don't have to pay

it off right away. So if you need time to pay for a transaction or you want

to collect the points, you can use plastic pay to

extend those payment terms. Strategy number three here, ask your supplier for a

discount for early payment. If you have to pay a supplier for materials that go

into your product, whatever it is, ask them for

a discount on early payment. Usually, you can get two

or 3% discount if you pay for the product as soon as it ships or if you pay

for it upfront, and over time, that can

really, really add up, especially if you're

ordering on a regular basis, you now have that extra two or 3% that you would have spent on cost of goods sold

that is now going directly to your

bottom line as profit. Now, strategy number four here, if you're ever in a pinch is

that you may be able to get a cash advance from your

merchant processor. If you run an online

store and it's on shop of Shopify will be able to give you a loan based on the revenue that your

company is bringing in, and in return, they will

take a percentage of every transaction that goes through your website

in the future. So if you are doing a

lot of sales online, especially through one

specific merchant processor, they may be able to give

you financing depending on the traction and the revenue that your company

is bringing in. I've seen a lot of

people do this, and they've had a lot

of success with it. However, it is super convenient, but the interest rate

is slightly higher. The last one here is to

negotiate a payment plan, you would be surprised how

often a supplier, a vendor, or a company is willing to put together a payment

plan with you, especially if they

have any type of concern that you might

not be able to pay. And so, for instance, every single company would

rather get money from you over the next

couple of months than not get paid at all, and so if you're ever in a

position where cash is tight, be honest, tell that

supplier, say, Hey, Things are really tight

right now. I'm struggling. I need some help here.

I need some time. I need you to help me out. I'm not going to be able

to pay you this month, but I can pay a third of it each month over the

next three months. I guarantee you 99% of people are going to

say yes to that deal, if they are concerned

at all about you going under or your

business not making it, whether it's true or not. It just depends on how you kind of have

that conversation. And so make sure that if you are going to have

those conversations, make sure it's necessary, make sure you actually need it, but you would be surprised

how flexible people can be when they're concerned

about not getting paid at all. Now, strategy number six year, if you have a good

relationship with your bank, I highly recommend signing

up for a line of credit, whether you need it or not. Most banks will give you

$10,000 as a line of credit, and it will cost you absolutely nothing if you never use it. However, if you need to use it, it is way better to have it

than to need to go get it and try and get the

bank to approve you when you actually

need the money, because it is not

going to happen. Because when you need the

money, you're desperate for it, you probably don't

have a ton of money, and you don't know what to

do, and so they can sense However, when you're like, Hey, I've got lots of

cash in the bank, business is going really well, can I get a $10,000

line of credit, just as a backup

case for the future? They love those scenarios. They want to give it

to you. It's like this is a no brainer for them. And so if you are in a good financial position and

you know that your business is kind of cyclical or that

you need to buy large batches of inventory like I did for

my wine barrel business, try and go to your bank and

get a line of credit set up? It's not going to cost you

anything unless you use it. So I highly recommend it

because it can be a lifesaver in the event of an emergency

or the event of a downturn. Now, in summary here, That was a lot, and I'm like, huffing right now, but

keep a cash reserve. No matter what

happens, keep cash in the bank account and

prepare for a downturn. In case something crazy happens, make sure that you're not over

leveraged and that you've got cash that's going to keep your business running,

no matter what. Second, stay up to date

and review it monthly. You need to review your cash flow statement

every single month. You need to update

it and think about these strategies and whether or not they apply to

your situation. Like I said, keep

your personal and business finances

completely separate. I can't say that enough. It is super super

important to keep everything as clean and

separate as you possibly can. And then, like I said, again, accelerate your

collections, meaning, bring in your collections

as soon as you can. You want to collect that

money as soon as possible. And ideally, you want to pay out your suppliers

and your vendors as late as possible without straining

those relationships. That is the goal

because it allows you to keep more money in your business that

you can invest into the business to

grow that business. That's the idea

there, and that's the reasoning. And

I hope this helps. If you have any questions, leave a comment down below, and

we'll see you in the next.

