Transcripts

1. Introduction: Hi. I'm Matt Cooper. I'm the CEO of Skillshare here in New York. In this class, we're going to go through the three primary financial statements: the income statement, the balance sheet, and the cash flow statement. We are going to use America's favorite business, the lemonade stand, to walk through and actually create those from the bottoms up. This is really designed for someone who doesn't have a finance accounting background. I think it's really important that everyone has at least a basic understanding of financials, and it could be you're part of a big business and you wanted understand better how it runs, or it might be that one day you want to run your own business or start your own company. You just need a little better understanding of how financial reporting works and what it means day to day. Regardless of the situation, it's something that everybody can benefit from. So, for your projects, I'd like you to do your own set of financial statements: income statement, balance sheet, cash flow. You pick the business, keep it simple. When your project is done, we encourage you to upload that to the project gallery and after we give you feedback, you can use Excel, Google Sheets, whatever works for you. But by going through that basic process of creating a simple balance sheet, cash flow and income statement for your own business, I think it will give you a much better understanding of how the whole thing works. So, excited you're here. Looking forward to walking through this with you and let's get started.

2. Getting Started: So, I set this up for you a bit. We're going to go through the three primary financial statements. First is the income statement. Income statement is what it sounds like, it's your income from the business. So, how much you generate a revenue, how much you spend on the various expenses, and what's left over at the end? Second, financial statement is the balance sheet. So, the balance sheet, whereas the income statement is a capture of what you generate and spend over time, the balance sheet is really a snapshot of what you have in any given point in time. So, the balance sheet is your assets, so what you have, your liabilities, what you owe other people, and then your equity, which is what's leftover. Then, third primary financial statement is your cash flow statement. So, there are some differences between what you actually bring in on your income statement and the actual cash that you have depending on your balance sheet. A great example is a credit card. So, if I buy something with a credit card on day one, I've incurred that expense. So, when I go out and buy a shirt, I now owe somebody money. No cash has actually changed hands yet. So, that's a good example of how a balance sheet can impact your cash flow, so that cash flow statement, the third statement, is what captures the differences between what's on your balance sheet and what's showing in your income statement. There's a couple basic terms I want to make sure we go through just to set the right foundations. We're going to use these terms frequently throughout the class. I'll start with the most basic, which is accounting. Really, what accounting is, is just the process of capturing the financial status of a business. The second major term we're going to use is accrual. What an accrual is, is when you conduct a transaction that has some sort of downstream effect, and basically, there is a timing difference between. So, we'll go much deeper into this, but ultimately, accrual is a way of capturing the timing differences between when you incur an expense or generate revenue, and when you actually see the cash flow come or go. Couple terms that we're going to use payables, liabilities, receivables that should tie back to that accrual concepts. So, a payable is when I owe some money. I need to pay them money. So, accounts payable will be I spend a bunch of money buying inventory, I put it on my credit card, I don't have to pay it till later, that's a payable. It's a liability that I owe someone else. Liabilities, exactly that. It's something that I owe that I'm going to have to pay down the road. Receivables is the inverse of a payable, so that's when someone owes me. I may sell you something on loan. You need to pay me in 30 days. I take a receivable on the book. Now, that's a payable for you. Then, you're going to pay me 30 days from now. So, as we talk about accrual accounting, you'll hear those concepts come up because that describes the timing differences between when the transactions occur and who owes what at the end of the day. So, another term you'll hear a lot is balance. So, in basic accounting, there is the accounting equation, and this is common across the globe, and that's assets equal liabilities plus equity. So, that's the balance sheet equation. So, when we go deeper in the balance sheet, you'll see that in the balance sheet itself, basically, what it says is, assets are the things you have, liabilities are the things you owe, equity is the difference between the two. So, when things are in balance, that equation is basically netting out. So, before we dive into the financial statements, we're going to cover two concepts that lead into that. Number one is accrual accounting versus cash accounting. Number two is just how to actually build up to your revenue that goes into your income statement. So, we'll start out with a quick summary of accrual accounting versus cash accounting.

