Transcripts

1. Intro: Hello everyone. My name is Zach hardly

and welcome to my course on dividend investing

for early retirement. In this course, we're going

to focus on four main topics, starting with what is a dividend and how do they

work that we're going to take a look at how

to buy and sell dividend stocks that

we're going to start evaluating different companies

to make sure that we're actually buying and

selling the right stocks. And we're going to

finish it off by calculating exactly

how much money you need in retirement

in order to live off dividends for

the rest of your life. And if you're

interested in myself, my name is Zachary Lee. I currently manage my

own personal portfolio of about $300 thousand, and I have a YouTube

channel with about 42 thousand

subscribers where I share all of my content and what I'm trading and

what I'm investing in. If you want to see any of that information on

a day-to-day basis, definitely consider subscribing

to the YouTube channel. But for this course, it's very, very exciting. This is actually my fifth

course here on Skillshare. Already taught over

13 thousand students on this platform alone. So I am very excited to launch this new dividend

investing course and share with you a couple of tricks and a little bit of

knowledge that I've gathered over the last few

years that I am using in my own personal

life to put towards my retirement is I want

to share that strategy with you today and if you get any value out of this course, the only thing that I ask is please leave a review for

how I can improve it in the future or what

you liked best and without any further ado,

let's jump right in.

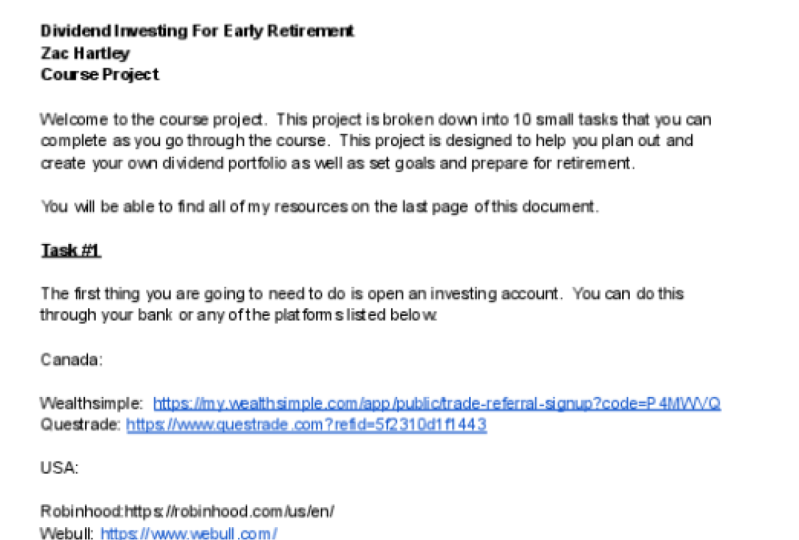

2. Course Project: All right, everybody. So before we get started

in less than one, I just want to introduce you

to our course project here, this is a very simple

PDF that has 10 tasks on it that are

designed to make sure you're understanding

all of the concepts, as well as setting

goals and starting to build your own

dividend portfolio. So everything you need is

going to be in this document. I've also included all

of my resources in the sample portfolios

that we're going to use as examples

throughout this course. Everything is included

in this document and all of those resources

are on the last page. So if you have a

printing nearby, I highly recommend printing

this off and going through it as you go through the course or keep it open

on your computer. You'll also be able to click

all of the links from there. So I highly recommend it. And without any further ado, let's dive into lesson one.

3. What is a Dividend: All right, everybody,

Welcome to Lesson 1. In this lesson, we're going to talk about what is a dividend. So to answer this

question, very simply, a dividend is when a

company gives money back to the people

that own the stock. And so this is quite

literally the company taking an amount of cash and

giving it back to the people that own

stock in that company. And so if you own stock, when the company pays dividends, quite literally have an

amount of money deposited into your account that you can use to pay for your expenses, go into retirement by other investments with you can do anything you want with it. And when that company

gives you that money, it's kinda like no

strings attached, then basically

paying you back and thanking you for investing

in their company. Now, what is a stock and

how do you buy the stock? Very simply, stock represents

ownership in a company. And so when you go out

and you buy stock, that literally means

that you are now becoming an owner in

that company because that stock represents a portion of ownership in that company. So for instance, if

we have Company XYZ, so that'll just be the name of the company for this example, Company XYZ has 100 shares and you own 400 of those shares. So that means that

there's a 1000 shares and the total pie and you

own 400 of those shares, that means that you own 40% of the company and that's how

your stock is broken up. You could also call that equity, you could also call that shares. You would call that a

percentage of the company. There's a variety of

different terms for it, but it basically means

that you own for 100 shares or 40 percent

of the outstanding shares, or the total shares that represent the ownership

in that company, where you own a higher

percentage of the company, you will receive a higher

percentage of the dividends. And so for instance,

company decides to pay $100 in dividends and you

own 40% of the company, you would receive

$40 in dividends. And that is why dividends are so attractive because they usually represent a steady source of income that anybody

can generate, anybody can establish for themselves without

having to do much work. In the meantime,

all you have to do is own the shares

and buy the stock. And it's very simple to do because in the rest

of this course, I'm going to walk you through everything you need to know. Now, in the next lesson, we're gonna talk

about how to tell if a company actually

pays a dividend. So I hope to see you there. We'll see you soon.

4. How to tell if a company pays a Dividend: All right, You guys,

welcome to lesson 2. Thank you so much for sticking

with me in this lesson, we're going to start

to talk about how to tell if a company

pays a dividend. So by the end of this video, you should be able to look at

your favorite companies and understand whether or not owning them will

get you a dividend. Let's dive right in. Okay, so to start us off here, let's just talk a

little bit more about dividends because

there's a couple of things you need to know. First of all, not all

companies pay dividends. That's really important to know. Some companies decide

to pay dividends, some companies decide

not to pay dividends. We're going to talk

about the reasoning behind that in just one minute. Let's move on for 1 second

here because dividends are paid out of the profits

that a company generates. So that can shorten the

list of companies that pay dividends because

some companies are not profitable in

the early days, a lot of growth companies

and startup companies operate at a loss for a few years until they

become profitable. And so not all companies

are profitable and most dividends are

usually paid out of profits. If a company is paying out a dividend and they're

not making money, that's a very bad sign and it's something that

we want to avoid. And lastly here, paying

out dividends means that the company is not investing

that money back into growth. So when a company

generates profit, they have two things that

they can do with that profit. They can either

decide to invest it back into the company and create a new warehouse or add a new shipping line or

