Transcripts

1. 01 Intro to Budgeting 101 vFinal: so is helping my sister create a budget. For the first time in her life, she had never made a budget before. What she explained to me is that creating a budget could seem overwhelming, and she would rather not do it. So I sat down with her for 30 minutes and helped her trade her first budget. What I learned is that creating a budget for the first time in your life is a daunting task . This is why she asked me to create this course, to make it easy and understandable for everyone. At first I thought creating a budget was easy and everyone knew how to do it. Of course, that's not true. So what we're going to do today is create our first budget that is 90% correct in less than 20 minutes together. So before we get started, here are four key points. One. Don't focus on the past. Our budget is for the future, so that's where our focus should be. Two way. Want to round up to the nearest $10 so far Car payments. $364.76. Just round up to $370. Don't focus on pennies and sincere at penny heater or dollar. There is not going to blow our budget. Three. Don't get discouraged. Working with my sister on her budget, she got discouraged in only 15 minutes. I'm here with you, and we're going to do this together. Four. This is our first pass at the budget. We need to be 90% accurate, which is in a in school. You'll be checking your budget daily. You'll revise this budget every month and make it more and more accurate. We're just trying to get 90% of the way there right now. At the end of this 20 minute class, we want to have a solid budget. So what we do, we created a visually appealing and easy to use budget spreadsheet to make this an easy process. Just stick with us for less than 20 minutes and you'll have your first budget. So without further ado, let's jump on the Google sheet and get started

2. 02 Intro to Budgeting Spreadsheet: Hi, everyone. And welcome to budgeting 101 So we're gonna calculate your network and budget today. This is for skill. Share students on Lee. So you can see here that this spreadsheet was actually made just for skill share students. And what we're going to do is talk about how we're gonna go through this class. We don't talk about all these steps here and how to do this. So the first step is actually to make a copy of the spreadsheet. Because every student we have thousands of students on skill share used this spreadsheet. We can't have everyone editing the same spreadsheet. So the first thing you need to do is if you look here on Steppe zero is click file and then making copies. So before we do anything, let's do that. So, file, you go file right here and making copy, so it's gonna say copy of net worth and budget for skill share. Students hit. Okay. So I cannot give you read access a right access to my spreadsheet. So you have to be able to do this on your own spreadsheets. Are you gonna make a copy? So we're gonna be working with copy of net worth and budget skill share students. And now what we will talk about are the instruction. So let's do a quick overview of the spreadsheet. Okay? Instructions for skill share students on Lee. How to get started. We're gonna be watching budgeting 101 which is this class to complete the spreadsheet together. You must make a copy to do this click file and then making copies. So we just did that together. So then you're gonna read over the instructions below, and you will be well on your way to financial success. The note is on Lee at it highlighted cells and try not to alter cells that contain a formula. Okay, so let's talk about each one of the steps. Each one of the steps will be a separate video. So step zero click file and then click. Make a copy. So we already did this. We did this one time. He's got to make a copy one time. The second step is input all your assets and liabilities to calculate your net worth. Each one of these steps is a tab here below step to create expense categories and your monthly budget for those expenses, and we'll review this monthly. Step three is to create income categories and your monthly budget for those sources of income. Let me extend this a little bit here, and we're going to review this monthly, but you will most likely not have to make changes. Step four is the input your daily transactions for income and expenses. You want to do this every day. Step five is a review Your budget each month and look at the grass. Do this every day, if possible, and then Step six, which is in a larger fund here, is submit your budget as this is the class project in skill share. Still, share is based on these class projects and uploading and inspiring other students. To do that, you're gonna submit your budget. It's a one time upload to projects on skill share, and we'll show you how to print to pdf. So again, here the stick, six steps, step zeros to make a copy. We've done that, and now we're gonna focus on Step One through six on the next videos