8. Conclusion : All right, everybody, welcome to the last video in this course. I sincerely appreciate you

sticking with me all the way. Now, just to recap what we

learned in this course, I gave you a template for building your cash

flow spreadsheet, and I explained why this

is such a powerful tool. And it's because it

basically builds a model of your business

that you can use to forecast as well as kind of experiment with and

scenario plan with in the case that you want to

expand your business or buy a piece of equipment or

go through a large purchase, whatever it might be, this

is a tool that you can use to figure out where

your cash position is going to be at three, six, hopefully, 12

months in advance. Now, I will tell you that this is a monthly task at minimum. You need to be

going through this and updating this spreadsheet at the end of every single

month at an absolute minimum, and your forecasting should get better with time and data. Remember, you were going to

be comparing your forecast to your actual numbers

and then analyzing those numbers to figure out

why they are different. Then you need to update forecast based on

that information and what you are finding

in that process. You also need to

remember some of the principles and

strategies that I taught you from managing your business money and

managing your cash flow. You want to extend

your payments. You want to shorten

your receivables. You want to make sure

that you are collecting your cash on time and that you

always have a cash buffer. Now, if there's anything that I didn't cover in this course, or if there's anything that you absolutely loved about this, please consider

leaving a review. Read every single comment, I read every single review, and I try to improve

this course over time based on the feedback

that you guys provide. And so if you can tell me what you liked or

what you didn't like or what was missing or what you thought of

the course in general, I would sincerely,

sincerely appreciate it. And I use that

feedback to try and improve it for the next people

going through the course. Now, remember, I did put

together a class project, and I can understand that

you may not want to submit your own business cash flow for kind of protective purposes. But what I would ask

is that you please share your website

or your social media handle or something related to your company so that we can look you up and we can follow, we can subscribe, we can

like, we can comment, and we can support you and possibly even buy your product. I'm trying to build a

community of students that have gone through the course that are going

through the course, and that will go through

it in the future so that we can come together and

we can support each other, and we can offer our own encouragement

and hopefully learn from each other as well. Now, if you are interested in continuing with

this education, please consider checking

out the next course. It is all about

marketing for growth. And I'm going to

walk you through how to scale your business up. I'm going to walk you

through the differences between marketing

branding and sales. We're going to talk

about all the different marketing channels

that you can use. We're going to discuss paid

vers organic marketing and a couple of

strategies behind both. Also going to go

through AB testing, which is one of the

most powerful tools in the entire world of business. I'm going to show you

what key metrics to use to evaluate your

marketing efforts. I'm going to show

you the tools I use to make my resources, my time, my energy,

and my money, go as far as possible, and I'm also going to walk

you through how to build an e mail list that makes you money. So

definitely check that Consider following

me on social media. I post most of my videos

on YouTube and TikTok, but I'm also active

on Instagram, Twitter, X, and Linked in. I also recommend following

me here on skill share. Now, if you are building a

business that is doing well, and you are sure that you have

found product market fit, and you've got good traction, and your cash flow is looking you need some money in order to scale up and actually

build this business. Please consider

reaching out to me. I am making active

investments in small companies to help

them grow and scale. I will write you a

check that will go into the company to help

you grow the business, and I will take a small

percentage of equity in return. If that sounds like something

you are interested in, please consider

writing an e mail to info at zach artley.com, and I sincerely appreciate and look forward to

hearing from you. Now, in summary, here's

what you need to do. Number one, conservatively, manage your cash flow and build a cash flow model

that you can use to help you build a

successful business. This is a tool in your tool belt as an

entrepreneur that you use for planning and decision making and forecasting and scenario

planning, and even financing. This is going to be a

massively powerful tool in the event that

you ever need to go to the bank and get a loan or a line of credit or any

type of debt. And so I hope this video helped. I hope this series helped. This is a tremendously

powerful tool that I use in my business

almost every single day, and I hope that it helps

you with your business. If you want to see more from me, check out my other courses, and I hope to hear

from you soon. Talk to you later, and good

luck with your business.

Zac Hartley, Entrepreneur and Investor

Zac Hartley, Entrepreneur and Investor