create new products, or put it into research

and development. And they can basically invest

it back into the company. Or they can take some of that profit and they can give

it back to shareholders. And that's how they

reward shareholders. And then shareholders can do whatever they want

with that money. And that transition

from the company to the shareholders is

called the dividend. And so when a company

issues a dividend, that means that they are

giving up the ability to invest that money

back into the company. And it needs that they

might grow a little bit slower compared to if they had invested that money

into the company. So it's something to

keep in mind here because It's kind of like

an opportunity cost. If you have a $1000, you can give it back

to shareholders, but it means that you cannot

invest it into yourself. Or you can invest

it into yourself. But it means you

cannot give it back to shareholders or you meet

somewhere in the middle, which is where most

dividend-paying companies meet. They pay out a portion

to shareholders and they put a portion of

it back into the company. Now, there's also

some companies that are profitable but

don't pay a dividend. And those companies

are usually what we call a growth

stock and a growth stock invest all of their profits back into

growing the company. And so this is a company that let's call it

Uber, for instance, oversees a massive opportunity to expand worldwide right now. And so all of the

money that Uber generates and all of the

money that Uber makes, their putting it back

into the company to grow and try and basically

take over the world. They don't want to

give that money back to shareholders right now because they can

use that money for growth and they

know that they have some competitors out there. And so there are some companies that people by thinking

that the price is gonna go up over the

long-term and somebody else is going to buy it from

them at a higher price. Other companies are more

focused on dividends. Other companies really

pride themselves on having a steady Dividend and

making sure that they're giving cash back to investors

pretty consistently. And so we have gross stocks on one side and we have dividend

stocks on the other side. And dividend stocks

find a balance between paying back shareholders

and growing the company. And basically, you can decide this of whether

or not a company pays a dividend if they paid dividend than they

are a dividend stock. If they don't pay a dividend, they're probably a growth

stock because they're keeping all of that money and putting

it back into the company. And so that's how I like to

look at companies in general. If they paid dividends, dividends stock, if they don't pay a dividend,

growth stock. Now there are some fine lines

to that, but in general, growth stocks are usually

technology stocks, drone stalks,

biotech, e-commerce, space, cannabis, any of

these growing industries, any of these newer industries, any of these kind of exciting

technology industry's, most of these companies are

going to be growth stocks. Now when it comes to

dividends stocks, these are going to

be companies with usually a more steady

business model and steady revenue stream. Things like utility companies or energy companies or mining

and resource companies, maybe even industrial or

construction companies, and a lot of times

even retail companies. If you look at a company like

maybe Procter and Gamble, where they have a variety

of different products in a variety of different niches and a variety of

different stores. And they have a fairly

steady business model. They can pay a fairly

steady Dividend. And so these kind of steady business model companies are usually the ones

that pay a dividend. Whereas these sort of e-commerce and space

and cannabis companies are usually considered

to be gross stocks. And so definitely something

to keep in mind here. Now, there are certain companies that kinda cross this boundary. So for instance,

I mentioned that a lot of technology

companies or gross stocks, but Apple and Microsoft

both paid dividends. They pay a dividend because

they have grown so fast and they make so much

money and they have so much cash on

their balance sheet, meaning that they

have so much cash that they have access to, that they might

as well give some of it back to shareholders. So yes, there are technology

stocks that pay dividends. Microsoft and Apple in general would be

considered growth stocks. However, they do pay dividends. So that line does blur

in different situations. Definitely something

to keep in mind. But in general, growth stocks are usually those

kind of technology, e-commerce space,

biotech stocks, dividends, stocks usually having more steady business model. Now, how to tell if a company pays a dividend? It's

very, very simple. You can just look

up that company and almost anywhere

you look it up, they will give you a couple of statistics about that company. And the one that we're

looking for right here is anything to

do with dividends. And so you can see right here, I looked up Shopify

incorporated. This is the e-commerce

website platform. And when you look at

the dividend yield or the ex-dividend date is just terms that refer

to their dividend. Everything is filled

in with NA or not applicable in

this means that Shopify does not pay

a dividend if you go to a different company

like caterpillar, which is an industrial

construction company in the United States. You can see that this

data is filled in here. You can see that they pay a $4.44 dividend and the

ex-dividend date is January 19th. And so you can see that

caterpillar does pay a dividend. Now if you look this

up on your phone, this is what the screenshot looked like for me

when I just went to the stock app on

my Apple iPhone. And you can see right here

that the dividend yield 2.15%. And so basically what

you're looking for is any information

about the dividend when you look up the company, if there is no information

or just says N A, that means that the company

does not issue a dividend. You do not get paid a dividend

for owning those shares. And so this is the way that

you can figure it out. You can find this information on almost any platform

that you look up. I've just gone to Yahoo

Finance and the stock apple, my cell phone because I find that those are the most popular. Now one question

that gets brought up a lot when I talk

about this topic is who decides on whether or not the company

issues a dividend? Like what makes the difference between issuing a dividend

and not issuing a dividend? And the truth of the matter is that decision is left up to something called the

board of directors. And the board of directors is a group of people that

are basically there to oversee the company

and choose the CEO of their role is to make sure that that company is being

governed and run properly. And if it is not,

it is their job to step in and replace the CEO. And they also decide

what happens with regards to the cashflow and the profit that comes

from the company. And therefore, if they

decide to issue a dividend, that money comes out

of the profit and it gets issued back

to shareholders. If the board of directors

would rather keep that money in the company

and use it for growth. They'll give that

directive to the CEO. And the CEO will go

into the company and execute it based on what the board of directors

has asked for. And that's how a large corporation

is usually structured. That's how most

corporations work, and that's how dividends

are decided upon. Now I know that there was a ton of information in this video. Feel free to rewatch it. Please make sure you are

taking notes because I know there's a lot that

we're going through right now. I'm trying to keep it

as simple as possible, but in the next video, we're going to start looking

at dividend yields so that we can start

to understand how different companies compare with regards to the amount of

money that they're paying out in a dividend so that you can get the most bang for

your buck and the highest ROI and make the most money from your

dividends. Here we go.

5. Dividend Yield: All right, You guys,

welcome back to lesson 3. In this lesson, we're

going to start to talk about the dividend yield. Now the dividend yield

is very, very simple. The dividend yield shows us

how much money we will get back from our investment

in the form of dividends. It's a really useful

tool for comparing different companies because

if we look at two companies, company a and company B, and one company, company B

has a higher dividend yield. That means we're going

to get more money back from investing

in this company. And that could influence

our decision or be a reason to invest in

company B over Company a. And so that's what we use the dividend yield for and

it's very simple to calculate. All you do is you take the

annual dividend yield. So the total amount of dividends that would

accompany is going to pay on an annual basis and you divide

it by the price per share. So let's look at

an example here. If we look at Caterpillar stock, the price per share is

$202.79 and this stock, Caterpillar stock pays an

annual dividend of $4.44. So if we divide $4.44

divided by $202.79, that gives us 0 to one. Now if we turn that

into a percentage, that gives us 2.1%, and that means that the dividend yield for

Caterpillar stock is 2.1%. And if you go back to

Yahoo Finance here, here's a quick

screenshot and you can see the price is $202.79, $4.44 in a annual dividend, and that equates to a