3. Accrual vs Cash Accounting: So, before we dive into the financial statements, I think it's important to give you just a quick overview of the two different types of accounting. So, there is cash accounting and then there's accrual accounting. Okay. So, the first accounting method I want to talk through is the basic one and that's cash accounting. So, this is how for your personal taxes, if you're running a sole proprietorship, if you're an independent contractor, you will report your taxes based on cash accounting. So, cash accounting, well, it sounds like the actual cash changing hands, it's ultimately about the timing of the transaction and when you get to recognize that transaction. So, think of it as a debit card regardless of whether or not the cash changes hands, the timing of that transaction is the timing of the activity and when you would recognize that on your financial statement. With cash, it's ultimately, if I take $99 in day one as an independent contractor or as an individual or a small business, I'm going to recognize that cash day one. So, that is revenue for tax purposes when that cash changes hands. Similarly with expenses, when the cash goes out the door, when I spend the money to buy lemons from a lemonade stand, that's an expense. It gets recognized right away. Think of cash accounting as just the most simple way to track your finances. Ultimately, whatever is in your bank account is reflective of what has happened on your income statement. If the cash balance is going up, you made money. If the cash balance is coming down, you lost money. The simplest way to think about it is when does the money move? In cash accounting, when the money moves is when things are recognized. In the accrual accounting, that may or may not be a case. For individuals, the advantage of cash accounting is you get to recognize the expense as you spend it. You're an artist and you need to be buy paint. When you pay for that paint, you can recognize as an expense and take it out of your taxable income on the day that it happens. The negative is on the income side. Let's say, somebody pays you an advance for that painting. You have to recognize that revenue on the day it's received. So, that goes into your taxable income. You don't get to defer that income until you deliver the paintings. So, you could take on the cash day one. You're going to pay taxes on that, and it may take you six months to do the custom painting, and then you deliver it. So, for individuals, there's pluses and minuses. Generally speaking, it works out in your favor. That's certainly a lot simpler from an accounting perspective, but there are some trade-offs. So, the second major term we're going to use is accrual. Accrual accounting is where things start to get a little more complicated. It's really about that timing difference. So, as you recognize and take action within the business, that's when the transaction occurs from an accounting perspective regardless of whether or not cash changes hands. Well, we talked about a debit card for cash accounting. Think of accrual accounting in terms of a credit card. If I go out and buy a shirt, I may have purchased the shirt. I get the shirt, but now, I have a payable. So, cash didn't change hands. I still spent money. I'm going to have to pay that later. So, this is how businesses operate from an accounting perspective. If I receive $99 from you for your Skillshare annual subscription, I now owe you $99 in liability because I have to deliver that service over time. As we think about accrual accounting, particularly for revenue, that timing difference between when I receive the cash and when I get to claim that revenue is really tied to when the transaction occurs, when the service is delivered, when the materials are used. So, whether it's Skillshare you buying a $99 annual subscription or it's a lemonade stand and I go buy a bunch of lemons, if I'm running a lemonade stand as a corporation using accrual accounting, I spend the money on the lemons on day one. I walk out the door with 50 lemons. In cash accounting, that's an expense I can take it off the books. In accrual accounting, I now have an inventory of lemons. So, I have the $50 in lemons showing up as an asset on my balance sheet. As I use those lemons to make lemonade, that's when I start to actually recognize that expense. So, I've accrued $50 in lemons as inventory. Let's assume I use $5 in lemons every month to make lemonade. Now, my asset of lemon inventory is coming down by $5 every month and I'm expensing $5 in lemons as I use them to make lemonade. So, you can see the timing differences there between cash accounting and accrual accounting. The goal of the accrual accounting is the matching principle. The matching principle is the basis of accrual accounting and what that says is when the activity occurs to the transaction, it shows up on your financial statements regardless of when cash changes hands. For accrual accounting, the advantage is it's probably more reflective of what's going on in the business day to day. If I buy a shirt with a credit card, it doesn't mean that I don't owe anything. It doesn't mean that I haven't transacted. I do owe that money. It does have to come out. So, for companies that are obviously spending much larger dollar amounts and earning much larger dollar amounts, it's just a much more accurate reflection of what's happening in that business day to today. The negative is it just brings a lot of added complexity. Going forward, we're going to be talking about accrual accounting because we're going to be looking at corporations, income statements from big companies as well as a fictional Lemonade Stand Corporation. We're going to talk about accrual accounting. I think most people figure about checkbook, you understand cash accounting. It's accrual accounting of where the differences come in and where there's a little more understanding of what's going on to understand what that means for the day to day of a business.