3. 03 Step 1 of 6 Calculate Your Net Worth: So now let's calculate your net worth, which is Step number one So you can click step number one here or just go to the tab below and click Step one. Calculate assets and liabilities. Okay, so get started again, watching them budgeting one a one. And this will calculate your network based on your inputs. Okay, so now we have two different categories. Assets and liabilities. Assets are things that are worth money. Liabilities are things that we Oh, OK, so now let's go through this. We've created categories for you. And so the 1st 1 is that, say, our house. Let's say our house is worth $325,000. Our car one is worth $20,000 just do this with me. Car asset to is worth $18,000. We have $6000 in our checking account in our savings account. Let's say that we got $2500 in our 41 K Let's say that we have $18,000 in a 41 K in our emergency fund. Let's say that we have $11,000 and then investing yourself fun. Let's say we have $3000. OK, so as you know, if you watch the core for personal finance class on skill share, you know that your network is the most important financial number when we talk about personal finance. So we've written down all of our assets here. It may take you a little longer toe in, put your assets, go ahead and pause the video and put in numbers. And then we're gonna go toe liabilities. So your house loan one. Let's say that we owe $280,000 on the house, so our house is worth 325,000. But we have a loan out for 280,000. Our first car. Let's say that we have a loan off $14,000 let's say, our car loan to which it relates to car asset to we just bought this car. So let's say the cars worked 18,000 and we just took out a loan for 18,000. We have a personal loan for, Let's say, $1500 in our credit card currently has $3000 outstanding. Let's say that we have a student loan for $15,000. Um and that's it OK, so now what you can see here is, while I was doing all of this, the grass to the right were being changed as I was putting numbers in. So my total assets, I have $403,500 in assets and liabilities. I have $331,500 in liabilities. Okay, so network is actually have $72,000 that's my network. Our goal is to increase our net worth every month and increase our network every year. This gives us financial security. So that's what we want to be focused on in. Which is why I say you should look at your network each month. Hopefully each month you're paying down your house loan, you're paying down your car loans and hopefully you have more more assets every month. So your assets get bigger, your liabilities get smaller, and then your network is going up again. I know we went through this quickly, but you just take your time. You could just even stop this video. A pause it and put in the values for your house in your car for your house. You can look at Zillow dot com. For your car, you can look on Kelley Blue Book or TRUECAR. There are a lot of other websites of Determine the value of your car. Everything else you should be able to get from just your financial statements. So your house loan you should be able to get from your mortgage receipts and payments, and then your car loans the same exact thing you get out. You got a bill each month that shows you how much you have outstanding. So with that being said, that's the end of the net worth calculate.

4. 04 Create Expense Budget: So now we've completed Step one, which is calculating our network. Let's move on to Step two now, which is creating our expense categories and our budget for each category. Again, let's start at the top here. Get started. What do you spend money on each month? That's the easy question. How do you spend on the How much do you spend on these categories each month, round to the nearest $10? No need to be exact. So what's very important here is a lot of people trying around, like 99 cents here, 28 cents. There does not matter. You don't need to be that exactly. Doesn't matter how much money you make. What you need to do is round to the nearest $10. What we need to do is complete this and b 90% accurate, which means that we're getting an A and we become more and more accurate each month. So our job today is within these 20 minutes. Let's get our first budget done. So next cell here says we'll start with debt payments and then work our way through big categories. Any monthly recurring items less than $50 will be all grouped together in the miscellaneous expenses. Think about Netflix. Spotify things like that. Okay, so do not adding in categories you can rename a category that so our first expense categories. Their house payment. Let's say on our house that we pay $2600 a month. Our car payment, our 1st 1 Let's say it's $330 a month. Our car payment to $225 a month. Our personal loan. We pay $80 a month credit card payments. We pay $150 month student loan payments. Let's say that we're paying $400 a month. Food. Let's say that I spend $650 a month on food on dining out. I have a separate category for that. Let's say that I spend $125 for myself and my wife. We go out to a nice dinner every month. Let's say car insurance. I pay 100 $10 a month Jim. $30 cell phone, $50. Um, do you want a budget for gifts? That's up to you. Health and medical. That's up to you. Other home expenses. $150 then transportation slash gas, $250. Okay, I put in some other ones here some other categories, but that's up to you. And then I rounded to the nearest dollar for miscellany expense or 100 bucks from miscellany expenses. These are small things. Netflix modify, etcetera. OK, and now I'm actually done with my expense categories. That's how easy it is you put in round numbers here. Where people get stuck here is they try to put in 100 $9.38 or whatever. Don't do that. Just put in round to the nearest $10.110 dollars for car insurance, for example. Again, pause creature expense categories. You can rename them. And then in the monthly budget round to the year's $10 you can see everything here is rounded. Okay, we're not putting any exact numbers in because we don't want to slow ourselves out. So we are now complete with Step two, which is creating expense categories. We pull it calculated our net worth, and now we created and budgeted for expenses