2.15% dividend yield. And so for every $100 that we invest into

Caterpillar stock, we are going to get $2.15 back

in the form of dividends. Now if we look at

another example here, this is John Deere, the popular tractor

company ticker symbol is D0 and it currently

trades at $348.78. That company has an

annual dividend of $4.20 and that gives them a

dividend yield of a $1.21. So for every $100 that we

invest into Deere and Company, where you're gonna

get a $1.21 back. And so if we were comparing

john Deere to caterpillar, caterpillar has a higher

dividend yield and as long as they are

both good companies that operate in the same way, caterpillar is going to be a better investment

for me because it's going to give me more money back in the form of dividends, which is exactly what we're

looking for in this course. And so here's an

example of how you can use that dividend yield to

find a better investment. Now, another example

here is AT and T, US Telecom company that provides cell phone coverage

and they have an exorbitantly high

dividend yield. So for instance, the price

per share is $23.68. They pay $2.08 dividend, and that means that their

dividend yield is 8.77%. So for every $100

invested into AT and T, you're actually gonna

get back $8.77, which is absolutely amazing. And it's even much higher than caterpillar and John Deere. And so if you're

looking just for dividends AT and T could be one of the options

that you consider above John Deere or

above caterpillar. Now, there's a variety of

other factors that you need to consider before

you make that decision. We're going to talk about all of those in the rest

of this course. But just in summary here, the dividend yield helps us to understand how much

money we should expect to generate from the investment in the

form of dividends. So for every $100 at

$1000 that you invest, the dividend yield will help tell you how much money

you can expect to get back from that investment

in the form of dividends. And we use the dividend yield to compare companies and understand which company is going to pay us back more money in the

form of dividends. And so it's very, very

helpful as investors. And now just to give you a

real-life example of this, here is my personal goal

when it comes to dividends. So for me, I live in

Calgary, Alberta, Canada. And if I can accumulate

a portfolio or in a massive money

that is $3 million, I can then invest that money into

dividend-paying companies. And if I can generate a 4% dividend yield

across those investments, that will pay me a $120

thousand per year before taxes and $97 thousand per year after-tax

is where I live. That means with a $3

million investment, I can generate $97 thousand of after-tax income for

the rest of my life. And over time it would

probably even increase. And so that is my goal. That is my target is to get to $3 million invested

into dividends, live off of that

dividend income for the rest of my life

because I could very, very easily live off in

$97 thousand per year. Absolutely no problem. So those are my goals. Now in the next

lesson, what I want to talk about are the dates associated with

dividends because there's a couple of different

dates that are super, super important with

regards to when you get paid from

those dividends. So I want to make

sure that you're well aware of the timelines and I'm going to walk you

through everything you need to know in the next lesson.

6. Dividend Dates: All right guys, congratulations, you have made it to lesson 4. In this lesson, what I

want to talk about are the dates that are

associated with dividends. There's a very specific timeline that happens when a

dividend is issued. And so in this video, I want to walk you through

that timeline so that you can better

understand it and make sure that you're not

surprised when money either does or doesn't show up

in your bank account. Okay. So when it comes to

dividend dates there for dates that are important

when it comes to dividends. And we're just gonna go through it in chronological order. So the first important date here is called the

declaration date. And we're going to use

caterpillar again as an example, just because I think they're a great dividend company and they're fairly

simple to understand that they build construction

equipment and bulldozers and pretty much stuff that you see at the construction site

on the side of the road. So everybody's familiar with their products and they're

very simple to understand. And so here is an announcement that the company put

out on December 8th, 2021 Were they have basically announced that they're going to issue a dividend. And so if you've read this, it says caterpillar ink

maintains dividend. And so the board of directors that I described

to you earlier of Caterpillar ink voted

today to maintain the quarterly dividend of $1.11 per share of common stock. And so if you own common stock, the board of directors has just announced

that they're going to issue a dividend

of $1.11 per share. Now, this announcement

goes on to say that this

dividend is payable February 18th of 2022

to shareholders of record at the close of business

on January 20th, 2020, 2. And these are the other dates that start to get

really important here. So this is the first one

that's super important. And basically they've

announced that it is payable on February 18th. So remember, they announce

this on December 8th, but it is not going to be

payable until February 18th. So two months from

the day that they announced it is when you're actually going to

receive that dividend. So just because IT company

announces dividend, doesn't mean that money is going to be in your account tomorrow, something to keep in mind there. They also said that it's going to be payable

to shareholders of record on January

20th, 2020, 20. And we're gonna talk about

that right now because the record date is

the second really, really important date that

you need to be aware of. And basically the record date is the date where the company acknowledges who owns the shares and creates a list for payments. This date is set by the company. You can see it was actually put in that press announcement, and in that announcement

in our example, it was January 20th of 2022. And so if you own

shares On this day, not at the beginning of day, you have to own them

for the full day. So you actually got to

buy and before that. But if you own shares

on January 20th, you will receive a dividend even if you sell

them the next day. So if you sell on January 21st, but you own them for the

full day of January 20th, you will receive that dividend. Now, the next date that

is super important here is called the

ex-dividend date. And basically what the

ex-dividend date is therefore, is it can take one to two

days for a trade to settle. So depending on what type

of account you have, depending on what type

of trade or you are and how much money

you are trading with. When you go in and

buy and sell a stock, it could take up

to one to two days for that trait to settle and for that trade to actually go

from one account to the other or that security to go from one account

to the other. And so because of

this time delay, we have something known

as the ex-dividend date. And so this ex-dividend date

is set by the exchange. It is not set by

the company itself, it is set by the exchange

that manages the shares. So the New York

Stock Exchange or the nasdaq or the

Toronto Stock Exchange, all have different

ex-dividend periods which are dictated by

that individual exchange. And that is because it can take up to two days for

certain traits to settle. And so because of that, they have the ex-dividend date. And it's basically

the date where you must own the shares before this date in order to qualify for the record date so that

the shares can settle. So for instance, if

the record date is the 28th of January and the exchange has a

two-day ex-dividend date. That means that you need to

own those shares on the 18th. You need to own them two

days before the record date. And so this is very,

very important. And it means that

you can't just buy the share the day

before the record date. You actually have to buy

them a certain period of time before that record date. And that period of

time is known as the ex-dividend period

or the ex-dividend date. Now, the last date that's

super important here is the one that we're all excited about and the one that

really matters here, and this is the payment date

and this is the day that the money is actually

transferred into your account. And so depending on

your account and how you have a setup

most of the time, it will literally just be an increase to

your cash balance. So money will come

into your account and if you hold any cash, it will just increase

that cash balance. Now, in our example, this was February

18th of 2020 2. And so on that date you would

see that money come into your account and this happens

completely automatically. You don't need to do

absolutely anything for this, and it will just

automatically take place in the morning

or usually buy lunch. That money will be in

your account and then you can do whatever

you want with it. Now, in summary, here, I just want to go over the

four days real quickly again. So the declaration

date is basically the announcement of a dividend

by the board of directors. This is controlled by the

company and they can come out whenever they want and

announce a dividend. Usually it happens on

a quarterly basis. The ex-dividend date

is the date that you must own the stock

before this date beat. This is set by the exchange, and this is basically

the period of time that it takes

for your traits to settle so that that list can be built for the record date. The record date is usually