4. Calculating Revenue: Before we dive into the full financial statements, I want to spend a little time talking about the first line or the first couple lines of the income statement, which is your revenue line. If you are building a financial statement or income statement from the ground up, you need to spend a little time thinking about the components that go into how you calculate revenue. So, we'll start with our fictional lemonade stand and talk about how we get to the revenue line. For lemonade stand, we're going to assume that you sell a couple different products, and just to give you a sense for different revenue models and how that would be calculated. For lemonade, it's pretty simple. How many units do you sell? So, in January, we sold 1,000 cups. We charged a dollar a cup. So, our total revenue from lemonade sales is $1,000. We had a great month in February. We sold 2,000 units at a dollar a unit to get to $2,000 in total revenue. In addition to our lemonade, coming into this year, we decided to launch a cookie line. So, we have a separate product, and we've created a separate revenue line for that product. The reason you do that: A, you want to know where your revenue is coming from, but also as you start to look at your cost of goods sold and we get into the income statement, it's important to have that separate products listed so that you can track your revenue expenses on a product by product basis. So, for our cookies, we started out. First month, we sold 140, $1.50 a cookie. That gave us $210 in cookie revenue in January. The next month, in February, we doubled that. We did 280 cookies at $1.50, so $420. Whether it's a lemonade stand or John Deere or any kind of manufacturing business where you're selling a product, product businesses tend to have certain differences and certain consistencies within their financial statements and differences with services businesses such as consulting firms. Lot of tech companies, they have different models. You have subscription businesses like Spotify and Skillshare and Netflix. You have other tech businesses, enterprise software companies. So, there are some differences between business models and how they recognize revenue and how they would build up to this revenue line. But I think you can think of them with a more traditional product businesses as ultimately, it's number of units times revenue per unit. That's your revenue. Now, this business, we're also going to walk through a subscription model. So, let's say that we sold lemonade subscriptions, and for five dollars a month or $60 a year, you could get all the lemonade you can drink. So, we started this year, we didn't have any subscribers. This was another new product we launched in January. So, we start out with zero. Over the course of January, we're going to add 10 new lemonade subscriptions. So, 10 new subscribers over the course of that month. Now, we didn't start out with any, so there weren't any to lose. So, churn subscribers or subscribers you used to have that quit for whatever reason during the month, and so, the ending subscriptions is just the sum of those three. What did you start with? How many new did you add? How many did you lose? So, as we look at February, we'll look at our subscriber count. We started with 10 because that's where we ended in January, and then, we added 30 new subscribers. So, we had a great month, 30 new subscriptions, but of the 10 that started with us in January, five quit. So, we lost five of our January cohort. The net of where we end February is 35. We started with 10, we gained 30, and then, we lost five. So, we netted 35 over the course of that month. So, on average, we started with zero in January, we ended with 10, and we had 5 on average. We started February with 10, we ended with 35. That meant we had 22.5 on average. So, assuming we get to recognize five dollars of revenue per unit, whether they pay the $60 upfront, five dollars a month times 12 months, or if they're paying us as they go, we get to recognize five dollars per month because that's when we deliver the service. So, the subscription delivery model, we recognize that revenue as the service is delivered. So, for January, we take our average of five, we multiply it by five dollars per unit, we get $25 in subscription revenue for January. Similarly, for February, we had 22.5 average customers over the course of that month. We take five dollars per unit, we end up with $112.50 in lemonade subscription revenue. Just to give you a flavor for different types of revenue models, many of you are going to be running your own businesses. You're doing [inaudible] consulting, you're doing freelancing. It's ultimately how many hours did you bill times the number of hours, and that's your revenue. So, we have a small consulting business here at our lemonade stand. We only billed an hour in January and two hours in February, but that gets us to $30 in services revenue and $60 in services revenue for February. So, that brings us to the end of our revenue calculation. We're now going to take that revenue line and those totals, move them over to the income statement, and we'll start working our way down through a full income statement.