5. 05 Create Income Budget: Now you've created your expense categories and created a monthly budget force. Have you completed Step two? Let's move on to step three. It's gonna look very similar to your expenses, but we know that you don't have as many income categories. How do I get money in? So let's start with cell six. Where do you get your money from each month, we'll start with your paycheck, which is likely your largest source of income and use your net paycheck. We get this question a lot. Use your net pay check after taxes because obviously, you don't get to take home any money after you pay the taxes. So don't include that as money that you earn. You only earn what you take home. The government takes part of your money. Then you can't use that right. So again, after taxes, your net paychecks or what do you actually get deposited into your bank account each month ? So let's say my income categories or my main job. My monthly budget is I get $12,000 a month from my main job. Um, my side hustle one. Let's say I make $800 a month for my side hustle. I'm not gonna budget for any bonuses, interest and dividend income. Let's say that's $250 then random other income, let's say $150. That's it. That's how easy it is to create your budget for your income categories. Because most people don't have 19 jobs, they have one main job. And if you watch our core for personal finance, you have at least one side hustle. Okay, maybe, too, but at least one side hustle, so you have maybe two sources of income. If you're married, you could easily change one of these two custom category to pay check main job to which is wife, and then put in a number here. Let's say it's 3000 or let's put in a larger number. Let's say it's $10,000 my wife makes $10,000 a month and I make $12,000 a month or vice versa. Doesn't matter. Um, and now you have all your income categories with each monthly budget. As you can see, this bread she that we created is to not overwhelm you, keep things simple, get 90% of the way they're making a on your first budget, then you can come back and make it better next time. But again, our job is to get this done.

6. 06 Input Actual Transactions: So now we've completed Step three. Let's move on to step four. So in your mind you've now created your net worth calculation. You created your budget for expenses, your budget for income categories. OK, budget for expenses here, your budget for income. And now we're gonna put an actual transaction so you can see Step four is called Input the actual transactions. So let's go through our expenses. And let's say, um, we're gonna put in the dates here. So 11 2020 the amount of our house. Let's say that our monthly payment was $2600 for a house, 1 to 2020 or a car payment was $330. One. 3 2020 Our second car payment was $280 and then groceries for the month of January. Let's say that I bought him on the first of January 2020. I spent $600 on groceries, and then let's keep adding mawr categories or more transactions to 1 2020 Let's say I'm I just deleted the one blow it. Let's say that 2120 20. I make another house payment, but I put in $2800 in my house and extra some extra money from point. A bigger house payment in OK, so now let's look at my income. And there's a reason why I did this for February. Okay, let's say now for my income, I put in 11 2020. I got paid. I got $5500 from my main job. Let's check how much themselves to make every month, and they're supposed to make 12,000 net. So actually, it's put in 6000 here and then on 1 15 2020 my second paycheck of the month. I get another 6000. Then let's put in my wife's income. 11 2020 $5000 1 15 2020 Another $5000. Okay, and the description is paycheck, paycheck, paycheck here. Pay check here and then Now you select the categories. OK. Selecting the categories for expenses and for your income are really important here. Okay, these are already selected 40 but you can see if you drop it down. You'll have all of these selections from what categories it is. So house payment. One carpet mint, one car payment to Let's elect food and then house payment. Okay. And let's actually add one more transaction for going out to dinner. So we had one nice dinner in January. Um, let's call it dinner, and then we can select the category as dining out. Okay? Just so you can see the in transactions in there. So all here's my income. And let's say that we did a side hustle on the 31st of January 2020. But we only made $245. Okay, we'll call this side hustle, and then we'll got to select the category for side hustle. And this one is gonna be paycheck main job to because this is my wife, remember? And then paycheck, main Job two, which is my wife. We can actually extend this so we can see it. So now we put in all our income for the month and for expenses. We put in all of our expenses for the month of January. So now what we can see here is that we are complete. Would step four. That's how easy it is.