one to two days after the ex-dividend date

and you have to hold the stock on this day for the entire day in order

to make it on that list, you can sell it the next day. Absolutely no problem. And you will still receive the payment on the payment date, and this is the day that

you receive that dividend. Now, there's a little

bit of reasoning for this number 1 is

that this system prevents people from

buying the dividend on the date of record and

selling it right afterwards. So not only does it help

account for that time delay, but it also means

that you can't just buy the stock the day before it's about to record a dividend and then

sell it the day after, you actually have to hold

it for a period of time. And in most situations,

in most scenarios, that record date of when that

basically listing is made, the stock will

actually drop just slightly because that

cash will actually be accounted for

at that point and that money will no

longer be the company's, it will be the shareholders. And therefore, the stock usually takes a very small

hit on that day. And so something to

be very wary of, you're not going to be

able to just buy and sell these shares before

and after the record date. That's not a strategy

that I would recommend. It's not a strategy that's worked very well

for many people. And there are

protocols and there are rules in place

to prevent that. So I don't recommend it. And I really recommend long-term investing

buying companies that you believe in and focusing on

good dividend companies. I'm going to help you find

in the rest of this course. Now, in the next video

we're going to talk about how to actually buy

these dividends stocks. We're going to go through one of the platforms that I use. I'm going to show

you exactly how to buy into these companies, as well as exit these companies in case you change your mind. So stay tuned and let's go.

7. How to Buy and Sell: All right, everybody,

welcome to lesson five. In this lesson I'm going to

walk you through exactly how to actually buy and

sell different stocks. And I'm going to do it

right in front of you so that you can see everything

you need to know. Let's go. Okay, so the first

thing that you need in order to buy and sell stocks is you need to open up in an investment account

if you live in Canada, I knew just getting started, I highly recommend well simple. If you live in Canada and you're already pretty

familiar with trading, then I would go with

Quest straight. It has a little

bit more features and control over your investing. But well, simple is by far the more simpler

and cost-efficient way to get started if you're new to trading and trading

with a smaller amount. And if you live in the USA, I would recommend weevil. That's probably the best

online platform for you. And if you live in Europe, I would go with equatorial. Now these are just

my recommendations and the platforms that

I think are good. I personally have most of

my money on Quest trade. But in this example,

we are going to use, well simple because it is the best platform for beginners. It's also the simplest

to understand and you will be able to correlate

what I am doing on well, simple with whatever platform

you are using at home, because it is so simple. So that's where we're

gonna get started. And in this video

we're going to buy shares of AT&T and

then we're going to sell shares of AT and T so that you can see

exactly how it works. So all I'm gonna

do here is go to my basically well Simple.com account here I have $1800 in this account and we only

have one position in it. I've got Amazon

CDRs right now and we have $57 of money leftover. And so what we're gonna do

is we're going to spend that $50 on AT and T. And so all I'm gonna do is start to type in or out here in the search bar and then find the companies

that I'm looking for. So AT and T cos $26.13 USD. And if we scroll down here, we can see some information

about the company. So the market cap here is what the entire company is worth. And at the bottom here, you can see that AT and

T has a yield of 7.94%, which is very, very nice,

very, very attractive. And that is a great

dividend yield. So what we're gonna do is we're going to

scroll back up here. And on the right-hand side, you can see this little window here where it says Place Order. And so what we're gonna do

is we're going to choose our account and

I'm going to leave it in my personal account. You can see we have $44 USD

available in this account. And then right underneath that you can see the order type here, and this is super-important. So you have two options. When you click on order type, you have the market by and

then you have a limit buy. And basically what happens here, when you place a market buy, you will go into the market and you will buy those shares at whatever the next person is willing to sell those shares at. So if the last transaction

was twenty-six dollars, but the next person is not

willing to sell those shares except for at $27 and you

place a market order, that may mean that you will go up to 27 dollars to

buy those shares, will then drive the market

price of those shares up. And so if you place

a market order, your order may

execute at something slightly different than where

the price is currently at. That is the risk

of a market order. But the benefit of a market

order is that it will execute absolutely right

away as early as possible. And so if you just want to get into it right

away and you're not worried about a one

to 2% slide and the price than a market

order is perfect for you. However, if you

are worried about the price moving once

you've placed that order, that's when you're going

to use a limit order. So a limit order

will basically set the maximum dollar amount that you are willing

to buy shares at. So for instance, if

the current price is $26 and you want to

buy a 100 shares, but there's only 50

shares available at 2650. And then the next

50 shares are at $28 and you place a limit order. It will only buy

the shares that are priced underneath

of your limits. So if your limit was

twenty-seven dollars, you will pick up

the 50 shares here, but you'll miss out on

the 50 shares at $28. And so a limit order caps the maximum amount that you will pay on a per-share basis. So for us right now, AT and T is trading at $26.17, the maximum price that I'm

willing to pay for it as $26.20 and I just want

to buy one share. And so my maximum

estimated cost is $26.20. Click on Buy, and

this is going to show me how the

limit orders work. I'm going to click on Continue. I'm going to confirm my order and then order sent

limit by of one share, and there we go, $26.20. Now let's see if

that order filled. We can go back to

my portfolio here. And when we click

on my portfolio, you can see we have

two positions there. And when we scroll

down, Oh, welcome back. It's asking me for my

password, that's weird. And when we go to

my portfolio here, you can see that we now

have two positions. We have the Amazon shares

that we held before, but we now also have

one share of 880. And so this is

really, really nice. That's how you buy the shares. And you can do it with either a market order L, a limit order, a limit order will cap the maximum price that

you pay for those shares, whereas a market order

will try and fill that order as

quickly as possible. And if it means that

it has to go up in price in order

to fill that order. That's what it will do when

you place a market order. So now we own shares

of AT and T. All I'm gonna do is I'm going

to slide this over here to the sell side, and it's going to show

me that I'm trading in my personal account and I

have one available share. And so my market cell is

again going to get me out at whatever the next person

is willing to buy it at. So if nobody is willing to buy 18 and t-shirts until

let's call it $24. And I click on a

market order to sell, that is going to drive the price down to twenty-four dollars and get me out there instead of

the current price at 26. Now, the nice thing about AT and T is that

it is a massive, massive company and there's a

whole lot of people trading AT and T and there's a lot of action back and forth on 18 C, so I don't really have to worry about that and it's

not really going to be a factor because I

know that there's enough people on both

of the buying side and the selling side

that are going to be willing to either take

that trade or give it up. So all I'm gonna do is I'm

going to sell at the market. I'm going to sell

one share rate here. And you can see that it's

going to get me out at about 26 dollars

and eighteen cents. We'll see where it

actually executes, but let's test it out here. We're going to

click on Continue. I'm going to confirm this order. We're going to click on Done, and now we can go back

to our portfolio. We should have that share no longer in our

portfolio shoot, so we should only

have one position, which is exactly what

you can see right here. And let's go see where

that executed at. Okay, so when I go

to the Activity tab up here in the top and I click on the 880

market sell order. It's displayed in

Canadian dollars right here unfortunately. But as you can see,

we've got out at $26.13, which is pretty close

to where we were at. At the moment, I

clicked on that buns. So as you can see, the market order

isn't going to make a significant change in the price that you're trade

actually executes at. But it can make a small

impact on that price. If you want to alleviate that, you can use what's

called a limit order, which is exactly

what I walked you through when we

bought the shares. And that will set the maximum

amount that you're going to buy or the maximum amount

that you're going to sell at. And that can protect you from a price ceiling that

you weren't expecting. And so, and so in this video, I just bought AT and T

with a limit order and I sold AT and T With

a market order. Now, what's very exciting

is that in the next video, we're going to start talking

about how to do that multiple times in order to

start building a portfolio.