5. Income Statements: Part One: Okay. So, now that we have our revenue line, we're going to carry that over to the income statement. So, as we start to go down through the income statement, I've created this to reflect on what we just described as our core revenue drivers, and we'll talk about the expenses that come out of that. So, for our lemonade stand, as I mentioned, we had a couple different products and services. So, you can see our lemonade line which we carry over from our revenue tab here. So, $1,000 in lemonade revenue, $2,000 in February. In January, we sold $210 in cookies, $420 in February, subscription services, that gives us our total revenue line. So, this is just a exact mirror and replication of what we built in the previous tab. So, for January, we had $1,265 in revenue. For February, we had $2,593 of revenue. So, the first section underneath revenue is the cost of goods sold. So, concept of cost of goods sold is you want to capture what expenses are directly tied to the delivery of that product or services. So, it's the most direct inputs whether it be materials or labor. So, in the case of a glass of lemonade, you got lemons, you've got sugar. For cookies, you've got cookie dough. We don't make our own, we just use the cheap cut baked stuff. It's plenty good. There's no reason to get your own wheat and all that. So, we've got the cookie dough, and then the labor. So, you've got the raw materials that you need to turn into lemonade and cookies. But you also have the actual physical labor required to produce those things. So, in my family lemonade stand, my most diligent kid, I'm going to put on lemonade production. So, she's going to be the one squeezing the lemons, mixing in the sugar, producing lemonade. All of the labor that I pay her to create that lemonade is going to go into the cost of goods sold there. So similarly, you may remember we had some consulting services, that's my labor. So, let's assume it's not my labor, I'm paying someone else to do it. I'm taking in $30 in revenue per hour for this consulting service. I'm paying the person who's delivering that service $15 an hour. So, you can see here my cost of goods sold for the consulting services is $15. So, I've got $30 in service revenue. I've got $15 in service cost of goods sold. I now have accounted for both sides of that. So, think of the cost of goods sold as the expenses most closely tied to the delivery of that product or service. You can't produce lemonade without lemon, sugar and water. You can't produce cookies without cookie dough. You can't produce consulting services without consulting labor. So, those are the most direct ties. Now, what about things like sales and marketing? What about rent expense? What about paying my accountants? Those are all operating expenses. Those are not cost of goods sold. I can sell lemonade without a lemonade stand. I can sell lemonade without an accountant or a lawyer. So, there are lots of other expenses but these are the ones most closely tied to the delivery or production of that product or service. So, once I take my total revenue and then I subtract out my cost of goods sold, that gives me my gross profit. So, my gross profit is the most direct tie to how much I'm making per unit, and so you'll see in this case, I earn $2,593 in February. The direct cost of goods sold associated with delivering those products and services is $664, and that leaves me with $1,928 in gross profit. So, gross profit as a percentage of my revenue is 74.4% here. Circling back to cash accounting versus accrual accounting. Now, these are the lemons I actually used in the production of my lemonade. If I were on a cash accounting basis, I may have purchased these lemons back in December, and they'd been sitting in the refrigerator since then. In cash accounting, there would be no expense here for lemons because I didn't buy the lemons this month, I bought them in a prior period. In accrual accounting, it doesn't matter when I bought them, it matters when I use them to produce the lemonade. So, even if I had them sitting around the kitchen, I'm going to recognize that expense in this month because that's the month that I produced the lemonade. We'll keep circling back to this cash versus accrual accounting concept, and as we get into the balance sheet, you'll see where that inventory comes into play.