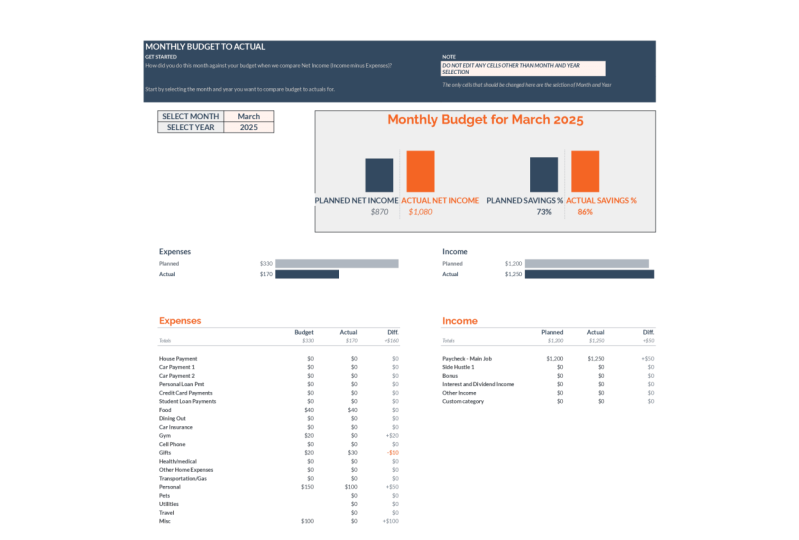

7. 07 You're Done! Step 5 and 6: So we've completed Step four. Let's recap what we've done. So in step one be calculated our net worth. Step two. We created our budget categories for expenses and the amounts from our monthly budget for expenses. Step three, we created the income. We created our monthly budget for income categories. Step four, we put in actual transactions. Okay, so this is the actual versus budget we put in actual transactions for the month of January 2020. Step five. Pretty easy. Step five is all you do is click down into a monthly one of you that say it's January 2020 . And then now we created this beautiful graph, which is a class project that we're gonna print out and upload for January 2020 So you can see the monthly budget for January 2020. And how do you get started? This is how did you do this month against your budget? When we compare net income, which is income minus expenses, so start by selecting the month and year. You want to compare the budget to actual for so January 2020 you can see a monthly to budget toe actuals. We had a plan net income of 17,950 we had an actual net income of $18,310. But why was that? We had a plan savings rate of 77% actual savings rate of 82%. So we saved more than we thought we could. But why was that? Look at our expenses. We plan for $5250 expenses, but we actually only had $3935 of expenses. Are income was also a little bit lower. Are planned income with $23,200 are actual income was $22,245. So here, if you scroll down, you can see how this is beautifully designed on the expenses in the income, and you can see what your budget was and your actual and where things were different. Right? So we said here that we were going to spend $2600 in the house. We did car payment one. We spend 330 but car payment to We decided to pay some extra toward towards that principal balance, which was $280 instead of 2 25 That's great. We're trying to get rid of our debt, right? And then So that's $55 extra. We didn't make any personal loan payments, credit card payments. We didn't make any student loan payments. We didn't make any. Okay, that's not actually true. We just haven't put in the transactions yet. So if we were to put in the transactions while that's going to change and you can go on to see so on and so forth how each one of these categories did same thing with income, you can see here that my main paycheck for my main job I made 12,000. I plan to make 12,000. The difference comes up in this side household one. I was gonna make $800 but because it's a side also, I only made $245 which meant that I came in $555 under budget. I didn't make enough money, right? And so that's where you can see my actual income is short of my planned income because of my side hustle, other income and interest and dividend income. Other than that, everything met their budget. So this summary. Here is the end of step five. You just got to review this and add. You put in more transactions. You could just change the month and change the year and look at the summary for that month . And that's it for step five. So because the step was so easy when actually advice and do steps six. At the same time, we'll go to file print. Yes, we want to print this all out, right, And what we can do is fit it toe one page, make it clean, make it easy to look for and then hit. Next. We're gonna print this to pdf as a class project hit print, weaken. Save it wherever we need to all just a bit to the desktop hit save and that's it. And we'll upload that. Pdf as a class project, and I'll actually upload this. Pdf in there. And as you can see, the adobe, Pdf has now saved it. So that's it. In less than 20 minutes, you created your monthly budget and calculated your network. You're so far ahead of other Americans. Congratulations on finishing this class in watching their class on skill share

BrainyMoney And Son Han, CFA,CPA, Personal Finance Made Easy!

BrainyMoney And Son Han, CFA,CPA, Personal Finance Made Easy!