8. Building a Portfolio: All right, everyone,

welcome to lesson 6. Now that you know how

to buy and sell stocks, it's time to start talking about how to build that portfolio. And so in this video, I want to walk you

through my philosophy and my thoughts when it comes to portfolio management and

the two main considerations that you need to be

thinking about when saying, okay, how do I build a

long-term sustainable, steady return portfolio or diversification

and position size. Those are the two main

factors that you need to think about and that we're

going to cover in this video. So number 1, diversification. Diversification

means investing in multiple different industries

that are not related. And we do this so that if one industry crashes or portfolio will have stalks

in other industries, they should do well. So for instance, if we hold a portfolio that has both

airline companies and oil and gas companies

in it can give us great diversification

because when oil and gas prices fall, that means that our

oil and gas companies probably won't do well. But that also means that the largest expense for airlines, which is gasoline or fuel

for these airplanes, it means that their

largest expenses now cheaper and they should

probably make more money. And so when gas prices fall, airlines usually do well and having a diversified

portfolio can help you balance out those highs and lows so that you

achieve steady returns. And so the idea is to

have diversification in your portfolio where you have companies in a variety

of different industries, where if one does poorly, the other one should do well. That's the concept and that's the idea behind diversification. And it basically

helps you to create steady or returns

over the long run. Now, here is an example of

a diversified portfolio. So let's say that you had a

portfolio that consisted of a variety of stocks and

five different industries. So retail, telecommunications, real estate, infrastructure,

and utilities. You held stocks in a variety of different industries in

these five industries. And I think that that would be a very diversified portfolio when utilities don't do well, real estate should do very well when retailed doesn't do well, infrastructure

probably will do well. So a variety of different

offsets that you will find that you have with a

diversified portfolio and there's a lot

of benefits to it. Now, the second factor

that you need to consider here is position size. Position size is

about how much money you have invested

into each stock. Now, in general,

what we wanna do is try and keep it fairly

equal and balanced. So for instance, if you have ten different positions in

dividend-paying companies, a good rule of thumb would be to go equal positioning

amongst all of those 10% of your

available funds into each of those positions. That way you can hold a diversified portfolio

with good position sizing. We're not all of your

money is in just one egg. Your Money is spread out evenly amongst a variety

of different eggs and hopefully a variety of different nests being the

industries that you choose. Now, here is an idea of

an example portfolio. And pretty much my, my portfolio that I have

for dividends right now. And so I don't like to follow more than ten stocks

because anything more than 10 is just

too much to cover. So for me, I have

10 positions and I put 10 percent of my money

into each of those positions, try to have those positions

in five different industries. And so there's just

a really good rule of thumb if you're

just getting started, this is where I would start, where I would start with

even less than this. Because having too

many positions and too many

companies to follow, especially in the beginning, can be very overwhelming and it can take up too

much of your time. Dividend investing is something that should be almost passive. It should be very easy to do. It shouldn't be

something that you think about every single day. It should be something

that you think about every now and then. When you check your accounts,

check your balances, and you sit down

at your computer after you get paid and you say, I've got a little

bit of money to invest, where should I put it? Now, just for this course, I've put together an

example portfolio here of a perfectly diversified and

position size portfolio. Now, obviously, in real life, this doesn't happen

because most of the stocks go up and

down all the time and you're never going to achieve a perfect 10 percent balance between all of your

securities here. But what's nice about this

portfolio is that the position sizes at 10 percent here are all of the

companies in the middle. So we've got Duke Energy, which is utility

company for this, which is another

utility company. We've got Caterpillar

and Brookfield, which are both

infrastructure companies. We've got Simon Property

Group and Crown Castle group, which are both real

estate companies, got AT and T and tell us what your telecommunications

companies, we've got Target and Best Buy, which are in the retail space. And so we've got five

different industries. We've got 10 different stocks, and each stock has an equal balance at

10% of the portfolio. Here are all of the tickers, right here on the right-hand side under the ticker column, and just a little bit further over here on the yield Kong, I've actually gone into each and every company and calculated

the yield for that stalk. I've taken them all

right here and then averaged it out at 3.8%. And so if you're just getting

started in dividends, Here's a sample

portfolio that you can look at that you

can model off of. You can make your

own changes to it. But this will get you

started with a 3.8% average yield portfolio in

some very good companies, some very large stocks that is probably going to do very

well over the long-term. Now, that was just an example

that I've put together. But what I wanted to

do in the rest of this course is equip

you with the tools and the knowledge and the skills

to evaluate companies for yourself and determine

which company is going to fit in

your portfolio. So in the next few lessons, we're going to talk about how to choose which companies to add to your portfolio and how to better evaluate these companies

to meet your goals. I look forward to

seeing you there.

9. Financial Statements: All right, everyone,

welcome to lesson 8. Now that you understand

the payout ratio, it's time to start

diving a little bit more in depth into the

company financials. And so in this video, we're gonna talk

about where to find the financials as well as

what to look out for in the three things that you really want to watch

for when it comes to company financials and evaluating

different companies for your portfolio is number

one, increasing revenue. We want to see that

revenue going up over time because

that is a sign of a healthy company and that shows that they're

going to have more cashflow in the future

to increase that dude. And which is exactly

what we're looking for. Number two is we want that

company to be profitable. Like I said before, that healthy companies

and the good companies are paying their

dividends out of profits. And so the more profit

that a company is making, the more dividends that we are going to receive

as shareholders. And so we wanna make sure that our companies

are profitable. And then the last thing we wanna do is look at the balance sheet. The balance sheet

is going to give us an idea of what the

company owns or how much cash and equivalent

assets of the company has compared to how much debt the company has and how

much money they actually 0. And so it's a good idea or

it's a good tool to give us an idea of how much the company has and how much

the company owes, and how healthy the company

is at the current moment. And so those are the three things that

we're going to try and look for when it comes to

the financial statements. Now, how do you find

the company financials? You may have never

done this before. And so in this video, we're gonna go through a live example and I'm

going to walk you through exactly how to find

the company financials. So in general, when it comes

to finding these financials, there's kinda two main

sources that you can go to. The first source and

usually the best source and the easiest source is going to be the company websites. So whatever company

you're looking at, type their name into Google and then type

Investor Relations. And a webpage will

pop up that usually has all of the

information you need. If you can't find it there, you can go to websites

called either Edgar or CDR. Cdr is for Canada, Edgar is for US companies, and your company