6. Income Statements: Part Two: So as we work our way down the income statement we start to get from get into the core operating expenses of the business so once you get below the gross profit line then you start to look at sales general administrative expenses research and development costs etc. So the next major line that I have here is sales and marketing expense. So for sales labor, all right I've got my one kid behind the scenes. She's doing all the labor to produce the lemonade. I've got another kid out run around the streets and she's actually selling lemonade. So she's flagging down cars she's handing out flyers in front of the grocery store. All of that labor to bring new customers in. All of the flier materials I'm putting up Google Ad Words or television ads all of those expenses come into my sales and marketing expense line. So here I've got my sales labor. I'm sending her out. She works 20 hours at eight dollars an hour and that gives me 160 dollars in sales labor. We spent 40 dollars on flyers marketing materials sales materials. And so that gives me 200 dollars in total sales and marketing expense in January and 220 in February so that's trying to capture what is the cost I'm spending to acquire new customers and bring them into the business. The next major section is our general administrative costs so G&A is kind of everything else. So it's not the directs expenses required to produce the product or service. It's not products. It's not expenses tied to the acquisition of customers. It's everything else I need to run the company. So in our simplified example here I've got my third kid she is our account. She does all the numbers she runs the books she is doing all the behind the scenes operational labor to keep the business running. All of her labor is captured here. So 20 hours times ten dollars an hour. I've got 200 dollars and 210 in February. I also have rent. My landlord charges me 50 dollars to keep my lemonade stand on his property. 50 dollars in January, 55 in February. I also have some outside legal and accounting expenses of 25 dollars in February 30, or 25 January 30 in February. So my total general and administrative expenses 275 for January 295 for February. So then moving into depreciation and amortization. So this is where we come back to one of the key differences between accrual accounting and cash accounting. There is equipment that I have to buy to make my cookies to make my lemonade. In a in cash accounting basis when I buy that equipment, it is immediately expense. And in accrual basis I buy that equipment on day one. Let's say that you know that piece of equipment may last me for three years. So the estimated useful life of that piece of equipment is three years. If I paid 300 dollars for it I would recognize that expense on a monthly basis over the next three years. So a hundred dollars a year. What's that. A twenty five a month. I would recognize that over time to general it to gradually chip away at that upfront cost of 300 dollars. In this case let's assume I bought a cookie oven for 60 dollars and I think that cookie oven is going to last me 12 months. So I would depreciate that asset I would recognize five dollars of depreciation expense each month over the course of 12 months until I've eaten up the entire 60 dollars that I paid upfront. So again if it were cost basis you'd see a 60 dollar expense line buying a new cookie oven because we're on accrual basis we recognize five dollars of depreciation expense over time. One key difference. It's called depreciation and amortization. Depreciation tends to be associated with physical assets whereas amortization is a similar concept but for intangible assets so let's say I bought a I bought a trademark or I bought a patent of how to buy a cookie or how to make a special cookie if I acquired that patent from somebody else. It's an intangible non-physical asset. I would then depreciate or I would amortize that intangible asset over time. So to give you the simplified version depreciations for physical assets amortizations for non-physical intangible assets. Either way whether it's depreciation or amortization the concept is the same you pay a certain amount upfront and then you chip away at that over time by expensing it through the depreciation and amortization line. Now moving on to research and development so most lemonade stands don't have an extensive extensive R&D program. Let's pretend that I have a whiz kid that I basically lock in a closet with a single light bulb. And all she does is think up new crazy lemonade concoctions so that we can innovate within our business. Those are indeed costs go into a separate category. It's really you need to be thinking about is investment in the future of the business as opposed to a current expense so companies that have heavy R&D costs are investing in future products and services that they can use to grow their business. So in our case the labor associated. Fifty dollars a month for her to sit back and concoct those new formulas. All the materials the test Lemmons the special Himalayans sugar that she uses. Anything going into those experimentations in that new product development is captured in R&D cost line here. So the final line here is you get to our operating expenses. So this is really just the sum of all of our sales and marketing expenses, our G&A expenses, and our R&D costs. And then our depreciation and amortization. So you take all those. That is our operating expense. That takes us to our operating income. So our operating income is just our gross profit minus our total operating expenses. And think of the operating income as the simplest reflection of how much money you're making from that business in a given period. So the operating income again if this were cash if this were a cash accounting model should reflect exactly what is going in or out of your bank account before you get to non operating items like taxes or other expenses. So so let's let's touch on that a little bit. The financial statements the operating income really that should be the revenue minus expenses most total type most closely tied to the business at hand. The taxes you pay if you have to pay regulatory fees you have to pay for registrations. So for a lemonade stand I've got to pay a local health department to get certified registered. Those aren't really associated with the day to day execution business paying taxes of government. That's reflective of the income I'm making not the business I'm running. So we want to capture those but we want to capture them below the operating income line that gets us down to the net income line. So the net income line is exactly how it's named. It is the net income after you take out all of your top line revenue. You subtract it out the cost of goods sold the actual expenses required to deliver that product or service you've taken out all your sales and marketing expenses your journal administrative expenses your R&D costs any other non operating items like taxes other expenses not associated with day to day running of the business that is your net income. If this were a cash accounting business your net income plus. So if you took your cash balance at the beginning of the month you added your net income your cash balance at the end of the month should equal those two combined. Because we're in accrual accounting that's not going to be the case. That's a great lead into the balance sheet which we'll talk about next. But for an accrual accounting business the net income is the closest replication of what came in and what went out as it relates to the actual day to day execution business. That brings us to the end of the income statement section. And now we're going to move on to the balance sheet and start looking at your assets liabilities and equity.

7. Balance Sheets: Okay. So, in this section, we're going to go into the balance sheet. So, the key equation for the balance sheet and what keeps the sheet in balance is the equation assets equals liabilities plus equity. So, as we think about a balance sheet as we walk through the example, you always have to keep that equation in balance. So, starting with assets, the asset is something you have that has current or future value. So, checking account, obviously, cash has immediate value, a receivable. So, if I have sold you something and you're going to pay me later, that obligation for you to pay me, that receivable on my books has future value. So, think about the assets of everything within your business that has a current or future value. So, next is the liabilities. Liabilities are things that I owe or things that I'm going to need to pay out or obligations that I have as part of that business. So within liabilities, you typically have current liabilities, which are things that- or obligations that are going to come due within the next 12 months, and then you have long-term liabilities that are greater than 12 months. So, if I took out a loan to finance my business, let's say it's a $500 loan. I need to pay back 100 this year. I need to pay back 400 next year. There's a current portion of that loan that's due, that goes into my current liabilities because that's due within the next 12 months. Then, I have a long-term portion that's due later, longer than 12 months. That goes into my long-term liabilities. Then, the last piece is the equity. So, there's two main components to equity. There's the equity that I've earned through the retained earnings of the business. So, the accumulated earnings over time. There's also paid in capital. So let's say I invested a certain amount or I brought in a family member, they gave me a couple of $100 to invest in this business. That equity goes into the business. So again, thinking about my balance sheet, let's say you invested $500 in my business, I take $500 in cash, my equity goes up by $500. So I've added $500 to both the assets and the equity at the same time, my balance sheet is still in balance. That's how I keep my balance sheet in balance. We'll keep coming back to that equation as we walk through this specific balance sheet for the lemonade stand. Okay. So, we'll walk through our fictional balance sheet for our lemonade stand. The first line is we look at assets equals liabilities plus shareholder equity is our cash line. At the end of January, we had $500 in our checking account. At the end of February, we had $1,332 receivables. So, this is money that we are owed. So, maybe some of our subscription business, they didn't pay us right away. They owe us that money. That would go into our receivables line. So the receivables, all cash that's owed to us from other people that we expect to receive in the next 12 months, and that gives us our total current assets. In this type of business, you're not going to have a lot of long term assets. It's really going to be equipment. So, because we've got our cookie oven, we've got our lemonade squeezing machine, all of that equipment goes into our asset line and that gives us total assets of 1,600 in January, 2,547 in February. For our liabilities, we start to get into our payables. So, again, maybe this is our lemon distributor, we owe them $50 in January, $6 in February. We have other accrued expenses the other vendors or other businesses of $25 and $30 in February. Then, we do have a loan. So, let's say we took out a loan to start this business. You can see the long-term portion here of $100. But then, we have a short term portion of current portion that shows up in our current liabilities. So, between our current liabilities plus our long-term debt, which in this case is our only long-term liability, that gives us our total liabilities. So, assets minus liabilities equals shareholder equity. You may see it called shareholder equity, stockholder equity, I've got both here. There's a couple of different terms that are interchangeable. Those will be the most common ones. We've got our retained earnings, which is $1,345 in February. That is equal to the $410 that we started with plus our net income from our income statement. That equals to $1,345. So, think of the retained earnings as the accumulated net income of the business over time. Then you have paid in capital, which is the money that came in whether it's money I invested, money outside investors put in. But that's the equity that came in as cash, invested into the business, and that's how it's captured on the balance sheet. So that's equity that's into the company. In this last line is our liabilities plus our equity. So, when you combine those two, to keep the balance sheet in balance, that should equal our total assets. So in this case, you can see in January, we had 1,600 in assets, we have 1,600 liabilities and equity. Same thing for February, 2,547 in assets and $2,547 in liabilities and equity. So, hopefully you have a better sense for how the balance sheet works and we're going to carry that over. We're looking at some of the differences between periods on your balance sheet to help tie together that cash flow statement next.