will have to file their financials

on these websites. And so if you can't find the financials on

the company website, you should be able to find

them on either CDR or Edgar, and we'll go through an

example of that as well. So what we're gonna do here is we're gonna go through an

example with caterpillar. We're going to try and

find their financials. It feels like

they're just kind of a good example for

this entire course. So I'm gonna open up a new tab here and we're going to type in caterpillar

investor relations. And the first link here, as you can see, caterpillar Investor Relations

very easy to find. And this is going to

basically take you to the website that is

specifically designed for investors and

to give investors information about the

company and about the stock. And as you can see here, you can find pretty

much anything you need to know

about the company, about the stock, even a

slide deck that gives you a brief overview of the company and everything

you want to know. An almost every company

that you need to look up is going to have something

very similar to this. And so you can literally do

all of your research here. But what we're going

to try and do, especially in this lesson, is focused on the financials. And so caterpillar has an option here at the

top for financials, we're just going to click

on the main tab here. And then as you can see, the last reported quarter

was third-quarter 2021. It's highlighted in

yellow right here. And this kinda gives you a press release and kind of

a summary of the financials. But what we want is the

actual financial statements. And for most companies, what we're going

to be looking for is the quarterly report. And for us, that form

is called the 10 Q. Now, every year come he's

going to have to put out an annual report and

that is called the 10 K. So you're either

looking for the 10 K, which is the annual report, or if it's a quarter

in-between the annuals, you're going to be looking

for the 10 Q for us. We're on the third

quarter of Caterpillar, so we are looking for the

10 Q and they even have one here that is described

as the cat Financial Form, 10 Q which should be the

perfect form for us. And so at the top

here is going to be basically a description of

what is inside of this form. And then as you scroll down, we're going to come

across the financials. You can see part one, financial information

right here. And this is going to be the consolidated statement

of result of operations are basically

the income statement or the profit and loss is

another word for this. And so this is a great place

for us to start because this is where we

can kinda check off those first two things that

we need to talk about. We're increasing revenue

and profitability. And so we can look at

that on this form here. And so as you can see here, sales and revenues is the first category that

we're going to look at. And in the year of 2021, they brought in a

11 billion dollars. As you can see here, these

numbers are in millions. And so they brought

in $11 billion in the sale of machinery,

energy, and transportation. And they brought in $690 million

with a financial product for total sales and revenue

of $12.397 billion. Now, like I said, we are looking for revenue

growth because revenue growth means that the company

might be able to give us a bigger dividend in the future. And when we compare

2021 to 2020, we can see that the

revenue in 2020 was only $9.8 billion. And so if we just do

the quick math on that, I'm going to pull up my

phone right here and we go 12,397 minus 9,881 equals 2516. And if you divide that by the 2020 revenue,

which was 9,881, that gives us a 25

percent increase in revenue for this company

and revenue year-over-year. And so the revenue

from the year of 2020 to the year of 2021

increased by 25 percent, which is extremely nice

to see that is very, very healthy, excellent growth. And for a company that pays

a reasonable dividend, that is very, very nice to see. And so when it comes

down to our first factor of increasing revenue, caterpillar has checked

out blocks and they have basically done a great job in the blown it

out of the water. Now the second thing

that we needed to look for was profit, and that is what we were

looking for down here. And so right at the bottom here, you can see is highlighted. It's literally just

described as profit. This is also described as

net income or net profit. And as you can see,

caterpillar generated $1.4 billion of profit in the quarter for the three

months ended September 30th, which is extremely nice

to see and it is up more than twice as much

compared to the year before. So their revenue

is increasing and their profit is increasing and they're extremely

profitable, which is very, very nice to see. And so when we look at

the first two factors of the financials that

I wanted to focus on, caterpillar has checked

both of them with flying colors and they've

blown them out of the water. Now as you scroll down here, we should come across the

balance sheet and you'll notice the balance sheet

when it's kinda broken into three

different categories. And those categories

are your assets, your liabilities, and your shareholders

equity riches right here. And so this is our

balance sheet, this page right here, and the top two categories right here is kinda

what we're focused on. So everything that I've

highlighted right here is what we want to look at because on the top side here

is your assets. This is things that

your company owns. So this is the cash in the bank, the equipment that you have, the buildings that you

have, all the tools, all of the machinery, anything, any equipment, any

trucks, anything like that. Those would all be considered assets and that's what

the company owns. And so when we look at the

assets for Caterpillar, we can see that they own $80

billion worth of assets. So again, this is in

millions of dollars, eighty thousand times a million, that gives them $80 billion. And so that's what they have

in total assets right now. We can also see that

that is up by about $2.5 billion compared

to last year. So they have more assets this year than last year,

which is good to see. But what we really

wanna do is we want to compare this to

the total liability. So total liabilities is how

much money this company owes. And when we look at the total liabilities

for Caterpillar, it's right at the bottom here, and it's basically a summary of all the money that

they owe people. And it is $64 billion. And so the $80 billion

worth of assets and they have $64 billion

worth of liabilities. And that is a good thing. We want the assets to be

higher than the liabilities. If it is higher than

the liabilities by at least a 10 percent margin, That will check the box that

will show us that we have a healthy balance sheet

and that will show us at the balance sheet as

well managed however, if the liabilities are ever equal or greater

than the assets, that is a red flag, that is a cause for concern and that is accompany

that you should think twice about investing in because that means that they

owe other people a lot of money and that debt could put

pressure on your dividend. Because remember that

debt probably as a contract behind it and an

interest rate behind it. But your dividend can be decided on by the

board of directors. And so if they decide that that debt is more important

than your dividend, then they can cut the dividend. And so you want to

find a company where the assets are greater

than the liabilities, that the liabilities do not put pressure on the company's

ability to pay your dividend. Okay, So that was the

summary of the financials. Now just the three things

you need to watch for. You want to see

increasing revenue when you want to see

increasing profitability. And you also want to see a balance sheet

where the assets are greater than the liabilities by at least a factor

of 10 percent. If you have all of

those three things, then it will have

checked all three boxes. And I give you the go-ahead to make that green

light investment. I think it's probably

a good company. Now in the next lesson, what we're going to talk

about is dividend lists. And dividend lists

can be a very, very useful for

finding new companies. So here is everything

you need to know. Let's go.