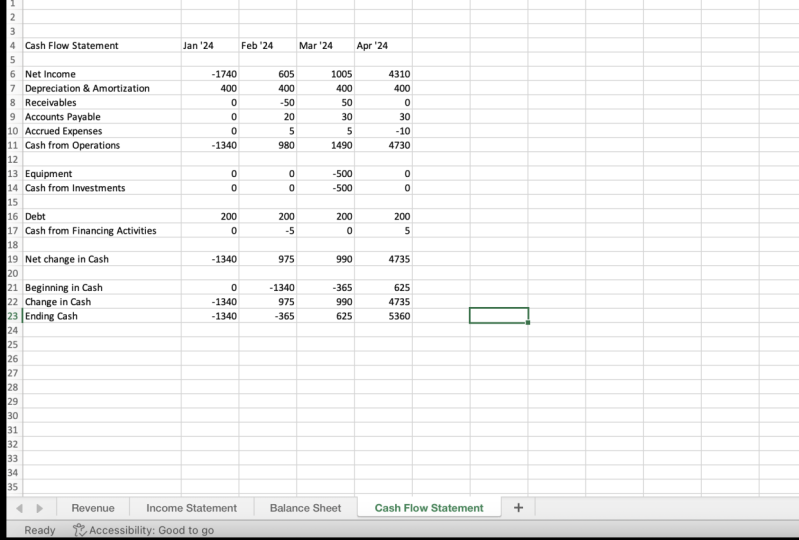

8. Cash Flow Statements: So, the cash flow statement is where you start to see all the differences between a cash accounting methodology and an accrual accounting methodology. So, as you remember, with cash, it's when it comes in, that's when it gets recognized. In accrual, you have timing differences. So, you could have revenue that comes in, and the cash hasn't come in yet. So, what you would get from your income statement actually might look like you have more cash than you do, but because you didn't get it yet, you take that accruals, you have to adjust for that. That's what shows up on the cash flow statement. Similarly, for expenses, there might be things that you spent money on in advance. You didn't actually use those. You had it went into inventory. So, it's cash that came out of the books but wasn't reflected on your income statement, it was reflected on your balance sheet. So, then, that's captured in your cash flow statement. That's where you find the difference between those two. So, think of the cash flow statement as where you start to see all of these differences between cash accounting and accrual accounting document. So, at the end of your cash flow statement, this is where your cash in your bank account will actually tie out to what's showing is the cash on your balance sheet and the cash on your cash flow statement. So, this is the final check to make sure that those three numbers are all in sync and that they align. So, now, we'll walk through our simplified cash flow statement for our lemonade stand. We're going to start with the the net income line. So, the first line of our cash from operations is net income. So, when you look at this spreadsheet, we've got $935 in net income. Now, if we go back to our income statement, that is pulling from the net income line for February on our income statement. So, that is a direct carryover. If you look at the actual formula, you can see it's pulling from that cell in the income statement. So, that's the opening line. Then, we add back our depreciation and amortization. So, depreciation and amortization, as you may remember, that is how we chip away at the money that we spent on equipment upfront. So, if we're amortizing five dollars a month, that's not cash that's actually coming out of our pocket because we already spent 60 on the equipment. We're just now expensing that imaginary expense over the course of the next 12 months to chip away at that money. So, the five dollars, while it shows up on our income statement as an expense, there's no actual cash changing hands. So, we add that back to bring that into balance. Then, on our receivables, so the receivables went up by $20. So, again, if you look at the formula here, it's the balance sheet, it's the account receivable from January minus the account receivable for February. So, if our receivables go up, that means we recognized revenue that we didn't yet get the cash flow for. So, if we just looked at our net income statement, it would look like we have more cash than we actually do, but the reality is, those customers still owe us that money. So, we take $20 off of our cash flow statement to get that trued up. Similarly, with payables and accrued expenses, these are expenses or payables that we incurred because the timing of the transaction was within February, but the cash hasn't actually changed hands yet. So, we just looked at the income statement, it looks like we've lost $10 and five dollars more from our cash balance than we actually did. So, we add that back. So, let's flip back to our balance sheet real quick. So, receivables, it went from 100 to 120. So, we received $20 less cash than we thought we did because receivables went up. There's $20, and we can tie that to the $20 for the receivables line on our cash flow statement. Similar thing for account payable and accrued expenses. We've got $10 and five dollars. So, those are because they're directly associated with the operations of the business. That's why we put it in the cash from operations section. So, you can see