10. Dividend Lists: All right, You guys,

welcome to lesson 9. In this video, we're gonna

talk about dividend lists now, dividend lists are very simple. They're basically just a

list of companies that have maintained their dividends

for a period of time. And what that means is that these companies are usually

some of the largest, some of the safest and some of the most reliable dividend

companies that you can find in the first list that

we're going to look at is the list of dividend kings. Now, to make it on this list, your company has to

have maintained or increased the dividends

for at least 50 years. So for the last 50 years, if your company

at any point ever got rid of or decreased

your dividend, you would not be on this list. This list is made up of only companies that

have maintained or increased that dividend with the last 50 years and

then having done so, that makes them some

of the most reliable, some of the most trusted, and some of the most

safe dividend companies that you can invest in. And so on the screen here is a list of all of

the dividend Kings. You'll find companies

like 3M, like Coca Cola, like Procter and Gamble, like American starts water-like, a variety of other companies. Most of them are

very well-known. Most of them are very reliable. And this is usually

a fantastic place to start when you're building

a dividend portfolio. Now the second list of companies that I

want to share with you is known as the

dividend aristocrats. And on the screen

here I have a list of dividend aristocrat

companies from Canada. You can also find

dividend aristocrats in the United States and a

variety of other markets. But basically, to make it

on the aristocrat list, you have to have maintained

or increased your dividends for somewhere between

25 and 50 years. So you're not good

enough to make it on the dividend king's list, but maybe you're pretty close, then you would be on the

dividend aristocrat list. And this is kinda the

next level down of companies that don't

have quite the same level of history, but they have over 25 years of history of dividend

increases or maintenance, which is extremely nice to see. And it means that

the dividend that you are buying into today, you can expect that to at least maintain or increase

in the future. And so if you're looking for more companies beyond the

dividend king's list, I would start to look at the dividend aristocrats

list because these are the companies that after the king's list are going

to have the most history, the most security and

the most reputation and the most kind of

longevity behind them. And so this is kinda

where I would start. Now, you can go even further. I think there's a

third level to this, but the dividend kings are kinda the top and the

cream of the crop. And then the dividend

aristocrats. And then after that, the next list that I

like to look at are the list of famous investors and what they're investing in. So just an example of this, you can think of Kevin O'Leary. You've probably seen him

on Shark Tank or Dragon Stan or one of the TV shows or maybe even on social media. He is a famous investor

and we can actually see almost everything that he has invested in because

he runs a fund. And so if you just

go to his website, its own shares.com and you

look at is dividend fund, so it's slash OUS M. You can also just look up

OUS M as a ticker. That's what you would

be buying if you bought OUS m. And in this fund, he has a variety of

different dividend companies that he believes are going to

do well over the long-term. And so you can actually see all the dividend companies

that Kevin O'Leary is holding. And if you have any

other famous investors that are big dividend investors, it's more than likely

that you can publicly see what they are

holding as well. But this is really, really

nice because if you don't like any of the dividend king or

dividend aristocrat lists. And you don't like those kind of longer-term blue-chip companies. You can look at a list like

this because these are all younger growth companies that still pay a dividend that Kevin O'Leary particularly

thinks are going to do well. And so there's a variety of different dividend

lists that you can go out and find depending on what you are looking for. These are just three examples. And what I would

do if I were you, is I would use these lists

as a place to start. Find a couple of

companies that you can do some research on, building an opinion around

and actually believe in. Once you have your belief, then you can add them

to your portfolio. I would start with

the dividend kings and the dividend aristocrats, because they tend to be the safest dividend

stocks that you can fund. Once you have a couple of those, then maybe you start

expanding into some of the younger companies or some of the more

exciting companies. But that's probably where

I would personally start. Now, in the next video, what we're going

to start covering is comparing companies. We're actually going

to look at one company and compare it to the other

company and compare all of the ratios in the financial

statements to figure out which one is a better

investment for our portfolio. So remember to stay tuned

and let's jump right in.

11. Comparing Companies: All right everyone, So now that you have a couple of tools for understanding these companies as well as finding these companies. What we need to start doing is comparing these companies

to figure out which one is the best and which one deserves a position

in our portfolio. Remember, we've only got 10 spots and we've got all

of these other companies basically trying out

and trying to compete for a right to get

into our portfolio. And what we wanna do is we

basically want to be the coach and only let in the best

companies into the portfolio. And so in this video

in Lesson 10 here, what we're gonna

do is walk through an example where we're

going to compare two companies to decide which one gets the right

to get into our portfolio. Let's go. Okay, so the first

thing to keep in mind here when we're comparing companies is you want to try

to compare companies that are in the same industry or have a similar business model, or do the same thing. You don't want to compare a

telecommunications company to an infrastructure company because they do very

different things. The ratios are going

to be different, the numbers are going to be

different and you're not really comparing

apples to apples. So what we wanna do

is if we're looking at infrastructure or if we're looking at

telecommunication, we want to try and find

two or three companies that we think are great

within that industry. And then we want

to compare those companies to try and find the best company

within that industry. We don't want to compare a bunch of different

companies from a bunch of different industries because they aren't really comparable. They're going to have

different pale ratios because the industries and the business model and the gross profit numbers are just different from

industry to industry. So that's the first

thing to keep in mind. Now in this example, what we're gonna do is we're going to say that we want to invest

into a construction company. And we're gonna compare

Caterpillar and John Deere. John Deere and Caterpillar both make construction

equipment. John Deere also make

some farm equipment, but they pretty much both have the exact same

business model where they manufacturer heavy equipment for commercial and industrial uses. And so very good comparison, very easy companies to compare. And now what I'm going

to, I'm going to show you just as simple spreadsheet

that I have made that compares the

different factors that we have already walked

through in this course. Okay, so here's the spreadsheet

that I've put together. And on the left-hand side

here you can see all of the different factors

that we're going to use to judge and

analyze this company, starting with the dividend

yield and the payout ratio, which are the first two

ratios we looked at. Then we're going to go to the financial

statements and look at the revenue growth

quarter over quarter. We're going to look

at the profit growth, and we're also going

to look at the assets compared to the liabilities, the three different factors from those financial statements. And finally, we're going

to finish it off with their dividend growth

in number of years. How long, how these

companies being paying and maintaining or increasing

dividend over time. That's going to give

us a good idea of how trustworthy that dividend is. So on the left-hand

side here we have caterpillar and on

the right-hand side here we have John Deere. And then I have a

couple of notes about a different ratios and what we are seeing in

the numbers here. So we're gonna go through line by line is gonna take

a couple of minutes, but I just want to break this down for you so that you can understand what goes through my head when we are

comparing these companies, okay, so first things first

here is the dividend yield. This is how much money

we get back for every $100 that we invest

into the company. Caterpillar has given us

back to point 14 percent. John Deere is only

giving us back 1.2%. That means that caterpillar

is giving us back almost twice as much our money for

how much we invest into it, which is really nice to see. Caterpillar is definitely

has a higher dividend yield. It's not anything that I would be worried about at this point. It's not above 10 percent, it's only at 2% here, but it is twice as

much as John Deere, which means I'm

going to get twice as much cash flow out of Caterpillar compared

to John Deere, which is really, really nice. And that's definitely

something that I am looking for as a dividend investor. And so I have highlighted

this block green because caterpillar very clearly

wins the dividend yield. Now when we move down

here to the second ratio, we can see that in order

to pay that dividend, caterpillars giving up

44.92% of their profit, meaning that they're

giving up nearly half of their profit back to shareholders at the

end of each quarter, John Deere is doing something

a little bit different. They're only giving up under 20 percent of their profit back to shareholders

every quarter. And that kind of explains why their dividend yield

is so much lower. They're keeping the rest of the money inside of the company. And I assume that they're