with the equipment, now we bought $100 of equipment. So, we will add $100 to our equipment balance. So, let's say, we went out and bought that new cookie oven. We paid $100 for it. You can see on our balance sheet, if we go from our equipment balance of 1,000 in January, and now, it's 1,095, so what happened here? So, you can see, we added the $100 from our cash flow statement or from the cash from investing activities, but then, we lost the five dollars of depreciation that we expensed. So, the net of the $1,000 plus the 100, minus the 95, is the 1,095 that we're showing here on the balance sheet. So, we look at the cash flow statement, we're seeing the five dollars in depreciation and amortization. Again, that was a non-cash transaction that showed up on the income statement. Then, we've got a $100 in equipment. The $100 spend on equipment, it didn't show up anywhere on the income statement, because those type of investments, you capitalize them as an asset on the balance sheet, then you chip away at it over time. So, that was a cash transaction that was not reflected in this net income line that came off the income statement. So, you factor those two in, that's our only cash from investing activities was that the purchase of equipment. Then, we have the last section, which is cash from financing activity. So, in this case, the only thing we did, if we go back to the balance sheet, if you look at our debt and you look at our equity, we didn't have any long term debt change, we didn't have any change in the equity and the paid in capital that came into the business. The only difference is, this current portion of long term debt went from 15 to 12. So, we paid off three dollars of our current portion of the total debt amount in this period. So, we're going to take out three dollars from the cash from financing activities. If we had raised another $1,000 in equity, you'd see that here because it was a cash transaction that occurred that was not reflected in the income statement. So, you get to a net change in cash of $832. So, this is where now we get to the reconciliation between the balance sheet, the cash flow, and then, whatever's in our checking account. So, we started out with $500 in cash. So, if you flip back to the balance sheet, we've got the 500 here at the end of January. Through our cash flow statement, you can see that we had $832 change in cash. Again, that's our cash from operations plus anything we spent or received on investing activities. Then, adding in any cash from financing activities, that gets us to our 832. We add that to our initial 500, and we have $1,332 in cash. So, that's according to the cash flow statement. Now, within the balance sheet, once we drop that number into the balance sheet, our balance sheet should balance. So, our assets are 2,547, our liabilities plus equities 2,547. We're good. These books are tied out. Everything balances the way it should, and we have an accurate income statement, balance sheet, and cash flow.

9. Final Thoughts: So, that's the end of the class. I hope that you're still awake. The goal here was to just give you the initial taste of what these three financial statements are, how they work together, what they mean for a company, ideally going through the project, and going through the process of creating your own will give you a little bit deeper understanding, and I guess a more tactical feel for how these things get constructed, and what those numbers mean day to day. I really encourage you to go for the projects, I do think it will put a finer point on a lot of what you learned during the class. Put it up on the project page, we'd love to give you feedback, get feedback from your peers, we can answer any questions you may have, and give you a little bit and hopefully give you some other perspectives on financial statements. Hope you enjoyed it. Hope you took something out of this and look forward to hearing from you on Skillshare.

10. More Business Classes on Skillshare:

Matt Cooper, Startup exec and former Skillshare CEO

Matt Cooper, Startup exec and former Skillshare CEO