using that money to try and grow the company over time. Now when it comes down

to revenue growth, caterpillar actually has the highest current revenue

growth quarter over quarter right now at 25 percent and John

Deere is only at 19.4. So they are fairly

close and honestly, 20 and 25 percent is

extremely high for dividend company like

this that has been around longest caterpillar

and John Deere. So both of these numbers

are very impressive, but Caterpillar

clearly wins that. However, the profit growth on John Deere is much higher than countable or 136

compared to 113. So even though caterpillars

growing their top faster, John Deere's actually generating more profit for the revenue

that they're bringing in. So that is very nice to

see from John Deere. And this is probably

the number that matters a little bit more than revenue is the

actual profit that you're walking away with

at the end of the day. And John Deere very

clearly wins his category. And so, so far, it's

kind of like, uh, to, to, to score between

these two companies. And then when we look at the assets compared to

the liabilities here. All I've done is divided

the total assets, divided by the total

liabilities to give us a ratio of 1.26 for Caterpillar, meaning that they have 1.26 times as much assets as

they do liabilities. That's all I'm doing

there is putting it into a ratio so that we can

compare these two metrics. When you compare

it to John Deere. John Deere actually has 1.23 and actually that is

worse than caterpillar. So realistically

this one should be highlighted green and

this should be white. So realistically I've kinda

mess that up right here. This should be green, 1.26 compared to John Deere, 1 to three because we want the company to have more

assets and liabilities. And so this number being higher is actually better

for Caterpillar. This should be highlighted

green right here. I've made a mistake

on the Excel sheet. Now when it comes to

dividend growth here, John Deere actually has the longer dividend

history of maintaining and increasing that dividend

at 33 years compared to Caterpillar at only 28 years. And so when we look at

these two companies, it's pretty much even this block right here should be green. And it's kinda like a

four to three score here between John

Deere and Caterpillar. I've put my notes

in or eight here, but this is kinda

what goes through my mind as I think about

these companies and as I go through these

metrics now when it comes down making a final decision

here in my thoughts, number one, I think both of these companies are

very good options. Both of them are

very well-managed. The growth is phenomenal, the profit is phenomenal. They're growing year over

year and they're very well managed with regards to

a financial perspective and that balance sheet, both balance sheets

are fairly healthy. Now, John Deere is

probably the safer option, just because that pale

ratios a little bit lower, it shows that they're

probably keeping a little bit more

money inside of the company and that's

always going to be safer for the company. However, John Deere also

pays out of very low yield, and it was only coming

in at about 1.2%, which means I'm only getting a $1.20 back for every

$100 I invest. Honestly, that's not very much. So for me, I like catalog better because cat pays a much

better dividend yield, meaning that they

give me more money back for the money

that I'm investing in. And it is still a very safe

company that does not raise any major concerns of

reason that I say that it's because they

have more assets than they do liabilities. There's still profitable. They're more profitable

than they were last year. The revenue is increasing. There's still maintaining an

increasing that dividend. And everything about the company looks like it's going

in the right direction. So even though John Deere's

probably a little bit safer and probably a little bit better in some

of the metrics. I would personally be

investing in cat because I get twice the cashflow back out of that company without

any additional risk, at least in my opinion. So that is how I think

about these two companies and how I think about

comparing these two companies. Now in the next lesson,

what I want to point out to you is some red flags

to watch out for. So if you ever see these things

come up in your research, It's definitely time to

think twice about this talk. I'm going to tell you

everything you need to know in the next video.

12. Red Flags: All right, everybody,

Welcome to Lesson 11. In this video, I'll

walk you through a couple of red flags

to keep an IO for. And if you ever see

these red flags pop up in your research, It's definitely

something you might want to think twice about. Here's everything

you need to know. Let's go. Okay. So first of all, I just

want to start with the red flags that I pointed out to you already

in this course, just so that you're

aware of them and I can kind of reinforce

them in your mind. So number one is anytime that the dividend yield

is above 10 percent, most companies cannot afford to pay a 10 percent dividend. As you can see, what is to come. These we have looked at

so far are somewhere between 2, 8% yield. So anything above 10

percent is a red flag. It's a red flag because that's

just exorbitantly high. Most companies can't

afford to pay that long-term means that

the payout ratio is probably going

to be very high. And I don't expect a

company to be able to maintain a 10 percent

dividend yield. Because if that existed, every single investor would

be buying into that stock and the price will go up and the yield would no

longer be 10 percent. So if you find a stock that has a 10 percent yield or higher, that is a red flag and it usually means that

something is wrong. You need to do more research. Secondly, as a payout

ratio above 90 percent, the payout ratio calculates how much profit are

going to shareholders. If you're paying more

cash to shareholders, then the profit you are making, that is very clearly

unsustainable and that company is not going to be able to keep doing that. So you need to keep that in

mind because that dividend, unless the company makes a whole lot of money

in the future, that dividend is

going to get cut. Third thing you

need to watch out for is declining revenue. If the revenue is declining, that means that they

have less money coming in to turn into profits, get back to shareholders. That is a very bad thing

and I'm very negative sign. So if you're investing

into accompany that, you are expecting

that dividend to grow and their

revenue is declining. That is something you

need to think twice about because it's probably

not going to happen. Number four is declining profit. Even if that revenue

is going up, if their profit is going down. Something you need

to be well aware of because that profit is what they pay out to shareholders in the

form of dividends. And if that profit

is going down, museums less money

for that dividend. And it means that you're

probably not gonna get paid at some

point in the future. Last red flag that I've

already pointed out here is the assets

and liabilities of the company has

more liabilities than they do assets that as a major red flag because

it means they owe people money and those people

that they owe money to, or in the form of contracting, you do not have a contract

for your dividends. Dividends or the choice of

the board of directors, which means they're

probably going to get cut in the event

that they need that money in order to fulfill the contracts and pay the debt. And so if a company has

a lot of liability, puts more pressure on the dividends and you

may not be able to receive that dividend in the future because

of that liability. And so company as higher

liabilities than assets, it's a major red flag. You need to watch out for it. Now, here are a couple of other things that

you need to watch out for that I have not

mentioned in this course so far. Number one is

management changes. If you see that the

company has gone through more than one CEO in the

last 12 to 18 months. That is a major red flag. Same thing with the CFO. If any of those major

positions changing over or have changed over more than once in the last

12 to 18 months. That is a major concern

and a major red flag. And it means that there's

probably some turmoil behind the scenes. The next red flag that

you need to watch out for is a declining industry. If you're buying stock

in a company that is in an industry that is on the downtrend or that

is on the decline, or there probably won't be

here in ten to 20 years. You really need to think

twice about it because dividend investing is

long-term investing. And if that company and that

industry are on the decline, that is not accompany that

you want to be investing in. And if the industry

is declining, It's more and more pressure on the company and it makes it harder and harder for that

company to be successful. So you need to be

very, very careful. Over the next 20 to 40 years, oil and gas might fall

into that category, where the next five to ten

years tobacco probability falls into that category